世界各国のリアルタイムなデータ・インテリジェンスで皆様をお手伝い

燃料電池電気自動車2025-2045:市場、技術、予測Fuel Cell Electric Vehicles 2025-2045: Markets, Technologies, Forecasts IDTechExの調査レポート「燃料電池電気自動車2025-2045年:市場、技術、予測」は、自動車、小型商用車、中型・大型トラック、バスなどのオンロード燃料電池電気自動車(FCEV)市場を調査しています。市場促進... もっと見る

※ 調査会社の事情により、予告なしに価格が変更になる場合がございます。

サマリー

IDTechExの調査レポート「燃料電池電気自動車2025-2045年:市場、技術、予測」は、自動車、小型商用車、中型・大型トラック、バスなどのオンロード燃料電池電気自動車(FCEV)市場を調査しています。市場促進要因、障壁、プレーヤー、技術、モデル、ベンチマーキングを網羅し、今後20年間の販売台数、燃料電池需要、バッテリー需要、市場価値について採用を予測する。

燃料電池電気自動車の動力源は燃料電池スタックであり、貯蔵された水素と空気中の酸素の反応によって電力を生成する。副産物は水だけであるため、燃料電池自動車はバッテリー電気自動車と同様にゼロエミッションのソリューションである。

燃料電池乗用車

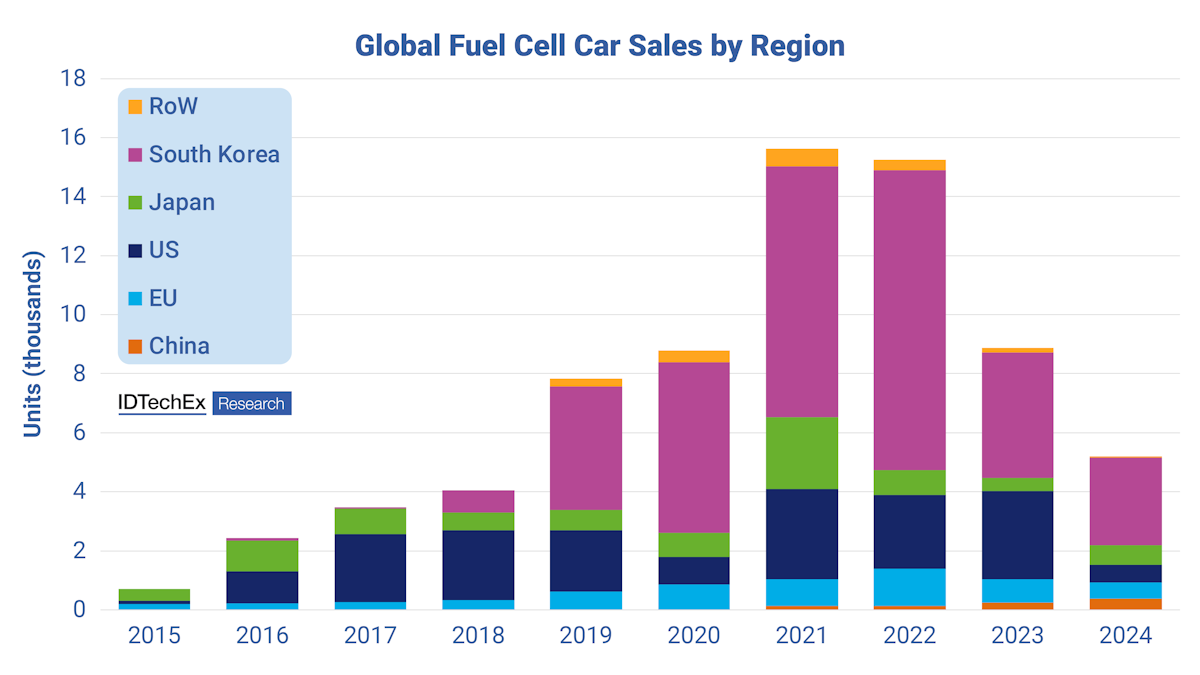

しかし、過去2年間、燃料電池車への関心は低下している。IDTechExは、その主な要因は、高価で信頼性の低い水素補給ステーション、BEVの継続的な進歩、モデルの不足であるとしている。カリフォルニア州や韓国などの地域では、燃料や購入補助金によって燃料電池車の価格が約50%以上引き下げられているにもかかわらず、年間販売台数は2022年の15,000台から2024年にはわずか5,000台へと約3分の2に減少している。一方、バッテリー電気自動車(BEV)は1,000万台以上、プラグインハイブリッド車(PHEV)は400万台以上の販売台数を記録した。IDTechExは、2年連続の市場縮小にもかかわらず、グリーン水素プロジェクトと水素補給ステーションへの国家投資が実を結び始めるにつれて、燃料電池乗用車の販売は徐々に回復すると予測している。IDTechExは、燃料電池乗用車の販売遅れ、販売不足、プロジェクト中止の結果、燃料電池乗用車の予測を前回から下方修正した。

.png)

FC車の世界販売進捗。過去2年間は以前の成長から大きく落ち込んでいるが、IDTechExは販売が回復すると予測している。2045年までの全データと予測は「燃料電池電気自動車2025-2045:市場、技術、予測」に掲載されている。

燃料電池小型商用車

ほとんどの地域では、乗用車は商用車よりも短距離を走行する。商用車は決まったルートを走行することが多く、長距離走行もある。しかし、小型商用車もまた、BEV の急速な改良によって FCEV が遅れをとっているセグメントである。ほとんどの地域で、FCEV は実証フリートやプロトタイプの段階にとどまっている。中国は最大の燃料電池 LCV 市場であり、2023 年には約 1,300 台の販売が記録された。しかし、同年には約 50,000 台の BEV が販売されている。

燃料電池バスとトラック

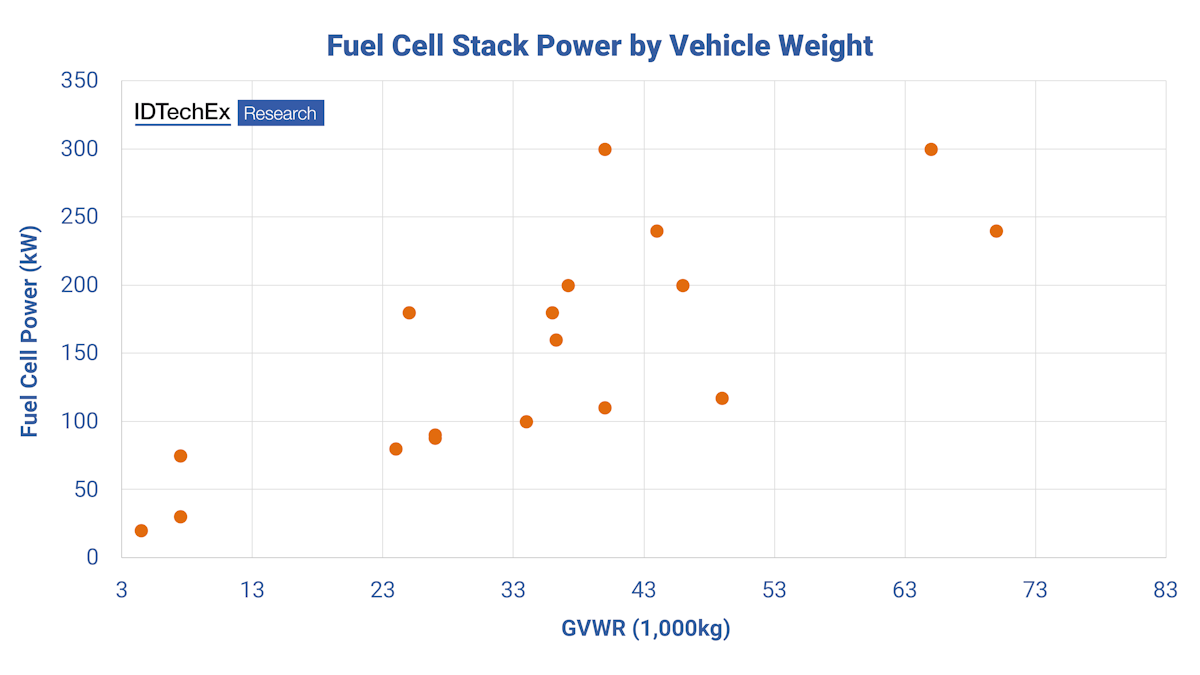

電気バスは世界中で急速に普及している。しかし、小型商用車や乗用車よりも重いため、バッテリーの重量とコストが問題になる。バスは、燃料電池スタックによってバッテリーのサイズと重量を減らすことができる。水素タンクと燃料電池は、車両が必要な期間内に運行するために必要な電力とエネルギーの一定割合を供給することができる。

.png)

FCEVの車両総重量定格(GVWR)と必要な燃料電池スタックの出力との関係。全データは、「Fuel Cell Electric Vehicles 2025-2045: Markets, Technologies, Forecasts 」に掲載されている。

