世界各国のリアルタイムなデータ・インテリジェンスで皆様をお手伝い

リチウムイオン電池市場2023-2033年:技術、プレーヤー、アプリケーション、展望、予測Li-ion Battery Market 2023-2033: Technologies, Players, Applications, Outlooks and Forecasts Enable Ginger リチウムイオン電池は、集電体に塗布された負極と正極を、電解液に浸されたセパレータで分離した構造をしているのが基本である。パウチ型、角型、円筒型に包装され、リチウム... もっと見る

日本語のページは自動翻訳を利用し作成しています。

サマリー

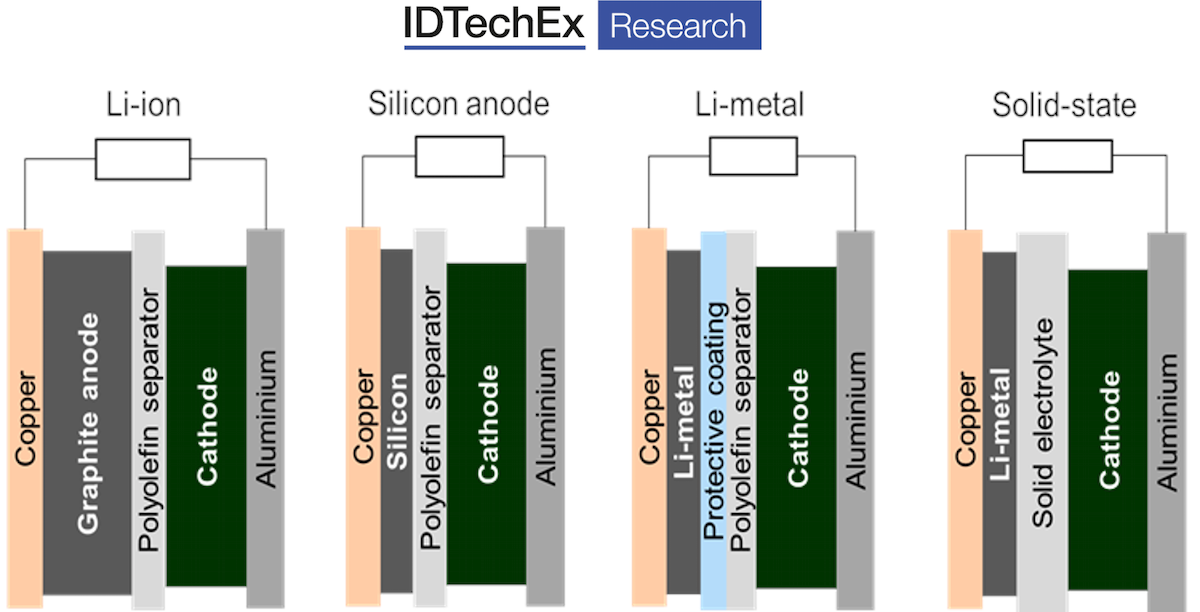

リチウムイオン電池は、集電体に塗布された負極と正極を、電解液に浸されたセパレータで分離した構造をしているのが基本である。パウチ型、角型、円筒型に包装され、リチウムイオン電池パックの基礎となる。リチウムイオン電池は、比較的高性能で、安価で、広く入手可能なため、電子機器から電気自動車(EV)、大型定置用蓄電システムまで、多くの用途で優れたエネルギー貯蔵技術となっている。そのため、ほとんどの用途において、リチウムイオン電池が今後10年以内に何らかの形で取って代わられることはないと思われる。しかしながら、リチウムイオン材料、製造、セル設計、パック設計の開発・革新は続いており、リチウムイオン産業への投資は急ピッチで続けられている。

出典 IDTechEx

IDTechExは、リチウムイオン市場が電気自動車の需要に牽引され、2033年までに4300億米ドル超に成長すると予測しています。電気自動車は引き続きリチウムイオン市場の主要な牽引役であり、今後10年間は電気自動車がリチウムイオン電池の最大市場となる見込みです。コロナウイルス、チップ不足、その他のサプライチェーン問題の影響が続いているものの、電気自動車の販売台数は2021年に640万台に達し、強力な排ガス目標と規制が後押ししています。

