世界各国のリアルタイムなデータ・インテリジェンスで皆様をお手伝い

グリーン水素の製造:電解槽市場 2023-2033年Green Hydrogen Production: Electrolyzer Markets 2023-2033 IDTechExは、水電解装置市場が2033年までに1,200億米ドル超に成長すると予測しています。グリーン水素や水素経済に対する以前の誇大宣伝が衰退する一方で、現在では官民を問わず、グリーン水素の製造のための... もっと見る

日本語のページは自動翻訳を利用し作成しています。

サマリー

IDTechExは、水電解装置市場が2033年までに1,200億米ドル超に成長すると予測しています。グリーン水素や水素経済に対する以前の誇大宣伝が衰退する一方で、現在では官民を問わず、グリーン水素の製造のための水電解システムの開発に多額の資本が投入されています。水素の需要は、精製やアンモニア生産などの既存市場だけでなく、メタノール、グリーン・スチール、輸送用途などの新市場からも世界的に増加すると予想されています。このような水素の生産と使用の増加は、エネルギー安全保障の向上と脱炭素化への取り組みによって促進されています。しかし、脱炭素社会の実現に貢献するためには、製造される水素そのものが低炭素である必要があります。

グリーン水素とは?

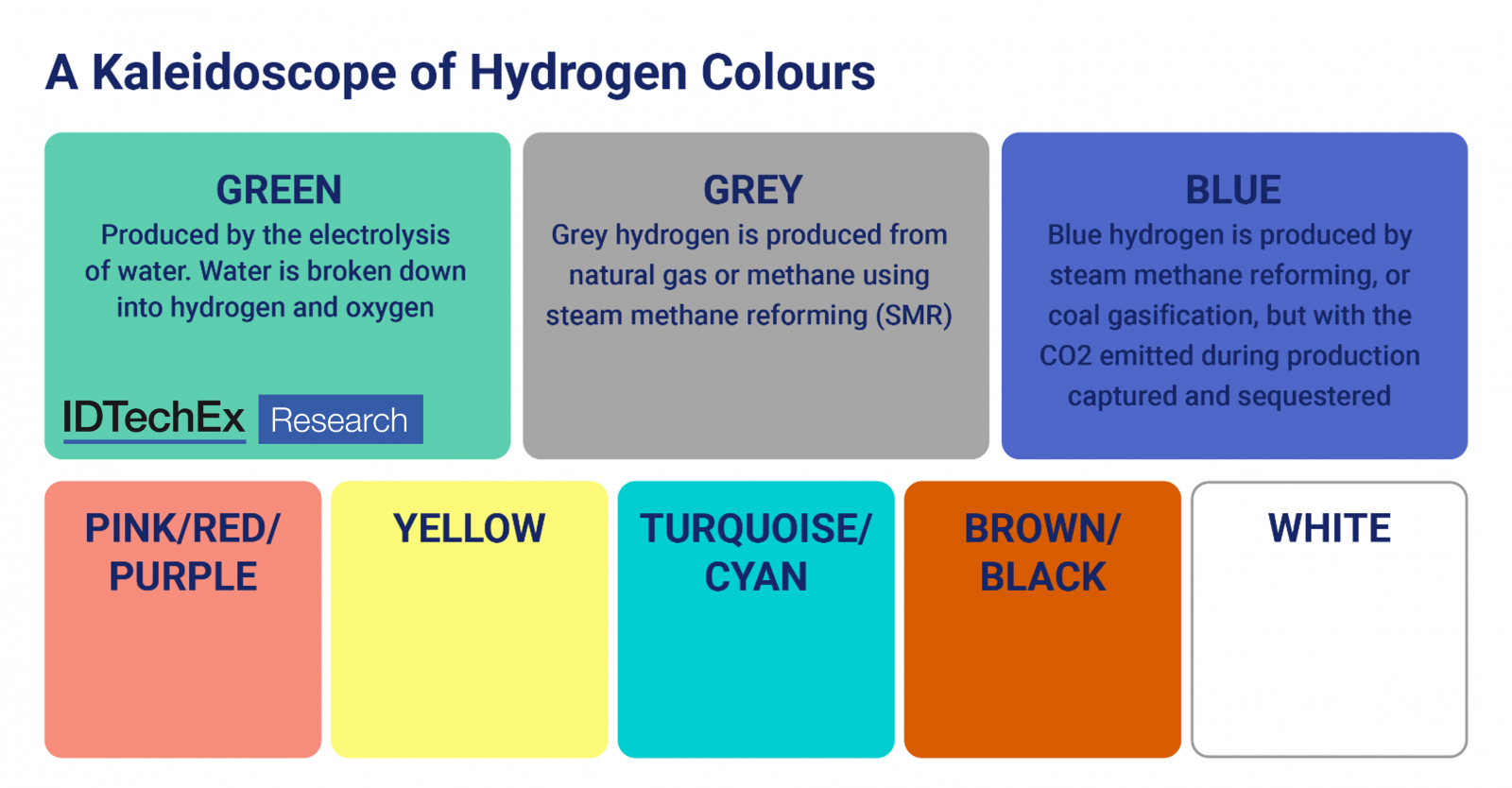

グリーン水素とは、電解槽で水を電気分解し、水素と酸素に分解することである。電解槽の電力に再生可能な電力を使用すれば、製造される水素は「グリーン水素」と呼ばれます。太陽光発電や洋上風力発電などの再生可能エネルギーを動力源とするグリーン水素は、現在生産されている水素(そのほとんどがメタンの水蒸気改質または石炭ガス化から得られる)よりも炭素排出量が少なくなります。現在、水素製造のさまざまなサブルートを表現するために、多くの色が存在します。例えば、ピンクや紫の水素は、原子力発電による電解水素を表し、黄色の水素は、太陽光発電による水の電解水素を表します。グレーと黒の水素は、メタンの改質や石炭ガス化によって製造された水素を表し、青の水素は、その結果排出されるCO2を回収した場合の水素を表しています。