中型・大型トラックは、積載量とデューティサイクルの両面で、自動車部門の中では重いほうである。ゼロ・エミッション・トラックはめまぐるしく変化する環境にあり、燃料電池トラック会社も例外ではない。Nikola、Quantron、Hyzon の 3 社はいずれも昨年大きな財務的障害に遭遇したが、トラックは最終的に FCEV が最も市場に浸透すると IDTechEx が考える車両セグメントであることに変わりはない。米国の国家ゼロエミッション貨物回廊戦略では、2040 年までに貨物輸送をサポートする水素補給ステーショ ンのネットワークを構築することになっており、中国では 2025 年末までに 1,200 箇所の水素補給ステーションを目標 に、毎年数千台の燃料電池トラックを販売し続けている。

バスと同様、固定ルートを持つトラックは、燃料補給インフラを重要なハブやセンターに集中させることができる。これは、航続距離と重量における BEV の現在の限界と相まって、トラック市場に FCEV のチャンスがあることを意味する。バッテリー電気トラックは現在、潜在的成長分野である大型長距離トラック輸送の過酷な要求を満たすのに苦戦している。燃料電池トラックの総所有コスト(TCO)は依然として高いが、生産コストは規模の経済によりいずれ下がるだろうし、グリーン水素プロジェクトが完成して水素燃料の大量生産が始まれば、燃料補給はよりコスト効率的になるだろう。

IDTechExの本レポートは、FCEVの主要セグメントをすべてカバーしており、市場を総合的にカバーしている。市場の最新情報、技術分析、ベンチマークに加え、本レポートで新たに取り上げたPFASの懸念を含む燃料電池用材料や、製造から燃料補給ステーションまでの水素サプライチェーン全体についてもカバーしている。水素充填インフラは、FCEV 市場の発展において重要な役割を果たす。本レポートでは、主要地域(中国、米国、欧州、その他の地域、主に日本と韓国)とサプライチェーン分析をカバーしている。販売台数、市場価値(US$)、燃料電池電力需要(GW)、バッテリーエネルギー需要(GWh)など、地域別、車両セグメント別に詳細な予測を掲載している。

主要な側面

本レポートでは、自動車、中型・大型トラック、バス、小型商用車を含む燃料電池電気自動車市場について、以下のような広範な概観を提供しています:

目次 1.エグゼクティブ・サマリー 1.1.レポートの概要 1.2.燃料電池自動車とは何か? 1.3.燃料電池自動車の魅力 1.4.水素燃料電池車の普及障壁 1.5.水素経済 1.6.水素の色 1.7.BEVとFCEVのシステム効率 1.8.燃料電池乗用車の展望 1.9.燃料電池乗用車の成長、停滞、衰退 1.10.BEVとFCEVの価格と航続距離の比較 1.11.2023年の欧州eLCV販売台数 - BEVがFCEVをリード 1.12.中国のNEV eLCV販売台数 2017-2023 1.13.BEVとFCEV LCVモデルのコストと航続距離のベンチマーク 1.14.燃料電池小型商用車の展望 1.15.2021~2024年における地域別トラックモデルの在庫 1.16.ゼロエミッションの中型・大型トラックの範囲 1.17.BEV と FCEV トラックのアップフロントコスト 1.18.FCEV トラックの水素消費量 - OEM ベンチマーキング 1.19.大型トラックの CO₂ 排出量:FCEV, BEV & Ice 1.20.バッテリートラックと燃料電池トラックの比較:航続距離 1.21.燃料電池バスの見通し 1.22.FCEV と BEV の 1 回充電/燃料補給時の航続距離予測:2025-2044 1.23.中国における BEV 対 FCEV バスの販売台数 1.24.欧州におけるバス登録台数、FCEB、BEB、PHEV 2013-2023 1.25.2023-2045 年の FCEV 車種別販売台数予測(台) 1.26.2045 年の FCEV 対 BEV 市場シェア 2.序論 2.1.運輸脱炭素化のコアドライバー 2.2.増加する輸送機関の排出量 2.3.交通機関の温室効果ガス排出量:中国、米国、欧州 2.4.都市の大気質 2.5.大気の質の悪化は早死を招く 2.6.化石燃料の使用禁止:解説 2.7.化石燃料の使用禁止(都市) 2.8.ICEの代替 - ゼロエミッション電気自動車 2.9.燃料電池自動車とは? 2.10.燃料電池自動車の魅力 2.11.燃料電池の輸送用途 2.12.トヨタ・モビリティ・ロードマップ 2.13.なぜ水素燃料電池自動車が注目されているのか? 2.14.水素エコノミーの一環としての燃料電池車 2.15. 燃料電池車プロトタイプの30年 2.16.水素燃料電池車の導入障壁 2.17.BEVとFCEVのシステム効率 2.18.課題:グリーン水素のコスト削減 2.19.マイルあたりの燃料コストFCEV、BEV、氷 2.20.2023年の1マイルあたりの燃料コスト 2.21.FCEVコスト削減のための大量生産 2.22.ゼロ・エミッション車:BEVブーム 2.23.改善するリチウムイオン電池と競合する FCEV 3.燃料電池:技術概要 3.1.はじめに 3.1.1.燃料電池とは何か? 3.1.2.燃料電池の種類の概要 3.2.PEMFC技術と材料 3.2.1.PEMFCの動作原理 3.2.2.PEMFCの組み立てと材料 3.2.3.ガス拡散層の役割 3.2.4.バイポーラプレートの概要 3.2.5.BPPの材料:グラファイトと金属 3.2.6.ガス拡散層の目的と構造 3.2.7.トヨタ燃料電池 3.2.8.膜:目的とフォームファクター 3.2.9.市場をリードする膜材料ナフィオン 3.2.10.PFAS規制と電解槽 3.2.11.触媒:触媒の目的と形状 3.2.12.燃料電池触媒の動向 3.3.SOFC技術・材料 3.3.1.SOFCの動作原理 3.3.2.SOFCの組み立てと材料 3.4.SOFC搭載車 3.4.1.フォルクスワーゲン 3.4.2.日産自動車 3.4.3.無人車両 3.4.4.補助動力装置 3.4.5.WeichaiとCeres Power 3.4.6.SOFC搭載車の展望 4.水素製造 4.1.はじめに 4.1.1.水素バリューチェーンの概要 4.1.2.水素はどのセクターを脱炭素化できるか? 4.1.3.水素アプリケーションの概要 4.1.4.水素産業の現状 4.1.5.水素需要の現状 4.1.6.水素開発を推進する主な法律と資金調達メカニズム 4.1.7.水素の色 4.1.8.SMRを用いた従来の灰色水素製造 4.1.9.水素製造からのCO₂ 排出量の除去 4.1.10.なぜグリーン水素が必要なのか? 4.1.11.グリーン水素:主な電解槽技術 4.1.12.電解槽企業-主要プレーヤー 4.1.13.FIDを実施または建設中の主なグリーン水素プロジェクト 4.1.14.グリーン水素の商業的進展 4.1.15.電解槽市場の将来動向 4.1.16.グリーン水素市場の重要な競合要因 4.1.17.ブルー水素製造 - CCUSを用いたSMR 4.1.18.ブルー水素:主な合成ガス製造技術 4.1.19.ATR&POXからのCO₂回収は容易 4.1.20.最終投資決定(FID)に達した主なブルー水素プロジェクト 4.1.21.ブルー水素の商業的進展 4.1.22.開発段階別の水素製造プロセス 4.1.23.各種水素のコスト比較 4.1.24.平準化水素製造コスト(LCOH) - グリーン水素 4.1.25.グリーン水素の LCOH の地域差 4.1.26.グリーン水素製造の課題 4.1.27.ブルー水素製造のケース 4.1.28.ブルー水素製造プロセスの比較と要点 4.2.FCEV への水素充填 4.2.1.水素の純度要件 4.2.2.水素流通の概要 4.2.3.水素ステーション(HRS) 4.2.4.水素のエネルギー密度 4.2.5.水素の輸送 4.2.6.圧縮・低温貯蔵・流通の問題点 4.2.7.水素の輸送 4.2.8.世界の水素充填インフラの現状(1/2) 4.2.9.世界の水素充填インフラの現状(2/2) 4.2.10.欧州の水素ステーション 4.2.11.欧州の水素ステーション(2) 4.2.12.アメリカの水素ステーション 4.2.13.アメリカの水素ステーション(2) 4.2.14.中国の水素ステーション 4.2.15.日本と韓国の水素ステーション 4.2.16.代替水素充填コンセプト 4.2.17.クリーン・エネルギー・パートナーシップ 4.2.18.ポンプでの水素コスト(1/2) 4.2.19.ポンプでの水素コスト (2/2) 4.2.20.LIFTE H2: より高圧の輸送が必要 4.2.21.LIFTE H2:移動式H2燃料補給機の方が競争力がある 4.2.22.オランダの水素ネットワークへの資金提供 4.2.23.インフラのコスト 4.2.24.水素充填インフラの開発 4.2.25.水素 FCEV - エアプロダクツ、ハイビア、ルノー 4.3.FCEV における水素貯蔵 4.3.1.圧縮水素貯蔵 4.3.2.水素貯蔵タンク 4.3.3.圧縮貯蔵容器の分類 4.3.4.構造材料 4.3.5.タイプ3・4タンクの用途 4.3.6.タイプ 3 & 4 技術におけるプレーヤー 4.3.7.FCEV 車載用水素タンク 4.3.8.FCEV 車載水素タンクサプライヤー 4.3.9.液体水素(LH2) 4.3.10.FCEV 車載用 LH2 タンク 4.3.11.極低温圧縮水素貯蔵(CcH2) 4.3.12.BMW の低温圧縮貯蔵タンク 4.3.13.IDTechExの水素研究ポートフォリオ 5.燃料電池乗用車 5.1.はじめに 5.1.1.燃料電池乗用車の展望 5.1.2.燃料電池乗用車 5.1.3.燃料電池乗用車のコンポーネント 5.1.4.FCEV 車の動作モード 5.1.5.燃料電池車のモデル 5.1.6.燃料電池乗用車の成長、停滞、衰退 5.1.7.FCEV 車市場シェア トヨタ、現代自動車、ホンダ、2016 年~2024 年 5.1.8.水素:排出ガスとコストの問題 5.1.9.パワートレインのテールパイプ排出量比較 5.2.燃料電池乗用車のプレーヤー、販売台数、ベンチマーク 5.2.1.トヨタ燃料電池乗用車の歴史 5.2.2.トヨタの電動化ロードマップ 5.2.3.トヨタMIRAI第1世代2015 5.2.4.トヨタMIRAI第1世代コンポーネンツ 5.2.5.トヨタミライ第2世代 5.2.6.トヨタミライ第2世代大幅改良 5.2.7.トヨタ ミライ 第2世代H2 安全対策 5.2.8.購入インセンティブ過去の5.2.9.2024年と2025年の購入インセンティブ 5.2.10.トヨタミライ販売台数 2014-2024 5.2.11.FCEV の設備投資の減少 5.2.12.プリウスに続くトヨタFCEV 5.2.13.トヨタミライのデモカー 5.2.14.トヨタFCEVの2024年以降の目標 5.2.15.トヨタ燃料電池ピックアップトラック 5.2.16.ヒュンダイ燃料電池乗用車の歴史 5.2.17.ヒュンダイFCEVの改良 5.2.18.ヒュンダイNEXO SUV 5.2.19.ヒュンダイNEXOコンポーネント 5.2.20.ヒュンダイNEXO水素タンク 5.2.21.ヒュンダイFCEVの目標 5.2.22.ヒュンダイ、フォルツェ水素レーシングと提携 5.2.23.ヒュンダイ N ビジョン 74:ローリングラボ 5.2.24.ヒュンダイ NEXO 販売 2018-2024 5.2.25.2021 年からの韓国補助金インセンティブ:FCEV を後押しするも、BEV が大きく先行 5.2.26.2023年以降の韓国補助金の推移 5.2.27.ホンダ クラリティ フューエルセル 5.2.28.ホンダFCEV開発スケジュール 5.2.29.ホンダ クラリティ FCEV コンポーネント 5.2.30.ホンダ、FCクラリティを廃止:需要の低迷 5.2.31.ホンダ、FCEV市場に再参入 5.2.32.ホンダ CR-V e:FCEV 5.2.33.BMW、FCEVを生産 5.2.34.BMW iX5 ハイドロジェン 5.2.35.ルノー・日産の燃料電池開発 5.2.36.日産e-Bio SOFCシステム 5.2.37.日産e-NV200 SOFCバイオエタノール試作車 5.2.38.ルノー、シーニックでFCEVに復帰 5.2.39.ゼネラルモーターズの燃料電池開発 5.2.40.GMハイドロテック燃料電池の進化 5.2.41.GM Pathway "An All Electric Future" 5.2.42.ダイムラー メルセデス・ベンツ GLC F-CELL 5.2.43.メルセデス・ベンツGLC F-CELLのコンポーネント 5.2.44.メルセデス・ベンツGLC F-CELLの動作モード 5.2.45.メルセデスのFCEVカー開発終了 5.2.46.フォルクスワーゲングループFCEV乗用車の開発中止 5.2.47.フォルクスワーゲン・グループ - 燃料としてのH2効率の悪さ 5.2.48.VW、クラフトワークと燃料電池車開発 5.2.49.アウディ、FCEV開発を断念 5.2.50.アウディA7スポーツバックHトロン 5.2.51.リバーシンプル高効率シティ FCEV 5.2.52.中国のFCEV車 5.2.53.商用車にフォーカスする中国 FCEV 5.2.54.乗用車をターゲットとする中国 FCEV 5.2.55.発表された中国のFCEV車 5.2.56.上海汽車のFCEVパイオニア 5.2.57.上海汽車 - 大衆向けFC MPV 5.2.58.長安ディープブルーSL03:中国初の量産FCカー 5.2.59.各社のFCEVに対する考え方 5.2.60.FCEV 水素消費量ベンチマーク 5.2.61.FCEV 車の燃料サイズのベンチマーク 5.3.燃料電池乗用車の障壁 5.3.1.BEV 車と FCEV 車の価格と航続距離の比較 5.3.2.FC 車の燃料補給/充電の優位性? 5.3.3.欧州で水素ステーションが減少? 5.3.4.乗用車のCO₂排出量 - H2ICE, FCEV, BEV & 化石燃料 5.3.5.発電によるCO₂排出量 5.3.6.給油コスト ガソリン vs 水素 5.3.7.FCEVの燃料費とBEVの充電費 5.3.8.テスラ、燃料電池に興味なし 5.3.9.中国におけるパワートレイン技術別の自動車排出量 5.3.10.FCEV車の結論 5.3.11.なぜ燃料電池車なのか? 6.燃料電池小型商用車 6.1.はじめに 6.1.1.小型商用車の定義 6.1.2.LCVセクターからのCO₂排出量 6.1.3.電気LCV:ドライバーと障壁 6.1.4.BEV と FCEV LCV の採用に関する考察 6.1.5.欧州 eLCV 販売 2023 - BEV が FCEV をリード 6.1.6.中国のNEV eLCV販売台数 2017-2023 6.1.7.LCV の航続距離要件 6.1.8.航続距離に関する考察 6.1.9.トラックと比較したLCVの航続距離要件 6.1.10.燃料電池LCV 6.1.11.グリーン LCV 用燃料電池にはグリーン水素が必要 6.1.12.BEV と FCEV の効率比較 6.1.13.フリートは FCEV を必要とするか? 6.1.14.BEV eLCV に移行する日本と韓国の OEM 6.1.15.BEV と FCEV の比較 6.2.燃料電池小型商用車:プレーヤーとベンチマーク 6.2.1.燃料電池LCVの仕様例 6.2.2.ルノーグループ 6.2.3.ルノー水素システム図 6.2.4.HYVIA-ルノーとプラグパワー社のFC-LCV合弁事業 6.2.5.ステランティスの燃料電池LCV 6.2.6.