世界各国のリアルタイムなデータ・インテリジェンスで皆様をお手伝い

Quantum Computing Market 2024-2044: Technology, Trends, Players, Forecasts量子コンピューティング市場2024-2044:技術、動向、プレイヤー、予測 この調査レポートでは、企業へのインタビューや複数のカンファレンスへの出席を含む広範な一次調査および二次調査をもとに、競合する量子コンピューティング技術(超伝導、シリコンスピン、フォトニック、トラ... もっと見る

※ 調査会社の事情により、予告なしに価格が変更になる場合がございます。

Summary

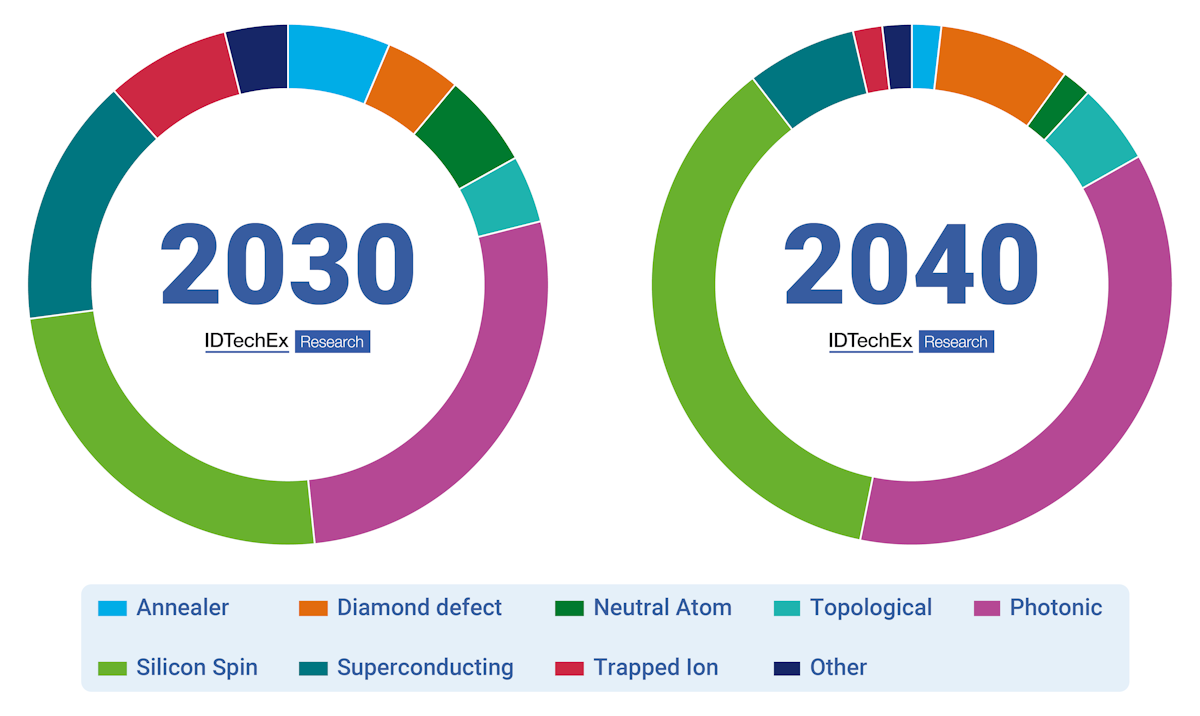

この調査レポートでは、企業へのインタビューや複数のカンファレンスへの出席を含む広範な一次調査および二次調査をもとに、競合する量子コンピューティング技術(超伝導、シリコンスピン、フォトニック、トラップドイオン、中性原子、トポロジカル、ダイヤモンド欠陥、アニーリング)について詳細に調査・分析しています。

主な掲載内容(目次より抜粋)

Report Summary

IDTechEx's report 'Quantum Computing 2024-2044' covers the hardware that promises a revolutionary approach to solving the world's unmet challenges. Quantum computing is pitched as enabling exponentially faster drug discovery, battery chemistry development, multi-variable logistics, vehicle autonomy, accurate asset pricing, and much more. Drawing on extensive primary and secondary research, including interviews with companies and attendance at multiple conferences, this report provides an in-depth evaluation of the competing quantum computing technologies: superconducting, silicon-spin, photonic, trapped-ion, neutral-atom, topological, diamond-defect and annealing.

These competing quantum computing technologies are compared by key benchmarks including qubit number, coherence time and fidelity. The scalability of whole computer systems is appraised - incorporating hardware needs for qubits initialisation, manipulation, and readout. This results in a twenty-year market forecast covering 2024-2044. The total addressable market for quantum computer use is converted to hardware sales over time, accounting for advancing capabilities and the cloud access business model. The entire hardware market is forecast to grow to US$800m by 2034. This growth will be driven by early adopters in pharmaceutical, chemical, aerospace, and finance institutions, leading to increased installation of quantum computers into colocation data centres and private networks alike. Revenue and volume forecasts are split into eight forecast lines for each methodology covered. Historic data on the number of quantum computer start-ups utilizing each methodology, and the qubit milestones achieved, are also included.

.png)

Key questions answered in this report include:

A logical era for Quantum Computers ahead

In the last decade, the number of companies actively developing quantum computer hardware has quadrupled. Between 2022 and 2024 multiple funding rounds surpassing US$100 million have been closed, and the transition from lab-based toys to commercial product has begun. Competition is building not only between different companies but between quantum computing technologies. The focus today has intensified on the need for logical, or error-corrected qubits. The challenge ahead is to scale up hardware and increase qubit number, while reducing errors as well as infrastructure demand - no mean feat.

.png)

Whilst all systems depend on the use of qubits - the quantum equivalent to classical bits - the architectures available to create them vary substantially. Many are now familiar with IBM and their superconducting qubits - housed inside large cryostats and cooled to temperatures colder than deep space. Indeed, in 2023 superconducting quantum computers broke the 1000 qubit milestone - with smaller systems made accessible via the cloud for companies to trial out their problems. However, many agree that the highest value problems - such as drug discovery - need many more qubits, perhaps millions more. As such, alternatives to the superconducting design, many proposing more inherent scalability, have received investment. There are now more than eight technology approaches meaningfully competing to reach the million-qubit milestone.

With so many competing quantum computing technologies across a fragmented landscape, determining which approaches are likely to dominate is essential in identifying opportunities within this exciting industry. IDTechEx uses an in-house framework for quantum commercial readiness level to measure how quantum computer hardware is progressing in comparison with its classical predecessor. Furthermore, as the initial hype around quantum computing begins to cool investors will increasingly demand demonstration of practical benefits, such as quantum supremacy for commercially relevant algorithms. As such, hardware developers need to show not only the quality and quantity of qubits but the entire initialization, manipulation, and readout systems. Improving manufacturing scalability and reducing cooling requirements are also important, which will create opportunities for methodology agnostic providers of infrastructure such as speciality materials and cooling systems. By evaluating both the sector and competing quantum computing technologies, this report provides insight into the opportunities provided by this potentially transformative technology.

Key aspects

This report provides the following information:

Market Forecasts & Analysis:

Table of Contents

|