.png)

グリーン水素市場

グリーン水素は、水素製造の脱炭素化につながるものであり、脱炭素化が困難なさまざまな分野の脱炭素化に貢献する。現在、水素の主な最終用途は精製とアンモニア製造である。中期的には、これらの用途が水素の主要な用途であることに変わりはないと予想される。さらに、鉄鋼、メタノール製造、大型車、船舶、航空など、脱炭素化が困難なセクターにおいても、水素は重要な役割を果たすと考えられます。また、水素は、鉄鋼、メタノール、建設、化学などの産業において、天然ガスや石炭の使用を減らし、水素の地産地消を可能にすることで、より高いエネルギー安全保障を実現する道筋を示すものでもある。2022年のロシアのウクライナ侵攻に伴う天然ガス価格と供給の不確実性と不安定性、そして需要の高まりと世界経済の脱炭素化に対する圧力を考えると、これは特に重要な課題であると言えます。しかし、IDTechExは、グリーン水素が2022年の世界全体の水素生産量の1%未満を占めると推定しており、電解槽とグリーン水素市場で必要とされるレベルを強調しています。

.png)

電解槽技術

グリーン水素の製造に使用される電解槽技術には、アルカリ性(AELまたはAWE)、プロトン交換膜または高分子電解質膜(PEM)、固体酸化物電解質(SOEL)の3種類があります。それぞれの技術には、長所と短所がある。アルカリ性電解槽は、古くから商業的に利用されており、産業用途に使用されています。アルカリ電解槽は資本コストが低く、寿命が長いことが特徴です。電解槽は商業化の初期段階にあるが、今後数年で市場シェアを拡大する予定である。電解槽は、アルカリ性電解槽に比べて出力密度、水素圧、応答速度が速いことが特徴です。このため、一般的に再生可能エネルギーの利用に適している。SOELは最も歴史の浅い電解槽技術です。700℃以上の高温で作動するため、システム効率は高いが、高価であり、動的な運転に苦労し、システムの寿命の改善が必要となる可能性がある。しかし、その高い効率は、製造される水素の平準化コストを下げる役割を果たし、また、H2OとCO2の複合電解による合成ガスの製造にも期待されている。