ステランティス - シトロエン/プジョー/ボクスホール/オペルFCバン 6.2.7.シンビオ燃料電池システム 6.2.8.フォルシアとシンビオ 6.2.9.バラードとリナマーの小型燃料電池アライアンス 6.2.10.燃料電池電気バン - ホルトハウゼン 6.2.11.中国におけるボッシュの燃料電池の進展 6.2.12.ボクスホール・ヴィヴァーロとモヴァーノ・ハイドロジェン - そして将来のステランティスFCEV 6.2.13.ハイヴィア・ルノー・マスターH2テック 6.2.14.初の水素 6.2.15. 水素トヨタ・ハイラックス試作車 6.2.16.燃料電池LCVのこれまでの試み 6.2.17.水素燃焼LCVの孤立した開発 6.2.18.BEV と FCEV LCV モデルのコストと航続距離のベンチマーク 6.2.19.燃料電池 LCV に関する IDTechEx の見通し 7.燃料電池電気トラック 7.1.はじめに 7.1.1.燃料電池トラックの展望 7.1.2.排気ガスゼロ(またはゼロに近い)トラックの台頭 7.1.3.トラック重量の定義 7.1.4.BEV と FCEV のシステム効率 7.1.5.新型トラックの燃料/CO₂ 規制 7.1.6.EU 排出量目標の詳細 7.1.7.EU の大型トラック電動化スケジュール 7.1.8.EUの大型トラック排出量目標はどの程度達成可能か? 7.1.9.EUの大型トラック排出量目標はどの程度達成可能か?(2) 7.1.10.米国のトラック排出基準 7.1.11.米国のクレジット制度 7.1.12.BEV と FCEV トラックのアップフロントコスト 7.1.13.燃料電池技術の比較 7.1.14.燃料電池企業の状況 7.1.15.トラック重量別のバッテリー搭載容量 7.1.16.燃料電池の出力と車両重量の比較 - OEMベンチマーキング 7.1.17.燃料電池のエネルギー密度の優位性 7.1.18.バッテリートラックと燃料電池トラックの比較:航続距離 7.1.19.1日の負荷サイクル需要 7.1.20.大型車燃料電池システムのコスト 7.1.21.課題グリーン H2 のコスト削減 7.1.22.FCEV がグリーンであるためにはグリーン H2 が必要 7.1.23.グリーン水素価格開発予測 7.1.24.グリーン水素の製造コスト 7.1.25.電力源別グリーン水素コスト 米国/欧州 7.1.26.削減された電力を利用する電解槽 7.1.27.水素燃料コストとディーゼル燃料コストの比較 7.1.28.FCEV トラックの水素消費量 - OEM ベンチマーキング 7.1.29.欧州における再生可能水素コスト予測 7.1.30.燃料電池トラックへの補助金 7.1.31.インフレ抑制法の FCEV トラックへの潜在的影響 7.1.32.FCEV トラックにおける燃料電池メーカーの協力 7.1.33.トラックに関する燃料電池メーカーの買収 7.2.燃料電池トラックのプレーヤー 7.2.1.燃料電池トラックの仕様例 7.2.2.燃料電池トラックヒュンダイ 7.2.3.米国XCIENTの航続距離 7.2.4.市販可能なヒュンダイの燃料電池トラック 7.2.5.現代水素モビリティ 7.2.6.ヒュンダイ XCIENT 中国の受注 7.2.7.燃料電池トラックダイムラー/ボルボ 7.2.8.メルセデス・ベンツ(ダイムラー)のトラック試験運用 2024年 7.2.9.ボルボ・グループ脱化石燃料輸送に向けて 7.2.10.燃料電池トラックの開発を続けるスカニア 7.2.11.ホライゾン燃料電池テクノロジー 7.2.12.HYZON Motors 7.2.13.HYZON Motorsの大型トラック概略図 7.2.14.ニコラ・コーポレーション 7.2.15.ニコラ、2025年2月に破産申請 7.2.16.ニコラ・モーターBEVとFCEV 7.2.17.燃料電池トラックケンワース(PACCAR) 7.2.18.燃料電池メーカーの例 米国のFCトラック 7.2.19.燃料電池トラックトヨタ/日野 7.2.20.VDLとトヨタが初のFCEVトラックを発表 7.2.21.燃料電池トラック東風 7.2.22.いすゞとホンダの燃料電池トラック 7.2.23.BOSAL/Ceres Power - SOFCレンジエクステンダー 7.2.24.バラード・モティブ・ソリューションズ 7.2.25.バラード・トラックのパートナーシップ 7.2.26.中国の燃料電池トラック販売 2018-2024 7.2.27.中国の FCEV サポート 7.2.28.中国の水素ステーション 7.2.29.中国のFCEV普及はグリーンか? 7.2.30.中国の燃料電池ダンプトラック 7.2.31.SANY 燃料電池トラック 7.2.32.中国の燃料電池設置容量 2024年 7.2.33.その他の中国の燃料電池プレーヤー 7.2.34.聯合燃料電池系統開発(北京)有限公司 7.2.35.水素トラック燃料補給ガイド 7.2.36.水素燃料補給インフラの開発 7.2.37.燃料電池トラック燃料補給の利点 7.2.38.長距離トラック輸送のチャンス? 7.2.39.燃料電池トラックは FCEV の普及を促進する 7.2.40.効率の根本的問題 8.燃料電池バス 8.1.はじめに 8.1.1.燃料電池バス - 新市場が低調な販売を押し上げる可能性 8.1.2.FCB開発の30年 8.1.3.燃料電池バスの主な利点/欠点 8.1.4.燃料電池バスの概略図 8.1.5.燃料電池バスの仕様例 8.1.6.その他のゼロ/低排出ガスバス・オプション 8.1.7.市場のギャップ:燃料電池バスの展望 8.1.8.バッテリー電気バス:ライバルか補完か? 8.1.9.BEV と FCEV の共存は可能か? 8.1.10.インフラコスト BEV vs FCEV バスデポ 8.1.11.分析例:例分析:カリフォルニア州フットヒル・トランジット 486 番線 8.1.12.分析例フットヒル・トランジット 8.1.13.必要な走行距離の提供 8.1.14.カリフォルニア州交通機関の走行距離分布 8.1.15.BEV と FCEV のランニングコストと効率 8.1.16.ゼロエミッションバスの 1 日あたりの走行距離 8.1.17.1 日あたりのゼロエミッションバス走行距離 8.1.18.BEV バスに適した路線の長さ 8.1.19.バッテリーの改善により、燃料電池バスは時代遅れになるのか? 8.1.20.ループエナジー社 8.1.21.水素燃料コストとディーゼル燃料コストの比較 8.2.FCバス:地域別性能、コスト、プレーヤー 8.2.1.FCEBバスの世界展開 8.2.2.中国の燃料電池バスOEM市場シェア 2023年 8.2.3.中国の燃料電池バスの事例 8.2.4.NEV バスの販売 - BEB、PHEB、FCEB 8.2.5.中国の電気バスOEMと市場シェア 8.2.6.中国の燃料電池設置容量 2024年 8.2.7.CEMT - Edelman Hydrogen Energy Equipment 8.2.8.北京サイノハイテック 8.2.9.シノシナジー 8.2.10.上海水素推進技術 8.2.11.REFIRE - Shanghai Reshaping Energy Technology 8.2.12.REFIRE - Shanghai Reshaping Energy Technology 8.2.13.その他の中国燃料電池システムメーカー 8.2.14.聯合燃料電池(北京)有限公司 8.2.15.トヨタSORA燃料電池バス 8.2.16.トヨタ燃料電池バスの構造 8.2.17.日本 - 燃料電池の目標 8.2.18.ヒュンダイ ELEC CITY 燃料電池バス 8.2.19.イヴェコ燃料電池バス(現代燃料電池) 8.2.20.韓国-FCEB目標 8.2.21.米国の燃料電池バスアクティブ燃料電池バスプロジェクト 8.2.22.米国の燃料電池バス計画中の燃料電池バスプロジェクト 8.2.23.米国の燃料電池バス完了した燃料電池バスプロジェクト 8.2.24.米国のバス車両のゼロ・エミッションバスへの移行 8.2.25.米国バス車両のゼロ・エミッション移行コスト 8.2.26.米国の燃料電池バス:価格 2010-2025 8.2.27.米国のバス:ドライブトレイン別設備投資コスト 2015-2023 8.2.28.米国のバス:パワートレイン別コスト:2023~2025年 8.2.29.NREL 燃料電池バスの評価 2023年 8.2.30.NREL 燃料電池バスの評価 2023年 8.2.31.燃料電池バスの長期スタック性能データ 8.2.32.NREL:燃料電池バスと CNG バスの比較 8.2.33.ニューフライヤー・エクセルシオ CHARGE H2 8.2.34.エルドラド・ナショナルAXESS燃料電池バス 8.2.35.エルドラド・ナショナルAXESS概略図 8.2.36.ヴァンフール 8.2.37.米国のスクールバス 8.2.38.米国eBus購入補助金 8.2.39.米国の燃料電池バスと水素ステーション補助金 2024 8.2.40.欧州の燃料電池バス普及 8.2.41.EU JIVE 2の目標 8.2.42.欧州連合の燃料電池バス市場 8.2.43.欧州のバス登録台数, FCEB, BEB, PHEV, 2013-2023 8.2.44.欧州クリーンバス普及イニシアティブ 8.2.45.水素バスの受注キャンセル 8.2.46.ソラリスUrbino 12 水素バス 8.2.47.ソラリスの代替ドライブ販売と戦略 8.2.48.ソラリス - バラード燃料電池の記録的受注 8.2.49.カエターノバスH2.シティゴールド 8.2.50.トヨタモーターヨーロッパ 8.2.51.1000km 水素バス 8.2.52.SAFRA Businova Hydrogen 8.2.53.ライトバス ストリートデッキ ハイドロライナー 8.2.54.ヴァン・フールEU受注 8.2.55.ADL Enviro400 FCEV 8.2.56.FCEB H2 消費ベンチマーク 9.予測サマリー 9.1.はじめに 9.1.1.予測の前提 9.2.予測サマリー:乗用車 9.2.1.前回からの FCEV 車予測変更の説明 9.2.2.予測の前提 9.2.3.燃料電池車予測 9.2.4.FCEV 車の地域別販売台数予測 2021-2045 (台) 9.2.5.FCEV 車の地域別燃料電池需要予測 2021-2045 (GW) 9.2.6.FCEV 車の地域別電池需要予測 2021-2045 (MWh) 9.2.7.FCEV 車の地域別市場規模予測 2021-2045 (US$) 9.3.予測概要:小型商用車 9.3.1.予測の前提 9.3.2.FCEV LCV 地域別販売台数予測 2023-2045 (台) 9.3.3.FCEV LCV 地域別燃料電池需要予測 2023-2045 (GW) 9.3.4.FCEV LCV 地域別市場価値予測 2023-2045 (US) 9.3.5.FCEV LCV 地域別電池需要予測 2023-2045 (MWh) 9.4.予測概要:トラック 9.4.1.予測の前提 9.4.2.2020-2045 年の FCEV 及び MDT 総販売台数予測(台) 9.4.3.FCEV MDT 地域別販売台数予測 2020-2045 (台) 9.4.4.中型 FC トラック燃料電池需要 9.4.5.FCEV MDT 地域別電池需要予測 2020-2045 (GWh) 9.4.6.2020-2045 年の FCEV MDT 地域別市場価値予測(US$) 9.4.7.2020-2045 年の FCEV 及び HDT 合計販売台数予測(台) 9.4.8.FCEV HDT 地域別販売台数予測 2020-2045 (台) 9.4.9.FCEV HDT 燃料電池地域別需要予測 2020-2045 (GW) 9.4.10.FCEV HDT 地域別バッテリー需要予測 2020-2045 (GWh) 9.4.11.2020-2045 年の FCEV HDT 地域別市場価値予測(US$) 9.5.予測概要:バス 9.5.1.予測の前提 9.5.2.FCEV バスの地域別販売台数予測 2020-2045 (台) 9.5.3.FCEV バスの地域別燃料電池需要予測 2020-2045 (MW) 9.5.4.FCEV バスの地域別バッテリー需要予測 2024-2045 (MWh) 9.5.5.FCEV バスの地域別市場規模 2024-2045 年予測(US$) 9.6.予測概要:オンロード FC 自動車全体 9.6.1.FCEV 地域別販売台数予測 2023-2045 (台) 9.6.2.FCEV 燃料電池地域別需要予測 2023-2045 (GW) 9.6.3.FCEV 電池地域別需要予測 2023-2045 (GWh) 9.6.4.FCEV 地域別市場規模予測 2020-2045 (US$) 9.6.5.FCEV 販売台数の車種別予測 2023-2045 9.6.6.2045 年の FCEV 対 BEV 市場シェア 9.6.7.FCEV 燃料電池の車両タイプ別需要予測 2023-2045 (GW) 9.6.8.2024-2045 年 FCEV 車種別バッテリー需要予測(GWh) 9.6.9.FCEVの車両タイプ別市場価値予測 2023-2045 (US$)