LFPは、特に中国でのシェア奪還により、2021年以降、EVでのシェアを回復している。高ニッケル層状酸化物(NMC/NCA/NCMA)材料は引き続き重要であり、大手正極メーカーはコバルト含有量をさらに減らし、わずかではあるが容量を増やすために90%以上のNMCおよびNCAへの移行を検討している。しかし、これらの材料の安全性や寿命の確保には困難が伴う。コバルトの含有量を減らすことは材料費の削減につながり、問題のあるコバルトを調達する可能性を抑えることができますが、コバルトとニッケルへの依存を抑えようとすると、LFP生産の大部分が中国企業によってコントロールされ、国外でのLFP生産計画が少ない中国への依存が高まることになります。これは、欧州や北米の政府やプレイヤーの狙いや目的に反することになる。2021年、リチウムイオン電池、正極材、負極材、電解液、セパレータ、銅集電体の売上の50%以上を中国企業が占めている。

.png)

出典 IDTechEx

正極の場合と同様に、今後10年間はどの負極が使われるかという疑問もある。例えば、シリコンは、高いエネルギー密度と高速充電を可能にする可能性があるため、グラファイトの代替品として大きな関心を集めていますが、まだほとんどがグラファイトへの添加物としての使用に限定されています。シリコン負極への関心が高まり、その可能性は大きく、30社以上の新興企業がシリコン負極を開発しているにもかかわらず、商用シリコン負極材料の生産はアジアの少数の企業によって独占されている。黒鉛は、合成および天然/人工のいずれにおいても、今後10年間は負極材として支配的であり続けると予測されます。本レポートでは、さまざまなリチウムイオン化学物質の使用動向とシェアを分析しています。また、異なる電池化学のコスト内訳と分析、最近の価格材料の変動が電池セル価格に与える影響についての分析も行っています。

リチウムイオン電池の需要急増に伴い、過去2~3年の間にギガファクトリーの計画・発表数が大幅に増加しています。その多くは、CATL、LG Energy Solution、SK Innovation、Samsung SDIなどの既存メーカーが牽引していますが、新興企業や初期段階の企業も、特に国内能力の開発を推進している欧州と北米において、市場への参入を検討しています。IDTechExの分析によると、新しいセル生産能力に関する現在の計画や発表は、2030年までに3TWhに達する。これは予測需要を満たさないが、新しいセル生産工場の建設に必要な期間が比較的短いため、EVからの予測需要を満たすために必要なセル生産能力への追加投資と拡大のための時間を確保することができる。

リチウムイオン電池産業にとって電気自動車市場が重要であることは間違いありませんが、太陽光や風力などの再生可能エネルギーの導入が進んでいることから、定置用エネルギー貯蔵システムがリチウムイオン電池の最速成長市場になると予想されます。電子機器向けリチウムイオン電池の需要は、定置型蓄電システムや電気自動車に比べ、成長率はかなり低いと予想されますが、電子機器向けのセルや電池の価格が高いため、これらのアプリケーションにはかなりの市場価値が残っています。そのため、新技術はまずこれらのアプリケーションから市場に投入され、製品サイクルが短く、電気自動車に比べて要求される性能も低いため、高い利幅を得ることができるのです。

本レポートでは、正極、負極、電解質、セパレータ、銅コレクタ、添加剤など、主要コンポーネントの分析とレポートを提供しています。各成分については、主要メーカー、生産地域、拡張計画などの調査による市場分析に加え、主要技術開発の内訳を掲載しています。リチウムイオン電池 2023-2033」は、リチウムイオン電池の市場、プレイヤー、技術動向などを包括的に解説しています。リチウムイオン電池の需要について、数量(GWh)、金額(US$)、アプリケーション別、正極タイプ、負極タイプ別にコスト分析、価格予測、10年後の予測を掲載しています。

主要な側面

本レポートでは、以下の情報を提供しています:

技術動向と市場分析

目次

Summary

この調査レポートでは、リチウムイオン電池市場の正極、負極、電解質、セパレータ、銅コレクタ、添加剤など、主要コンポーネントの分析とレポートを提供しています。

主な掲載内容(目次より抜粋)

Report Summary

Fundamentally, a Li-ion cell consists of an anode and a cathode, coated onto current collectors, separated by an electrolyte-soaked separator. Packaged in pouch, prismatic or cylindrical formats, they form the basis of Li-ion battery packs. Their comparatively high performance, low cost and wide availability make Li-ion batteries pre-eminent energy storage technology for many applications, from electronics devices to electric vehicles (EVs), to large stationary energy storage systems. As such for most applications, Li-ion batteries, in one form or another, are unlikely to be superseded within the next 10 years. Nevertheless, developments and innovations continue to be made in Li-ion materials, manufacturing, cell design, and pack design and investment into the Li-ion industry continues at a rapid pace.