.png)

電解槽システムの性能を評価するための主要な指標には、効率、資本コスト、応答時間とダイナミックレンジ、水素純度と圧力、寿命と設置面積などがあります。最終的に最も重要なパラメータの1つは、水素の平準化コストであろう。このレポートでは、さまざまな電解槽システムについて、作動メカニズム、使用材料、システム性能などを分析・比較している。また、電解槽技術の改善と革新とともに、将来の電解槽技術の採用についての展望と議論も提供しています。

電解槽市場

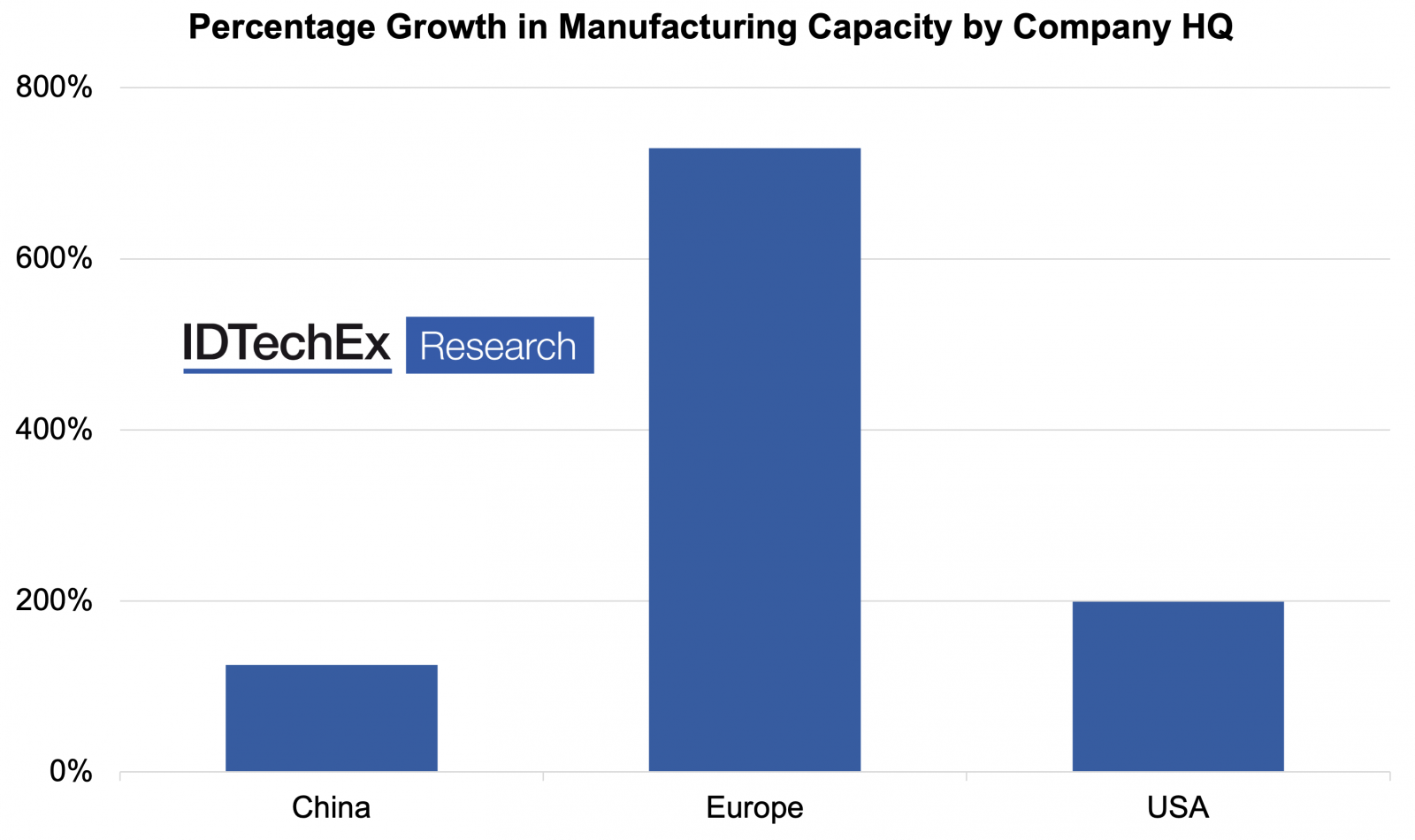

電解槽の製造能力は、この成長市場でのシェアを獲得するために、今後5年間で大幅に増加すると予想されます。IDTechExの分析によると、ヨーロッパ企業は電解槽の製造能力と能力を拡大し成長させる計画に特に積極的であるが、電解槽製造への多額の投資は中国と米国企業からも予想され、インドとオーストラリアの企業もこの市場への参入を検討している。電解槽市場は現在、アルカリ電解槽と電解質膜電解槽のメーカーが支配的で、固体酸化物電解槽を製造・商品化している企業は比較的少ない。しかし、固体酸化物型電解槽と固体酸化物型燃料電池は類似しているため、燃料電池メーカーがグリーン水素市場に参入するきっかけになる可能性があります。確かに、グリーンでクリーンな水素製造のための野心的な国や地域の目標を達成するためには、3種類の電解槽のいずれにおいても電解槽市場の成長が必要であろう。

.png)

本レポートでは、現在商業化・開発されている電解槽の技術や設計について分析・比較を行っています。さらに、主要な電解槽メーカーとプレーヤー、現在の製造能力、設置計画、地域のグリーン水素製造目標などを概説し、市場の概要を示しています。

本レポートでは、以下の情報を提供しています。

水素市場

電解槽技術分析

電解槽の市場分析

Summary

この調査レポートは、2023-2033年のグリーン水素の製造について詳細に調査・分析しています。

主な掲載内容(目次より抜粋)

Report Summary

IDTechEx forecasts the water electrolyzer market to grow to over US$120B by 2033. While previous periods of hype for green hydrogen and the hydrogen economy have waned, significant capital, both public and private, is now being spent on developing water electrolysis systems for the production of green hydrogen. Hydrogen demand is expected to grow globally from both incumbent markets, including refining and ammonia production, as well as from new markets such as in methanol, green steel, and transport applications. This increase in hydrogen production and use is being driven by a growing desire to improve energy security and by decarbonization efforts. However, to play a role in decarbonization, the hydrogen produced must itself be low carbon.

What is green hydrogen?

Green hydrogen refers to the splitting of water into hydrogen and oxygen via electrolysis in an electrolyzer. If renewable electricity is used to power the electrolyzer then the hydrogen produced can be referred to as green hydrogen. Powered by renewable energy sources such as solar PV or offshore wind power, this green hydrogen will have lower carbon emissions associated with it than the hydrogen being produced today, most of which comes from steam methane reformation or coal gasification. A plethora of colours now exist to describe the various sub-routes to hydrogen production. For example, pink/purple hydrogen is used to describe electrolytic hydrogen using nuclear power and yellow hydrogen describes electrolytic hydrogen utilising mixed power grid sources, though it has also been used to refer to solar PV powered water electrolysis. Grey and black hydrogen refer to hydrogen produced via methane reformation or coal gasification while blue hydrogen describes this hydrogen if the resulting CO2 emissions are captured.