Summary

この調査レポートは、自動車、小型商用車、中型・大型トラック、バスなどのオンロード燃料電池電気自動車(FCEV)市場を調査しています。

主な掲載内容(目次より抜粋)

Report Summary

IDTechEx's report "Fuel Cell Electric Vehicles 2025-2045: Markets, Technologies, Forecasts" explores the market for on-road fuel cell electric vehicles (FCEVs), including cars, light commercial vehicles, medium- and heavy-duty trucks, and buses. The report covers the market drivers, barriers, players, technology, models, benchmarking, and forecasts adoption for the next 20 years for unit sales, fuel cell demand, battery demand, and market value.

Fuel cell electric vehicles are powered by a fuel cell stack, which generates electrical power through the reaction between stored hydrogen and oxygen from the air. With the only side product being water, fuel cell vehicles are a zero-emissions solution, just like battery-electric vehicles.

Fuel Cell Passenger Cars

However, the past two years have shown a fall in interest in fuel-cell cars. IDTechEx puts this down to multiple factors, the key ones being expensive and unreliable hydrogen refueling stations, the continued progress of BEVs, and the lack of model availability. Despite fuel and purchase subsidies reducing the price of fuel cell cars by approximately 50% or even more in regions such as California and South Korea, annual sales have decreased by approximately two-thirds, from 15,000 in 2022 to only 5,000 by 2024. Meanwhile, battery electric vehicles (BEVs) and plug-in hybrids (PHEVs) sold over 10 million and 4 million units respectively. Despite the second successive year of market shrinkage, IDTechEx forecasts fuel cell passenger car sales to slowly recover as national investments in green hydrogen projects and hydrogen refueling stations begin to bear fruit. As a result of delays, lack of sales, and project cancellations, IDTechEx has adjusted its forecast for fuel cell passenger cars downwards from its previous edition.

Global sales progress of FC cars. The past two years have shown a significant drop from earlier growth, but IDTechEx does forecast sales to recover. Full data and forecasts to 2045 are available in "Fuel Cell Electric Vehicles 2025-2045: Markets, Technologies, Forecasts".

Fuel Cell Light Commercial Vehicles

In most regions, passenger cars drive shorter journeys than commercial vehicles, which often take fixed routes, some of which are long-haul journeys. However, light commercial vehicles are another segment where the rapid improvement of BEVs has left FCEVs lagging behind. In most regions, FCEVs remain in demonstration fleets and prototype phases. China is the largest fuel cell LCV market, where in 2023, approximately 1,300 sales were recorded. However, approximately 50,000 BEVs were sold in the same year.

Fuel Cell Buses and Trucks

Electric buses are rapidly becoming commonplace worldwide. However, being heavier than light commercial vehicles and passenger cars, the weight and cost of the battery can be an issue. Buses can reduce the size and weight of the battery with a fuel cell stack: hydrogen tanks and the fuel cell can provide some proportion of the power and energy necessary for the vehicle to operate within the required periods.

Relationship between gross vehicle weight rating (GVWR) of an FCEV and the power of the fuel cell stack required. Full data is available in "Fuel Cell Electric Vehicles 2025-2045: Markets, Technologies, Forecasts".

Medium- and heavy-duty trucks are on the heavier side of the automotive sector, both in terms of carried loads and duty cycles. Zero-emissions trucks continue to be a fast-moving environment, and fuel cell truck companies have been no exception. Nikola, Quantron, and Hyzon have all encountered significant financial obstacles in the past year, but trucks remain the vehicle segment that IDTechEx believes will eventually experience the most market penetration from FCEVs. The USA's National Zero-Emission Freight Corridor Strategy involves the building of a network of hydrogen refueling stations to support freight transportation by 2040, and China continues to sell thousands of fuel cell trucks yearly, accompanied by a targeted 1,200 hydrogen refueling stations by the end of 2025.

Similar to buses, trucks with fixed routes mean that refueling infrastructure can be focused at key hubs and centers. This, combined with the current limitations of BEVs in range and weight, means that there is an opportunity in the truck market for FCEVs. Battery electric trucks currently struggle to meet the harshest demands of heavy-duty, long-haul trucking, a potential area of growth. While the total cost of ownership (TCO) remains high for fuel cell trucks, production costs will eventually come down with economies of scale, and refueling will become more cost-effective once green hydrogen projects are completed and begin producing hydrogen fuel in volume.

This IDTechEx report covers all the main FCEV segments, providing holistic coverage of the market. In addition to market updates and technology analysis and benchmarking, there is also coverage on the materials for fuel cells, including PFAS concerns newly in this report, as well as the whole hydrogen supply chain, from production to refueling stations. Hydrogen refueling infrastructure will have a massive part to play in any progress of the FCEV market, with this report covering the key regions (China, the US, Europe, the Rest of the World - primarily Japan and South Korea) and supply chain analysis. Granular forecasts are included, split by region and vehicle segment, including unit sales, market value (US$), fuel cell power demand (GW), and battery energy demand (GWh).

Key aspects

This report provides an extensive overview of fuel cell electric vehicle markets including cars, medium and heavy-duty trucks, buses, and light commercial vehicles, including:

Table of Contents

1. EXECUTIVE SUMMARY

1.1. Report Overview

1.2. What is a Fuel Cell Vehicle?

1.3. Attraction of Fuel Cell Vehicles

1.4. Deployment Barriers for Hydrogen Fuel Cell Vehicles

1.5. The Hydrogen Economy

1.6. The Colors of Hydrogen

1.7. System Efficiency Between BEVs and FCEVs

1.8. Outlook for Fuel Cell Passenger Cars

1.9. Growth, Stagnation, and Fall of Fuel Cell Passenger Cars

1.10. Price and Range Comparison of BEV and FCEV Cars

1.11. Europe eLCV Sales 2023 - BEV Leads FCEV

1.12. China NEV eLCV Sales 2017-2023

1.13. Cost and Range Benchmark of BEV and FCEV LCV Models

1.14. Outlook for Fuel Cell Light Commercial Vehicles

1.15. Regional Truck Model Availability 2021-2024

1.16. Range of Zero Emission Medium and Heavy Trucks

1.17. Up Front Costs of BEV and FCEV Trucks Progression

1.18. FCEV Truck Hydrogen Consumption - OEM Benchmarking

1.19. Heavy-Duty Truck CO₂ Emissions: FCEV, BEV & ICE

1.20. Battery vs Fuel Cell Trucks: Driving Range

1.21. Outlook for Fuel Cell Buses

1.22. FCEV and BEV Range on a Single Charge/Refuel Forecast: 2025-2044

1.23. BEV vs FCEV Bus Sales in China

1.24. Bus Registrations, FCEB, BEB, PHEV in Europe 2013-2023

1.25. FCEV Sales Forecast by Vehicle Type 2023-2045 (units)

1.26. FCEV vs BEV Market Share in 2045

2. INTRODUCTION

2.1. The Core Driver for Transport Decarbonization

2.2. Transport Emissions Rising

2.3. Transport GHG Emissions: China, US & Europe

2.4. Urban Air Quality

2.5. Poor Air Quality Causes Premature Deaths

2.6. Fossil Fuel Bans: Explained

2.7. Fossil Fuel Bans (Cities)

2.8. Replacement for ICE - Zero Emission Electric Vehicles

2.9. What is a Fuel Cell Vehicle?

2.10. Attraction of Fuel Cell Vehicles

2.11. Transport Applications for Fuel Cells

2.12. Toyota Mobility Roadmap

2.13. Why is the Focus on Hydrogen Fuel Cell Vehicles?

2.14. Fuel Cell Vehicles as a Part of the Hydrogen Economy

2.15. 30 Years of Fuel Cell Vehicle Prototypes

2.16. Deployment Barriers for Hydrogen Fuel Cell Vehicles

2.17. System Efficiency Between BEVs and FCEVs

2.18. The Challenge: Green Hydrogen Cost Reduction

2.19. Fuel Cost per Mile: FCEV, BEV, ICE

2.20. Fuel Cost per Mile 2023

2.21. Volume Production to Decrease FCEV Cost

2.22. Zero Emission Vehicles: BEV Booming

2.23. FCEV Competing with Improving Li-ion Batteries

3. FUEL CELLS: TECHNOLOGY OVERVIEW

3.1. Introduction

3.1.1. What is a Fuel Cell?

3.1.2. Overview of Fuel Cell Types

3.2. PEMFC Technology & Materials

3.2.1. PEMFC Working Principle

3.2.2. PEMFC Assembly and Materials

3.2.3. Role of the Gas Diffusion Layer

3.2.4. Bipolar Plates Overview

3.2.5. Materials for BPPs: Graphite vs metal

3.2.6. Gas diffusion layer purpose and structure

3.2.7. Toyota Fuel Cell

3.2.8. Membrane: Purpose and form factor

3.2.9. Market leading membrane material: Nafion

3.2.10. PFAS Regulations Affecting PEM Fuel Cells & Electrolyzers

3.2.11. Catalyst: Purpose and form factor

3.2.12. Trends for fuel cell catalysts

3.3. SOFC Technology & Materials

3.3.1. SOFC working principle

3.3.2. SOFC assembly and materials

3.4. SOFC-Powered Vehicles

3.4.1. Volkswagen

3.4.2. Nissan

3.4.3. Unmanned vehicles

3.4.4. Auxiliary power units

3.4.5. Weichai and Ceres Power

3.4.6. Outlook for SOFC powered vehicles

4. HYDROGEN PRODUCTION

4.1. Introduction

4.1.1. Hydrogen Value Chain Overview

4.1.2. Which sectors could hydrogen decarbonize?

4.1.3. Overview of hydrogen applications

4.1.4. State of the hydrogen industry

4.1.5. State of hydrogen demand today

4.1.6. Key legislation & funding mechanisms driving hydrogen development

4.1.7. The colors of hydrogen

4.1.8. Traditional Grey Hydrogen Production Using SMR

4.1.9. Removing CO₂ emissions from hydrogen production

4.1.10. Why is green hydrogen needed?

4.1.11. Green hydrogen: main electrolyzer technologies

4.1.12. Electrolyzer companies - key players

4.1.13. Major Green H2 Projects With FIDs Made or Under Construction

4.1.14. Commercial progress of green hydrogen

4.1.15. Future trends of the electrolyzer market

4.1.16. Important competing factors for the green H2 market

4.1.17. Blue hydrogen production - SMR with CCUS

4.1.18. Blue hydrogen: main syngas production technologies

4.1.19. Capturing CO₂ from ATR & POX is easier

4.1.20. Major blue H2 projects reaching final investment decisions (FID)

4.1.21. Commercial Progress of Blue Hydrogen

4.1.22. Hydrogen production processes by stage of development

4.1.23. Cost comparison of different types of hydrogen

4.1.24. Levelized cost of hydrogen (LCOH) production - green hydrogen

4.1.25. Regional variations in LCOH of green hydrogen

4.1.26. Challenges in green hydrogen production

4.1.27. The case for blue hydrogen production

4.1.28. Blue H2 process comparison summary & key takeaways

4.2. Hydrogen Refueling for FCEVs

4.2.1. Hydrogen purity requirements

4.2.2. Overview of Hydrogen Distribution

4.2.3. Hydrogen refueling stations (HRS)

4.2.4. Energy density of hydrogen

4.2.5. Transporting Hydrogen

4.2.6. Problems with compressed & cryogenic storage & distribution

4.2.7. Transporting Hydrogen

4.2.8. State of hydrogen refueling infrastructure worldwide (1/2)

4.2.9. State of hydrogen refueling infrastructure worldwide (2/2)

4.2.10. Europe Hydrogen Refueling Stations

4.2.11. Europe Hydrogen Refueling Stations (2)

4.2.12. USA Hydrogen Refueling Stations

4.2.13. USA Hydrogen Refueling Stations (2)

4.2.14. China Hydrogen Refueling Stations

4.2.15. Japan and South Korea Hydrogen Refueling Stations

4.2.16. Alternative hydrogen refueling concepts

4.2.17. The Clean Energy Partnership

4.2.18. Cost of hydrogen at the pump (1/2)

4.2.19. Cost of hydrogen at the pump (2/2)

4.2.20. LIFTE H2: higher pressure transportation is needed

4.2.21. LIFTE H2: Mobile H2 refuelers are more competitive

4.2.22. Netherlands Funding a Hydrogen Network

4.2.23. Infrastructure Costs

4.2.24. Developing Hydrogen Refuelling Infrastructure

4.2.25. Hydrogen FCEVs - Air Products, Hyvia & Renault

4.3. Hydrogen Storage in FCEVs

4.3.1. Compressed Hydrogen Storage

4.3.2. Hydrogen Storage Tanks

4.3.3. Compressed Storage Vessel Classification

4.3.4. Construction materials

4.3.5. Applications for Type 3 & 4 tanks

4.3.6. Players in Type 3 & 4 technologies

4.3.7. FCEV onboard hydrogen tanks

4.3.8. Onboard FCEV Tank Suppliers

4.3.9. Liquid hydrogen (LH2)

4.3.10. LH2 tanks for onboard FCEV storage

4.3.11. Cryo-compressed hydrogen storage (CcH2)

4.3.12. BMW'S Cryo-compressed storage tank

4.3.13. IDTechEx's Hydrogen Research Portfolio

5. FUEL CELL PASSENGER CARS

5.1. Introduction

5.1.1. Outlook for Fuel Cell Passenger Cars

5.1.2. Fuel Cell Passenger Cars

5.1.3. Fuel Cell Passenger Car Components

5.1.4. FCEV Cars Operating Modes

5.1.5. Fuel Cell Car Models

5.1.6. Growth, Stagnation, and Fall of Fuel Cell Passenger Cars

5.1.7. FCEV Car Market Share Toyota, Hyundai, Honda, 2016-2024

5.1.8. Hydrogen: Emissions & Cost Issues

5.1.9. Powertrain Tailpipe Emissions Comparison

5.2. Fuel Cell Passenger Car Players, Sales, and Benchmarking

5.2.1. Toyota Fuel Cell Passenger Cars History

5.2.2. Toyota Roadmap for Electrification