.png)

Source IDTechEx

IDTechEx forecast the Li-ion market to grow to over US$430 billion by 2033, driven by demand for electric vehicles. Electric vehicles remain the key driver behind the Li-ion market and electric cars will be the largest market for Li-ion batteries over the next 10 years. Despite the ongoing effects of coronavirus, chip shortages and other supply chain issues, electric car unit sales reached 6.4 million 2021, driven by strong emissions targets and regulations.

LFP has been re-gaining market share in EVs since 2021 due its recapture of market share in China in particular. High-nickel layered oxide (NMC/NCA/NCMA) materials will continue to be important, and major cathode manufacturers are looking to move toward 90+% NMC and NCA in a bid to further reduce cobalt content and increase capacity, if only marginally. Difficulties remain in ensuring safety and longevity of these materials. While reducing cobalt content can help reduce material costs and limit exposure to potentially problematically sourced cobalt, a push to limit reliance on cobalt and nickel will increase reliance on China, with the vast majority of LFP production controlled by Chinese companies and fewer plans for LFP production outside the country. This would be contrary to the aims and objectives of governments and players in Europe and North America. In 2021, Chinese companies were responsible for at least 50% of sales of Li-ion cells, cathode and anode materials, electrolytes, separators and copper current collectors.

(1).png)

Source IDTechEx

Similar to the situation with cathodes, there are questions over which anodes will be used over the coming decade. For example, silicon has received considerable interest as a replacement for graphite due to its potential for enabling high energy densities and fast charging, but it is still mostly limited to use as an additive to graphite. Despite the growing interest, large potential for, and 30+ start-ups developing silicon anodes, commercial silicon anode material production is dominated by a small number of companies in Asia. Graphite, both synthetic and natural/artificial, is forecast to remain the dominant anode material over the coming decade. The report analyses the trends in use and shares of different Li-ion chemistries. Cost breakdowns and analysis is also provided for different cell chemistries as well as analysis on the impact of recent price material volatility on battery cell price.

Given the rapid increase in forecast demand for Li-ion batteries, there has been significant growth in the number of gigafactories being planned and announced over the past 2-3 years. Much of this has been driven by incumbent manufacturers such as CATL, LG Energy Solution, SK Innovation and Samsung SDI but start-ups and early-stage companies are also looking to enter the market, especially in Europe and North America where there is a drive to develop domestic capability. IDTechEx analysis shows that current plans and announcements for new cell production capacity will reach 3 TWh by 2030. While this would not meet forecast demand, the relatively short time-period needed to build new cell production factories allows time for the additional investment and expansion in cell production capacity needed to meet forecast demand from EVs.

Despite the undoubted importance of the EV market for the Li-ion industry, stationary energy storage systems are forecast to be the fastest growing market for Li-ion batteries, given the continued drive to adopt increasing levels of variable renewable power sources such as solar PV and wind. While growth in Li-ion demand for electronics devices is forecast to grow at a much slower rate than stationary storage or EVs, the higher price of cells and batteries for electronic devices means considerable market value remains available in these applications. New technologies can therefore make their way onto the market via these applications first, with higher margins on offer alongside shorter product cycles and often less demanding performance requirements compared to EVs.

This report provides analysis and reporting on key components, including on cathodes, anodes, electrolytes, separators, copper collectors and additives. For each component, the report provides a breakdown of the key technological developments, in addition to analysis of the market through a study of the key manufacturers, production regions and expansion plans. Li-ion Batteries 2023-2033 provides a comprehensive view of the Li-ion battery market, players, and technology trends. Cost analyses, price forecasts, and 10 year forecasts are provided for Li-ion battery demand by volume (GWh) and value (US$) and broken down by application, cathode type and anode type.

Key Aspects

This report provides the following information:

Technology trends & market analysis

Table of Contents

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(電池)の最新刊レポートIDTechEx 社の最新刊レポート本レポートと同じKEY WORD(battery)の最新刊レポートよくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

詳細検索

2024/07/04 10:27 162.47 円 175.74 円 209.86 円 |