Green hydrogen markets

Green hydrogen offers a route to decarbonising hydrogen production, in turn helping to decarbonise various hard-to-abate sectors. Currently, the primary end-uses for hydrogen are in refining activities and ammonia production. These are forecast to remain the key uses for hydrogen in the medium-term. Furthermore, hydrogen can also play a role in helping to decarbonise hard-to-abate sectors such as steel manufacturing, methanol production or certain modes of transport such as heavy-duty vehicles, shipping, or aviation. Beyond decarbonization, hydrogen also offers a route to greater energy security by allowing local production of hydrogen as well as a reduction in the use, via their replacement, of natural gas and coal for industries including steel, methanol, construction and chemicals production. This is particularly topical given the uncertainty and volatility in natural gas prices and supply following Russia's invasion of Ukraine in 2022 as well as growing demand and pressure to decarbonise the global economy. However, IDTechEx estimate that green hydrogen accounts for <1% of total hydrogen production globally in 2022, highlighting the level that is needed in the electrolyzer and green hydrogen market.

.png)

Electrolyzer technology

There are three main types of electrolyzer technology that can be used to produce green hydrogen: alkaline (AEL or AWE), proton-exchange-membrane or polymer-electrolyte-membrane (PEM), and solid-oxide electrolyzers (SOEL). Each technology comes with their own set of advantages and disadvantages. Alkaline electrolyzers have long been commercial and used for industrial applications. They are characterised by their low capital costs and long lifetimes. PEM electrolyzers are at an earlier stage of commercialization but are set to gain market share over the coming years. They are characterised by higher power densities, output hydrogen pressures and faster response times than alkaline systems. This generally makes them better suited to utilising renewable power. SOELs are the youngest electrolyzer technology. Operating at elevated temperatures above 700°C, they offer higher system efficiencies but are expensive, can struggle with dynamic operation, and improvements to system lifetime are likely to be necessary. Nevertheless, their higher efficiencies can play a role in decreasing the levelized cost of the hydrogen produced while they also hold promise for producing syngas through the combined electrolysis of H2O and CO2.

Key metrics for assessing the performance of an electrolyzer system include: efficiency, capital cost, response time and dynamic range, hydrogen purity and pressure, lifetime and footprint. Ultimately, one of the most important parameters is likely to be levelized cost of hydrogen. This report provides an analysis and comparison of the different electrolyzer systems available, covering working mechanisms, materials employed, and system performance, amongst other factors. An outlook and discussion on future electrolyzer technology adoption is also provided alongside improvements and innovations being made to electrolyzer technology.

Electrolyzer market

Manufacturing capacity is expected to increase significantly over the next 5 years as players looks to capture a share of this growing market. IDTechEx analysis shows that European companies are particularly active in their plans to expand and grow their electrolyzer manufacturing capacities and capabilities, though significant investment into electrolyzer manufacturing is also expected from Chinese and US companies while Indian and Australian players are also looking to enter the market. The electrolyzer market is currently dominated by alkaline and PEM electrolyzer manufacturers with comparatively few companies manufacturing or commercialising solid-oxide electrolyzers. However, the similarity between solid-oxide electrolyzers and solid-oxide fuel cells could provide an entry point for fuel cell manufacturers into the green hydrogen market. Certainly, growth in the electrolyzer market, across the three electrolyzer types, will be needed to meet ambitious national and regional targets for green and clean hydrogen production.

This report provides analysis and comparison of the electrolyzer technologies and designs being commercialised and developed. In addition, an overview of the market is provided, outlining key electrolyzer manufacturers and players, current manufacturing capacities, planned installations and regional green hydrogen production targets.

This report provides the following information:

Hydrogen market

Electrolyzer technology analysis

Electrolyzer market analysis

Table of Contents

ご注文は、お電話またはWEBから承ります。お見積もりの作成もお気軽にご相談ください。本レポートと同分野(その他)の最新刊レポート

IDTechEx 社の最新刊レポート本レポートと同じKEY WORD()の最新刊レポート

よくあるご質問IDTechEx社はどのような調査会社ですか?IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る 調査レポートの納品までの日数はどの程度ですか?在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

注文の手続きはどのようになっていますか?1)お客様からの御問い合わせをいただきます。

お支払方法の方法はどのようになっていますか?納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

データリソース社はどのような会社ですか?当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

|

詳細検索

2024/07/01 10:26 162.23 円 174.76 円 207.97 円 |