5.2.3. Toyota Mirai 1st Gen 2015

5.2.4. Toyota Mirai 1st Gen Components

5.2.5. Toyota Mirai 2nd Generation

5.2.6. Toyota Mirai 2nd Gen. Significant Upgrades

5.2.7. Toyota Mirai 2nd Gen H2 Safety Measures

5.2.8. Purchase Incentives: Historical

5.2.9. Purchase Incentives 2024 and 2025

5.2.10. Toyota Mirai Sales 2014-2024

5.2.11. Decreasing CAPEX of FCEV

5.2.12. Toyota FCEV Following the Prius Pathway

5.2.13. Toyota Mirai Demonstrator Fleets

5.2.14. Toyota FCEV Goals 2024 and Beyond

5.2.15. Toyota Fuel Cell Pickup Truck

5.2.16. Hyundai Fuel Cell Passenger Car History

5.2.17. Hyundai FCEV Improvements

5.2.18. Hyundai NEXO SUV

5.2.19. Hyundai NEXO Components

5.2.20. Hyundai NEXO Hydrogen Tanks

5.2.21. Hyundai FCEV Goals

5.2.22. Hyundai Partners Forze Hydrogen Racing

5.2.23. Hyundai N Vision 74: A Rolling Lab

5.2.24. Hyundai NEXO Sales 2018-2024

5.2.25. Korea Subsidy Incentives from 2021: FCEV push but BEV far ahead

5.2.26. Korea Changing Subsidies for 2023 and beyond

5.2.27. Honda Clarity Fuel Cell

5.2.28. Honda FCEV Development Timeline

5.2.29. Honda Clarity FCEV Components

5.2.30. Honda Discontinue FC-Clarity: Weak Demand

5.2.31. Honda to Re-enter FCEV the Market

5.2.32. Honda CR-V e:FCEV

5.2.33. BMW to Produce FCEVs

5.2.34. BMW iX5 Hydrogen

5.2.35. Renault-Nissan Fuel Cell Development

5.2.36. Nissan e-Bio SOFC System

5.2.37. Nissan e-NV200 SOFC Bio-Ethanol Prototype

5.2.38. Renault Returns to FCEVs with Scenic

5.2.39. General Motors Fuel Cell Development

5.2.40. GM HYDROTEC Fuel Cell Evolution

5.2.41. GM Pathway "An All Electric Future"

5.2.42. Daimler Mercedes-Benz GLC F-CELL

5.2.43. Mercedes-Benz GLC F-CELL Components

5.2.44. Mercedes-Benz GLC F-CELL Operating Modes

5.2.45. Mercedes End FCEV Car Development

5.2.46. Volkswagen Group: No to FCEV Passenger Cars

5.2.47. Volkswagen Group - H2 Inefficiency as a Fuel

5.2.48. VW Fuel Cell Car Development with Kraftwerk

5.2.49. Audi Abandons FCEV Development

5.2.50. Audi A7 Sportback H-Tron

5.2.51. Riversimple: Highly Efficient City FCEV

5.2.52. Chinese FCEV Cars

5.2.53. China FCEV Focus on Commercial Vehicles

5.2.54. Some in China Still Targeting Passenger Cars

5.2.55. Announced Chinese FCEV Cars

5.2.56. SAIC China's FCEV Car Pioneer

5.2.57. SAIC - Mass Market FC MPV

5.2.58. Changan Deep Blue SL03: China's First Mass Produced FC Car

5.2.59. Attitude to FCEV Cars by Company

5.2.60. FCEV Hydrogen Consumption Benchmarking

5.2.61. FCEV Car Fuel Size Benchmarking

5.3. Fuel Cell Passenger Car Barriers

5.3.1. Price and Range Comparison of BEV and FCEV Cars

5.3.2. FC-Car Fueling / Charging Advantage?

5.3.3. Hydrogen Stations in Decline in Europe?

5.3.4. Passenger Car CO₂ Emissions - H2ICE, FCEV, BEV & Fossil Fuels

5.3.5. CO₂ Emission from Electricity Generation

5.3.6. Fueling Costs Petrol vs Hydrogen

5.3.7. Fueling FCEV Costs vs Charging BEVs

5.3.8. Tesla No Interest in Fuel Cells

5.3.9. Car Emissions by Powertrain Technology in China

5.3.10. FCEV Car Conclusions

5.3.11. Why Pursue Fuel Cell Cars?

6. FUEL CELL LIGHT COMMERCIAL VEHICLES

6.1. Introduction

6.1.1. Light Commercial Vehicles Definition

6.1.2. CO₂ emission from the LCV sector

6.1.3. Electric LCVs: Drivers and Barriers

6.1.4. Considerations for BEV and FCEV LCV Adoption

6.1.5. Europe eLCV Sales 2023 - BEV Leads FCEV

6.1.6. China NEV eLCV Sales 2017-2023

6.1.7. LCV Range Requirement

6.1.8. Range Considerations

6.1.9. LCV Range Requirement Compared to Trucks

6.1.10. Fuel Cell LCVs

6.1.11. Fuel Cells for Green LCVs Need Green Hydrogen

6.1.12. BEV vs. FCEV Efficiency

6.1.13. Do Fleets Need FCEVs?

6.1.14. Japanese & Korean OEMs Moving Towards BEV eLCVs

6.1.15. BEV and FCEV Comparison

6.2. Fuel Cell Light Commercial Vehicles: Players and Benchmarking

6.2.1. Example Fuel Cell LCV Specifications

6.2.2. Groupe Renault

6.2.3. Renault Hydrogen System Diagrams

6.2.4. HYVIA - Renault and Plug Power FC-LCV Joint Venture

6.2.5. Stellantis Fuel Cell LCVs

6.2.6. Stellantis - Citroen / Peugeot / Vauxhall / Opel FC-Van

6.2.7. Symbio Fuel Cell Systems

6.2.8. Faurecia and Symbio

6.2.9. Ballard and Linamar Light-Duty Fuel Cell Alliance

6.2.10. Fuel Cell Electric Vans - Holthausen

6.2.11. Bosch Fuel Cell Progress in China

6.2.12. Vauxhall Vivaro & Movano Hydrogen - and Future Stellantis FCEVs

6.2.13. Hyvia-Renault Master H2-Tech

6.2.14. First Hydrogen

6.2.15. Hydrogen Toyota Hilux Prototype

6.2.16. Previous Attempts at Fuel Cell LCVs

6.2.17. Isolated Developments in Hydrogen-Combustion LCVs

6.2.18. Cost and Range Benchmark of BEV and FCEV LCV Models

6.2.19. IDTechEx's Outlook on Fuel Cell LCVs

7. FUEL CELL ELECTRIC TRUCKS

7.1. Introduction

7.1.1. Fuel Cells Trucks Outlook

7.1.2. The Rise of Zero (or Near Zero) Exhaust Emission Trucks

7.1.3. Truck Weight Definitions

7.1.4. System Efficiency Between BEVs and FCEVs

7.1.5. Fuel/CO₂ Regulation for New Trucks

7.1.6. EU Emissions Targets in Detail

7.1.7. EU Timeline for Heavy Duty Truck Electrification

7.1.8. How Achievable are the EU Heavy Duty Trucks Emissions Targets?

7.1.9. How Achievable are the EU Heavy Duty Trucks Emissions Targets? (2)

7.1.10. US Truck Emissions Standards

7.1.11. US Credit System

7.1.12. Up Front Costs of BEV and FCEV Trucks Progression

7.1.13. Comparison of Fuel Cell Technologies

7.1.14. Fuel Cells Company Landscape

7.1.15. Installed Battery Capacity by Truck Weight

7.1.16. Fuel Cell Power vs Vehicle Weight - OEM Benchmarking

7.1.17. Fuel Cell Energy Density Advantage

7.1.18. Battery vs Fuel Cell Trucks: Driving Range

7.1.19. Daily Duty Cycle Demand

7.1.20. Heavy Duty Vehicle Fuel Cell System Costs

7.1.21. The Challenge: Green H2 Cost Reduction

7.1.22. Must be Green H2 for FCEV to be 'Green'

7.1.23. Green Hydrogen Price Development Forecasts

7.1.24. Green Hydrogen Production Costs US/EU

7.1.25. Green H2 Cost by Electricity Source US/EU

7.1.26. Electrolyzer Powered by Curtailed Electricity

7.1.27. Comparison Hydrogen Fuel Cost vs Diesel Cost

7.1.28. FCEV Truck Hydrogen Consumption - OEM Benchmarking

7.1.29. Renewable Hydrogen Cost Prediction in Europe

7.1.30. Subsidies Available to Fuel Cell Trucks

7.1.31. Potential Impact of Inflation Reduction Act on FCEV Trucks

7.1.32. Fuel Cell Manufacturers Collaboration on FC-Trucks

7.1.33. Fuel Cell Company Acquisitions Related to Trucks

7.2. Fuel Cell Truck Players

7.2.1. Fuel Cell Truck Example Specifications

7.2.2. Fuel Cell Trucks: Hyundai

7.2.3. US XCIENT Longer Range

7.2.4. Commercially Available Hyundai Fuel Cell Trucks

7.2.5. Hyundai Hydrogen Mobility

7.2.6. Hyundai XCIENT China Order

7.2.7. Fuel Cell Trucks: Daimler/Volvo

7.2.8. Mercedes-Benz (Daimler) Trucks Trial Operations 2024

7.2.9. Volvo Group: Toward Fossil Free Transport

7.2.10. Scania Still Developing Fuel Cell Trucks

7.2.11. Horizon Fuel Cell Technologies

7.2.12. HYZON Motors

7.2.13. HYZON Motors Heavy-Duty Truck Schematic

7.2.14. Nikola Corporation

7.2.15. Nikola Files For Bankruptcy February 2025

7.2.16. Nikola Motor: BEV and FCEV

7.2.17. Fuel Cell Trucks: Kenworth (PACCAR)

7.2.18. Example Fuel Cell Manufacturers US FC-Trucks

