世界各国のリアルタイムなデータ・インテリジェンスで皆様をお手伝い

Chemical Recycling and Dissolution of Plastics 2024-2034: Technologies, Players, Markets, Forecastsプラスチックのケミカルリサイクルと溶解 2024-2034:技術、プレーヤー、市場、予測 このレポートでは、IDTechExが独自の市場予測、業界分析、および熱分解、解重合、ガス化、溶解プロセスに関する重要な技術評価を提供しています。 主な掲載内容(目次より抜粋) ... もっと見る

※ 調査会社の事情により、予告なしに価格が変更になる場合がございます。

Summary

このレポートでは、IDTechExが独自の市場予測、業界分析、および熱分解、解重合、ガス化、溶解プロセスに関する重要な技術評価を提供しています。

主な掲載内容(目次より抜粋)

Report Summary

Creating a circular economy is an essential sustainability target for stakeholders across the plastic value chain. With notable market drivers, including increasing regulatory pressures, IDTechEx is witnessing a surge in market activity that will impact the global landscape over the next decade and beyond. Conventional mechanical recycling methods will continue to be necessary but given the inferior physical properties of the products, this downcycling can only go so far; this is where chemical recycling and dissolution enter the picture.

In this leading report, IDTechEx provides independent market forecasts, industry analysis and critical technical assessment on pyrolysis, depolymerization, gasification, and dissolution processes both in use today and being proposed for the near future to enable a circular economy.

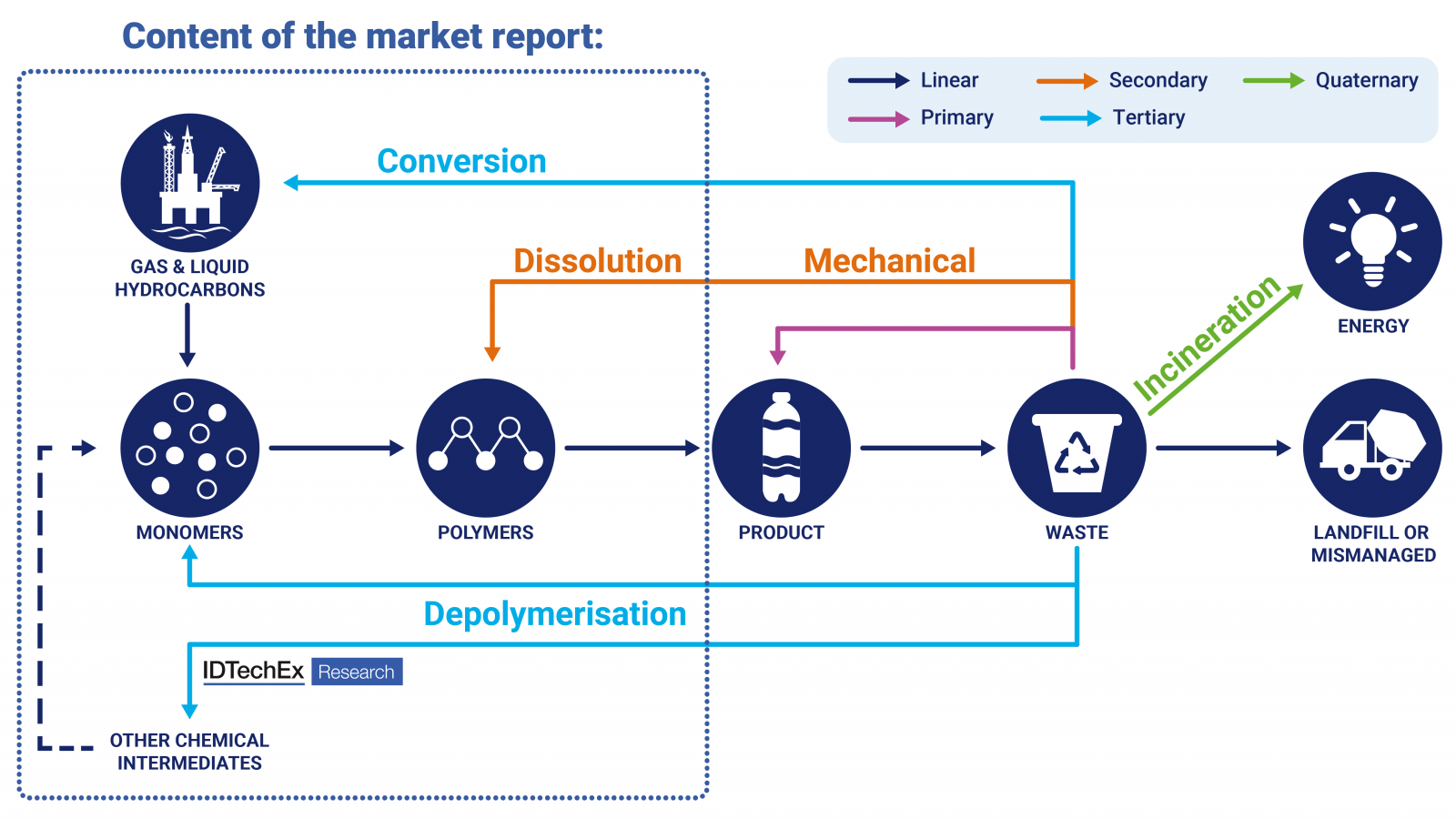

The existing ISO definition defines chemical recycling as follows: feedstock (=chemical) recycling: recycling of plastic waste: conversion to monomer or production of new raw materials by changing the chemical structure of plastic waste through cracking, gasification, or depolymerization, excluding energy recovery and incineration.

