世界各国のリアルタイムなデータ・インテリジェンスで皆様をお手伝い

定置用エネルギー貯蔵用電池 2023-2033年Batteries for Stationary Energy Storage 2023-2033 定置用エネルギー貯蔵のためのバッテリー需要は、世界的に電力網に追加される再生可能エネルギー資源の増加に伴い、拡大すると考えられています。また、再生可能エネルギー発電とエネルギー貯蔵に関する目標達... もっと見る

日本語のページは自動翻訳を利用し作成しています。

サマリー

定置用エネルギー貯蔵のためのバッテリー需要は、世界的に電力網に追加される再生可能エネルギー資源の増加に伴い、拡大すると考えられています。また、再生可能エネルギー発電とエネルギー貯蔵に関する目標達成を求める政府や州からの圧力も、配備の推進力となるでしょう。また、規制環境の進化と改善により、エネルギーおよびバッテリー貯蔵市場の繁栄が期待されます。

IDTechExは、2033年までに世界の定置用蓄電池の累積容量が2TWhを超えると予測しています。これにより、2023年から2033年にかけて、定置型蓄電池の年間導入量はCAGR30%で成長すると予想されます。

.png)

本レポートでは、きめ細かい市場予測、キープレイヤー分析、技術動向とアプリケーション、収益源を生み出すドライバーとビジネスモデル、上位設置国の地域分析などを掲載しています。

定置用蓄電池の技術動向

過去10年間で、リチウムイオン電池は定置型エネルギー貯蔵技術としてますます重要性を増しています。現在では、世界の電気化学エネルギー貯蔵設備の90%以上を占めています。リチウムイオン電池の採用の主な理由は、性能の向上とコストの削減が急速に進んだことです。

LFPとNMCが最も普及していますが、グリッドスケールの電池はLFPにシフトすると予想されます。その理由としては、コストが低いこと、安全性が高いこと、NMCに比べてLFPの方がサイクル寿命が長いことなどが挙げられます。家庭用電池のサプライヤーは、電池の化学的性質に左右されにくく、電池の寿命は電池本来の性質や化学的性質よりも、消費者の使用行動によって決まるからです。とはいえ、LFPとNMCは今後も家庭用市場で支配的な2つの化学物質として君臨し続けるだろう。

その他の分析・考察としては、最新の家庭用蓄電池市場の動向、市場規模(米ドル)、主要企業の収益データなどを、主要企業へのインタビューから得た新たな一次情報によって補完しています。1社目は、中国で太陽光・住宅・低速車両用電池の開発・販売を行うBSLバッテリーです。2社目はE3/DC社で、ドイツに拠点を置き、住宅市場向けの電池システムを開発・販売しており、Vehicle-to-X(V2X)市場への進出を計画しています。E3/DC社では、バッテリービジネスのディレクターとして、家庭用市場の動向についてお話を伺いました。

グリッドスケールの市場は、電力網における再生可能エネルギーの容量の増加に対応するため、より長時間の蓄電に傾いている。リチウムイオンは将来的に長時間の蓄電には向かないかもしれませんが、RFBは10時間以上の蓄電が可能で、エネルギー会社が将来的に長時間のグリッドスケール蓄電を導入するための別の手段となります。しかし、この市場はまだ初期段階にあり、グリッドスケールの実証プロジェクトが立ち上がり始めています。例えば、住友電工は2022年に日本で世界最大級のバナジウムRFBを稼動させました。

アプリケーション、ビジネスモデル、収益源

今後10年間、世界の電池エネルギー貯蔵システム(BESS)設置台数のうち、GWh単位で見ると、メーター前(FTM)設置台数の方がメーター後(BTM)設置台数よりも大きな割合を占めると予想されています。

これらの電池は、さまざまな公益サービスや補助サービスを提供することができ、送電系統運用者(TSO)に適切な国家エネルギー安全保障と供給を提供するために必要な手段を提供することができます。さらに、レベニュースタッキングなどの手段により、大型電池システムが所有者に収益をもたらす手段も明らかになってきている。ビジネスモデルの成熟が進めば、BESSの収益性に対する投資家の信頼が高まり、将来のプロジェクトコストの削減と設置台数の増加が促進されるでしょう。

電池はBTM市場において、主に顧客側に価値を提供します。ドイツのような地域ではFiTスキームが段階的に廃止されるため、消費者は価格裁定を利用し、グリッド価格が最も高いピーク需要時に電池を使用することになります。

本レポートでは、あらゆる市場セクターにおいて蓄電池が活躍できる様々な電力市場について、収益創出メカニズムとともに、図解と解説を交えて総合的に解説しています。

市場の推進要因:再生可能エネルギーの導入、蓄電池の目標値、規制

エネルギー貯蔵システム(ESS)の導入は、再生可能エネルギーの普及と統合をより高いレベルで実現するために必要です。また、世界的なBESSの導入数を加速させるためには、エネルギーとバッテリーストレージの目標値と明確な政策的枠組みが必要です。