7.2.19. Fuel Cell Trucks: Toyota/Hino

7.2.20. VDL and Toyota Present First FCEV Truck

7.2.21. Fuel Cell Trucks: Dongfeng

7.2.22. Isuzu and Honda Fuel Cell Truck

7.2.23. BOSAL/Ceres Power - SOFC Range Extender

7.2.24. Ballard Motive Solutions

7.2.25. Ballard Truck Partnerships

7.2.26. Fuel Cell Truck Sales in China 2018-2024

7.2.27. Chinese FCEV Support

7.2.28. China Hydrogen Refuelling Stations

7.2.29. China's FCEV Deployment will it be Green?

7.2.30. Chinese Fuel Cell Dump Trucks

7.2.31. SANY Fuel Cell Trucks

7.2.32. China Fuel Cell Installed Capacity 2024

7.2.33. Other Chinese Fuel Cell Players

7.2.34. United Fuel Cell System R&D (Beijing) Co.

7.2.35. Guide to Hydrogen Truck Refuelling

7.2.36. Developing Hydrogen Refuelling Infrastructure

7.2.37. Fuel Cell Truck Refuelling Advantage

7.2.38. Long-Haul Trucking Opportunity?

7.2.39. Fuel Cell Trucks Facilitate Wider FCEV Deployment

7.2.40. The Fundamental Issue of Efficiency

8. FUEL CELL BUSES

8.1. Introduction

8.1.1. Fuel Cell Buses - New Markets May Boost Low Sales

8.1.2. 30 Years of FCB Development

8.1.3. Main Advantages / Disadvantages of Fuel Cell Buses

8.1.4. Fuel Cell Bus Schematics

8.1.5. Fuel Cell Bus Example Specifications

8.1.6. Other Zero / Low Emission Bus Options

8.1.7. Gaps in the Market: Prospect for fuel cell Buses

8.1.8. Battery Electric Buses: Rival or Complementary?

8.1.9. Can BEV and FCEV Coexist?

8.1.10. Infrastructure Cost BEV vs FCEV Bus Depot

8.1.11. Example Analysis: Foothill Transit, California, Line 486

8.1.12. Example Analysis: Foothill Transit

8.1.13. Delivering the Required Duty Milage

8.1.14. Californian Transit Agencies Milage Distribution

8.1.15. BEV vs FCEV Running Costs and Efficiency

8.1.16. Zero Emission Bus Range Per Day

8.1.17. Zero Emission Bus Range Per Day

8.1.18. Route Length Suitability for BEV Buses

8.1.19. Will Battery Improvements make Fuel Cell Buses Obsolete?

8.1.20. Loop Energy Inc

8.1.21. Comparison Hydrogen Fuel Cost vs Diesel Cost

8.2. FC Buses: Regional Performance, Costs, and Players

8.2.1. FCEB Bus Deployment Worldwide

8.2.2. Chinese Fuel Cell Bus OEM Market Share 2023

8.2.3. Chinese Fuel Cell Bus Examples

8.2.4. NEV Bus Sales - BEB, PHEB and FCEBs

8.2.5. Electric Bus OEMs and Market Shares in China

8.2.6. China Fuel Cell Installed Capacity 2024

8.2.7. CEMT - Edelman Hydrogen Energy Equipment

8.2.8. Beijing SinoHytec

8.2.9. Sinosynergy

8.2.10. Shanghai Hydrogen Propulsion Technology

8.2.11. REFIRE - Shanghai Reshaping Energy Technology

8.2.12. REFIRE - Shanghai Reshaping Energy Technology

8.2.13. Other Chinese Fuel Cell System Manufacturers

8.2.14. United Fuel Cell System R&D (Beijing) Co.

8.2.15. Toyota SORA Fuel Cell Bus

8.2.16. Structure of Toyota fuel cell bus

8.2.17. Japan - Fuel Cell Targets

8.2.18. Hyundai ELEC CITY Fuel Cell Bus

8.2.19. Iveco Fuel Cell Buses (Hyundai fuel cells)

8.2.20. South Korea - FCEB Targets

8.2.21. US Fuel Cell Buses: Active Fuel Cell Bus Project

8.2.22. US Fuel Cell Buses: Fuel Cell Bus Projects in Planning

8.2.23. US Fuel Cell Buses: Fuel cell Bus Projects Completed

8.2.24. Transitioning the US Fleet to Zero Emission Buses

8.2.25. The Cost of US Bus Fleet Transition to Zero Emission

8.2.26. US Fuel Cell Buses: Price 2010-2025

8.2.27. US Buses: Capex Cost 2015-2023 by Drivetrain

8.2.28. US Bus Costs By Powertrain: 2023-2025

8.2.29. NREL Fuel Cell Bus Evaluations 2023

8.2.30. NREL Fuel Cell Bus Evaluations 2023

8.2.31. Fuel Cell Bus Long-Term Stack Performance Data

8.2.32. NREL: Fuel Cell vs CNG Buses

8.2.33. New Flyer Xcelsior CHARGE H2

8.2.34. ElDorado National AXESS Fuel Cell Bus

8.2.35. ElDorado National AXESS Schematic

8.2.36. Van Hool

8.2.37. US School Buses

8.2.38. US eBus Purchase Subsidies

8.2.39. US Fuel Cell Bus and Hydrogen Station Grants 2024

8.2.40. European Fuel Cell Bus Deployment

8.2.41. EU JIVE 2 Targets

8.2.42. European Union - Fuel Cell Bus Market

8.2.43. Bus Registrations, FCEB, BEB, PHEV in Europe, 2013-2023

8.2.44. European Clean Bus Deployment Initiative

8.2.45. Cancelling Orders for Hydrogen Buses

8.2.46. Solaris Urbino 12 Hydrogen Bus

8.2.47. Solaris Alternative Drive Sales and Strategy

8.2.48. Solaris - Record Order for Ballard Fuel Cells

8.2.49. CaetanoBus H2.City Gold

8.2.50. Toyota Motor Europe

8.2.51. 1000km Hydrogen Coaches

8.2.52. SAFRA Businova Hydrogen

8.2.53. Wrightbus StreetDeck Hydroliner

8.2.54. Van Hool EU Orders

8.2.55. ADL Enviro400 FCEV

8.2.56. FCEB H2 Consumption Benchmarking

9. FORECAST SUMMARY

9.1. Introduction

9.1.1. Forecast Assumptions

9.2. Forecast Summary: Passenger Cars

9.2.1. Explaining the Change in FCEV Car Forecasts from the Previous Version

9.2.2. Forecast Assumptions

9.2.3. Fuel Cell Car Forecasts

9.2.4. FCEV Car Sales Forecast by Region 2021-2045 (Units)

9.2.5. FCEV Car Fuel Cell Demand Forecast by Region 2021-2045 (GW)

9.2.6. FCEV Car Battery Demand Forecast by Region 2021-2045 (MWh)

9.2.7. FCEV Car Market Value Forecast by Region 2021-2045 (US$)

9.3. Forecast Summary: Light Commercial Vehicles

9.3.1. Forecast Assumptions

9.3.2. FCEV LCV Sales Forecast by Region 2023-2045 (Units)

9.3.3. FCEV LCV Fuel Cell Demand Forecast by Region 2023-2045 (GW)

9.3.4. FCEV LCV Market Value Forecast by Region 2023-2045 (US$)

9.3.5. FCEV LCV Battery Demand Forecast by Region 2023-2045 (MWh)

9.4. Forecast Summary: Trucks

9.4.1. Forecast Assumptions

9.4.2. FCEV and Total MDT Sales Forecast 2020-2045 (Units)

9.4.3. FCEV MDT Sales Forecast by Region 2020-2045 (Units)

9.4.4. Medium Duty FC Truck Fuel Cell Demand

9.4.5. FCEV MDT Battery Demand Forecast by Region 2020-2045 (GWh)

9.4.6. FCEV MDT Market Value Forecast by Region 2020-2045 (US$)

9.4.7. FCEV and Total HDT Sales Forecast 2020-2045 (Units)

9.4.8. FCEV HDT Sales Forecast by Region 2020-2045 (Units)

9.4.9. FCEV HDT Fuel Cell Demand Forecast by Region 2020-2045 (GW)

9.4.10. FCEV HDT Battery Demand Forecast by Region 2020-2045 (GWh)

9.4.11. FCEV HDT Market Value Forecast by Region 2020-2045 (US$)

9.5. Forecast Summary: Buses

9.5.1. Forecast Assumptions

9.5.2. FCEV Bus Sales Forecast by Region 2020-2045 (Units)

9.5.3. FCEV Bus Fuel Cell Demand Forecast by Region 2020-2045 (MW)

9.5.4. FCEV Bus Battery Demand Forecast by Region 2024-2045 (MWh)

9.5.5. FCEV Bus Market Value by Region 2024-2045 (US$)

9.6. Forecast Summary: Total On-road FC Vehicles

9.6.1. FCEV Sales Forecast by Region 2023-2045 (Units)

9.6.2. FCEV Fuel Cell Demand Forecast by Region 2023-2045 (GW)

9.6.3. FCEV Battery Demand Forecast by Region 2024-2045 (GWh)

9.6.4. FCEV Market Value Forecast by Region 2020-2045 (US$)

9.6.5. FCEV Sales Forecast by Vehicle Type 2023-2045

9.6.6. FCEV vs BEV Market Share in 2045

9.6.7. FCEV Fuel Cell Demand Forecast by Vehicle Type 2023-2045 (GW)

9.6.8. FCEV Battery Demand Forecast by Vehicle Type 2024-2045 (GWh)

9.6.9. FCEV Market Value Forecast by Vehicle Type 2023-2045 (US$)

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(自動車)の最新刊レポート

IDTechEx社の自動車 - Vehicles分野での最新刊レポート

本レポートと同じKEY WORD()の最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

|