Headlines on investments, planned expansions, and real-world product launches are all accelerating in their frequency and scale. The largest petrochemical companies, consumer goods companies, and other key stakeholders in the value chain are responding with both internal developments and external engagements; early-stage technology companies are announcing funding, strategic partnerships, joint development agreements, and offtake agreements from critical players in the supply chain.

However, chemical recycling is not without its critics. Many question both the environmental credentials and economic viability of these processes. Companies generally position their solution as a silver bullet, but the reality is more complex; there are benefits and limitations to every approach but that does not mean each cannot be a piece in the overall puzzle. There are also many examples of failures that should provide a suitable warning.

Chemical recycling of plastic waste

This is the area with the most attention right now. These tertiary processes break the polymer down either into constituent monomers or into raw materials further upstream in the plastics supply chain.

Depolymerization is one of the key emerging processes. This takes a relatively homogeneous feedstock and breaks the material down into its constituent monomers via thermal, chemical, or biological processes. Not all polymers are well suited to this with PET and PS being the most prominent but PU, PC, PLA, PMMA, PA, and more all have industrial activity.

Pyrolysis and gasification can convert mixed plastic waste into pyrolysis oil and syngas, respectively, via a thermochemical process. The main difference between the two is the oxygen present. The products could re-enter the polymer supply chain and create a circular economy or not be recycled and used directly for energy or converted into fuel. Pyrolysis is the most notable here with many chemical companies pursuing this and incorporating a mass balance methodology to account for sustainability. There are several technical limitations and specific considerations both upstream (sorting etc) and downstream (cracking etc) but these are beginning to be overcome. Like pyrolysis, gasification is not a new process; in fact, it has regularly been utilized for removing municipal solid waste (MSW) from landfill and converting it to energy. Gasification can be seen as the "backstop" when all other approaches are exhausted.

The chemical recycling market is on the cusp of significant growth. This unbiased market report provides a complete overview of the technology providers as well as a comprehensive list of the current plants and future projects. There is significant momentum, and the maturity will benefit the whole industry; more announcements will arrive but equally not all of those planned will ever be realized.

Overall, IDTechEx forecasts that pyrolysis and depolymerization plants will use over 17 million tonnes/year of plastic waste by 2034. This is a significant number but will require a major investment and continuous engagement from stakeholders across the value chain. Chemical recycling has a role to play in closing the loop, but it is just one small solution to a greater global challenge.

IDTechEx details recent increases in global chemical recycling capacity, with both pyrolysis and depolymerization plant capacities seeing increases of over 60% since early 2021.

Chemical recycling also has its notable critics. They point out the flaws in the claimed environmental benefits, such as the assumptions behind life cycle assessments including the comparison that waste would have otherwise been incinerated, and question the economic viability. The economics are challenging and not only influenced by the company's process but also the associated infrastructure, policy, and macroeconomic trends. The "green premium" for the products is a key factor; the further prices can be decoupled from that of oil, the greater the long-term success of these projects. This report aims to provide a balanced view of both those endorsing and criticizing the technology.

Unsurprisingly, the majority of the engagement is for FMCG packaging, but it is not limited to this sector with various textiles, automotive parts, electronic equipment, and other significant use cases.

There also remains a large amount of technology innovation, including microwave and enzymatic processes for depolymerization, hydrothermal approaches as a competition to pyrolysis, new polymer developments, and more. These developments are all detailed and appraised throughout the report.

Secondary recycling via dissolution

Secondary recycling involves recovering and re-using the plastic without breaking the chemical bonds. Mechanical routes are very well known but not always suitable and downcycle the product. An emerging space is selectively dissolving the polymer and subsequently precipitating this to produce the pure polymer; ideally, this is a low-energy process, and the recycled polymer retains properties closer to that of the virgin material.

As with chemical recycling, there are many challenges as clearly demonstrated by failed projects. However, numerous players are climbing the technology and manufacturing readiness levels and progressing to notable plants. There is key proprietary know-how in both the solvent and process conditions which must be specifically tailored. There is also a range of waste polymers being pursued with PS, PP, and PET being the more prominent. This report provides an in-depth analysis of the technology, players, plants, economic viability, environmental impact, and market outlook.

IDTechEx has a longstanding history of providing an independent technical and market assessment of sustainable plastics. This market report includes:

Table of Contents

|

|