米国のいくつかの州は、エネルギー貯蔵と再生可能エネルギーの義務付けを行っています。より多くの州が新しい蓄電池目標を発表し、古い目標を拡大している(ニューヨークなど)ため、この傾向は続くと予想され、米国のBESS成長の重要な推進力となるであろう。

オーストラリアの州レベルの再生可能エネルギー目標と蓄電インセンティブは、過去と未来の高いBESS設置率の主要な原動力となっています。

しかし、政府レベルの再生可能エネルギーやストレージの目標は、ビクトリア・エネルギー政策センター(VEPC)が推進してきたものの、現在のところ存在しません。明らかに、オーストラリアでは州レベルの圧力が政策面で強まっている。

地域は、BESS設置のための規制障壁をより意識するようになっている。例えば、英国では蓄電池の導入オークションで50MWの上限が撤廃されたため、今後数年間でより大規模なシステムが導入されることになります。また、現在インドの2003年電気事業法では、蓄電は独立した資産として定義されていません。このため、これらの資産に課税する際に規制上のハードルがあり、投資家の信頼を低下させ、インドのBESSの成長を阻む大きな障壁となっています。

包括的な分析および市場予測

本レポートでは、FTMおよびBTM BESSの年間導入量(MWh、GWh、TWh導入量)について、10年間の詳細な市場予測を提供しています。

最も活発な7カ国では、住宅用/C&I用/グリッドスケール用、またはFTM/BTM用の年間導入量MWhを2023年から2033年にかけて予測しています。米国と中国は、2033年にこれらの地域の累積BESS容量の59%を占め、総導入量では互いに拮抗することになる。

地域別分析セクションでは、地域の規制動向、政府や州レベルの発表、再生可能発電やエネルギー、バッテリーストレージの目標、主要プレイヤーの活動、主要プロジェクトの設置、将来のプロジェクトパイプラインに関する詳細な議論と分析が含まれています。

将来の定置型蓄電池導入のためのこれらの推進要因と動向は、文書化され、精査され、議論されています。

主な内容

本レポートでは、以下の情報を提供しています。

技術動向:

バリューチェーン分析:

市場予測および地域分析:

目次

Summary

この調査レポートでは、FTMおよびBTM BESSの年間導入量(MWh、GWh、TWh導入量)について、2023-2033年の10年間の詳細な市場予測を提供しています。

主な掲載内容(目次より抜粋)

企業プロフィール

Report Summary

Battery demand for stationary energy storage is set to grow in line with an increasing number of renewable energy resources being added to electricity grids globally. Deployments will also be driven by pressure from governments and states to reach targets pertaining to renewable energy generation and energy storage. An evolving and improving regulatory landscape will also allow energy and battery storage markets to flourish.

IDTechEx predicts that by 2033, global cumulative stationary battery storage capacity is set to exceed 2 TWh. This will see annual stationary storage deployments grow at a CAGR of 30% from 2023-2033.

(1).png)

Lithium-ion Battery Demand (GWh, left) and (% split by market segment, right). Source IDTechEx

This report includes granular market forecasts, key player analysis, technology trends and applications, drivers and business models giving rise to revenue streams, and regional analysis for the top installing countries.

Technology trends for stationary battery storage

Over the past decade, Li-ion batteries have become an increasingly important stationary energy storage technology. They now account for >90% of global installations of electrochemical energy storage. The main driver for their adoption has been the fast improvement in their performance and reduction in their cost.

LFP and NMC chemistries are the most popular in storage applications, though a shift towards LFP for grid-scale batteries is expected. Reasons for this include lower costs, better safety properties, and higher cycle life of LFP versus NMC. Residential battery suppliers are far more agnostic to battery chemistry choice, as these batteries' lifetimes are dictated more by consumer use behaviour than their intrinsic properties and chemistry. Regardless, LFP and NMC will continue to reign as the two dominant chemistries in the residential market.

Other analyses/discussions include the latest residential storage market trends, market size (US$), key players with revenues data, etc. supplemented by new primary information from key company interviews. The first company interviewed is BSL Battery, who operate in China, develop and sell batteries into the solar/residential and low speed vehicle markets. The second company interviewed is E3/DC GmbH, that operate in Germany, develop and sell battery systems to the residential market, and are planning to expand into the Vehicle-to-X (V2X) market. The E3/DC interviewee was a Director for their Battery Business and provided key insights into residential market trends.

The grid-scale market is leaning towards longer duration of battery storage, to accommodate growing volumes of renewable energy capacity on electricity grids. Li-ion may not be well suited to long-duration storage in future, whereas RFBs can store >10 hours of energy, presenting another means for energy companies to install longer-duration grid-scale storage in future. However, this market is still in its early stages, with grid-scale proof-of-concept projects starting to emerge. For instance, in 2022, Sumitomo Electric brought one of the world's largest vanadium RFBs online in Japan.

Applications, business models and revenue streams

Annual front-of-the-meter (FTM) installations will take a larger share of global annual Battery Energy Storage System (BESS) installations, by GWh, than behind-the-meter (BTM) installations in the next decade.

These batteries can provide a range of utility and ancillary services, giving Transmission System Operators (TSOs) the tools necessary to provide adequate national energy security and supply. Moreover, the means for large battery systems to produce revenues for their owners are becoming more apparent, through means such as revenue stacking. As business models continue to mature, investor confidence in BESS profitability will grow, thus facilitating reduced future project costs and increased installation volumes.

Batteries provide value in the BTM market primarily for the customer side. With regions such as Germany phasing out FiT schemes, consumers will take advantage of price arbitrage; using their batteries when grid prices are most expensive at times of peak demand.

This report provides a holistic view, with depictions and explanations, of the various electricity markets that battery storage assets can operate in across all market sectors, in tandem with revenue generation mechanisms.

Market drivers: renewable energy deployment, battery storage targets, regulation

The adoption of energy storage systems (ESS) is necessary for higher levels of renewable energy penetration and integration. As well as this, energy and battery storage targets and clear policy frameworks are necessary if the number of global BESS deployments is to be expedited.

Several US States have energy storage and renewables mandates. With more states announcing new battery storage targets, and expanding older targets (such as New York), this trend is expected to continue and will be a key driver for US BESS growth.

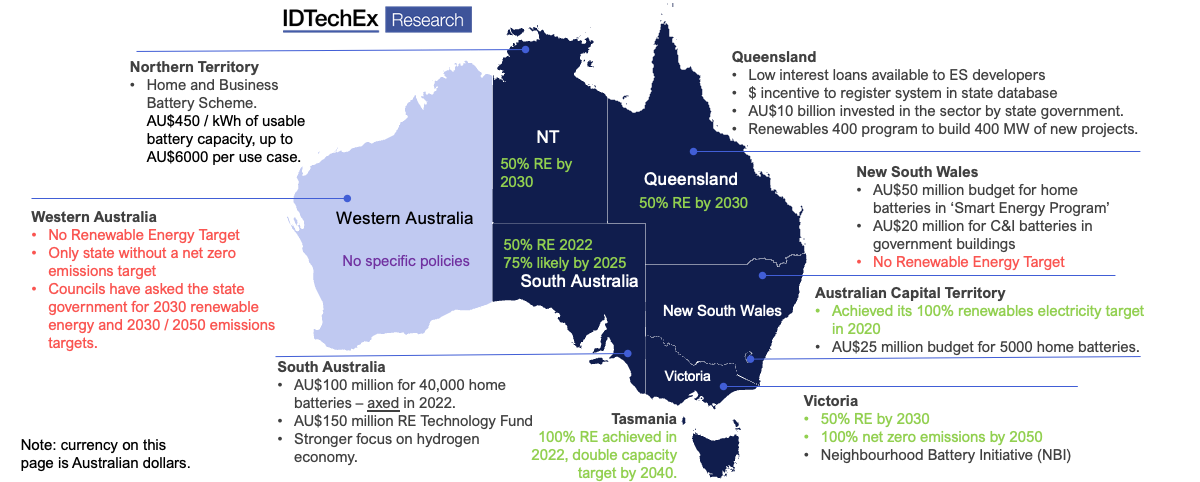

The state-level Australian renewable energy targets and storage incentives are key drivers for their high historical and forecasted BESS installation rates.

.png)

Australian storage policy, funding & renewables targets. Source IDTechEx

However, any government-level renewable energy or storage targets are currently absent, while the Victoria Energy Policy Centre (VEPC) has pushed for this. Clearly, state-level pressure is mounting on the policy front in Australia.

Regions are becoming more aware of regulatory barriers for the installation of BESS. For example, the removal of the 50 MW cap for storage deployment auctions in the UK will see larger systems installed in the coming years. Also, currently under India's Electricity Act 2003, storage is not defined as a standalone asset. This has led to regulatory hurdles when taxing these assets, reducing investor confidence, and acting as a major barrier preventing Indian BESS growth.

Comprehensive analysis and market forecasts

This report offers granular 10-year market forecasts, for the annual installations of FTM & BTM BESS (in MWh, GWh, TWh installed).

The seven most active countries have 2023-2033 forecasts with annual MWh installed for residential / C&I / grid-scale splits, or FTM / BTM splits otherwise. The US and China will be responsible for ~59% of these regions' cumulative BESS capacity in 2033, while rivalling each other for total deployments.

The regional analysis section includes detailed discussion and in-depth analysis on regional regulation developments, government and state-level announcements, renewable generation and energy and battery storage targets, key player activity, major project installations, and future project pipelines.

These drivers and developments for future stationary storage deployments are documented, scrutinised, and discussed.

Key aspects

This report provides the following information

Technology trends:

Value chain analysis:

Market Forecasts & Regional Analysis:

Table of Contents

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(太陽光)の最新刊レポートIDTechEx 社の最新刊レポート本レポートと同じKEY WORD()の最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

詳細検索

2024/07/01 10:26 162.23 円 174.76 円 207.97 円 |