Summary

この調査レポートでは、DNAシーケンサ業界を取り上げ、関連する主要技術や市場について詳細に調査・分析しています。

主な掲載内容(目次より抜粋)

-

DNAシーケンシングの技術

-

DNAシーケンシング 市場

-

予測

Report Summary

This report covers the DNA sequencing industry, discussing the key technologies and markets involved. The report covers Sanger, Next-Generation (NGS), and nanopore sequencing, benchmarking these against each other on key metrics required by leading applications. The report includes in-depth analyses of DNA sequencing applications ranging from population genomics and companion diagnostics to forensics, identifying the requirements for each. Barriers of entry to the market and relevant challenges are analysed.

Since its inception, DNA sequencing has brought about major advancements in our understanding of biology. The DNA sequence encodes the biological information used by cells to develop and operate, and understanding the sequence of DNA is key to understanding the function of genes and other parts of the genome. The breadth of information this technology can offer has the potential to revolutionize healthcare, drug discovery, and many other fields. The importance of DNA sequencing has been further emphasized by the COVID-19 pandemic, which highlighted the need for infrastructure to effectively track and monitor outbreaks - a task well suited to DNA sequencing.

DNA sequencing technology has progressed in leaps and bounds over the years. The advent of next-generation sequencing (NGS) in 2004 lead to a rapid decrease in the costs of sequencing, with this reduction of cost far outpacing Moore's law. As a noteworthy example, market leader Illumina managed to lower the cost of a human whole genome sequence from an estimated US$1M in 2007, to US$1k in 2014. This drastic reduction of cost has led to a meteoric expansion of the sequencing market, with the number of related academic publications rising by more than 15 times between 2004 to 2014.

However, these developments have since slowed. The declining costs in sequencing have since tailed off, and technological developments have slowed. While this may be in part due to the difficulty of improving existing technology, a prominent reason for the slow progress has been a lack of competition in the industry.

Despite this, major changes may be approaching. The recent entry of third-generation sequencing technology into the market has served to reinvigorate the market and intensify competition, with their promise of ultra-long reads and real-time sequencing. The greater insight these devices can bring, along with their promise of further lowering costs of whole-genome sequencing, could lead to a new age of personalized medicine and greatly expand the sequencing market, bringing in the next revolution of DNA sequencing. Several significant recent developments have also been observed in the NGS market itself. Multiple start-ups have emerged, each with the aim of further lowering the costs of and improving the accuracy of sequencing. The imminent expiry of several key patents of a major player will also allow China-based genomics giant BGI to enter the US sequencing market, further escalating competition.

In this report, IDTechEx discusses the technologies involved in DNA sequencing. The report provides in-depth analyses of the sequencing methods employed by key players in the sequencing industry, including:

-

Sanger sequencing

-

Reversible terminator sequencing

-

Pyrosequencing

-

Proton detection sequencing

-

Sequencing-by-ligation

-

Single-molecule real-time (SMRT) sequencing

-

Nanopore sequencing

These technologies are benchmarked against each other to provide a comprehensive understanding of the technological landscape. Comparisons of sequencing platforms are also used to identify business strategies of various players, along with several unmet needs for current instruments.

Of the sequencing technologies discussed above, the third generation nanopore sequencing method is of particular interest. Nanopore sequencing can provide unprecedented read lengths, far exceeding that of any other sequencing method. However, what may be one of the most compelling arguments for nanopore sequencing is the that they may remove the need for many of the reagents needed for sequencing today; this could help significantly lower the cost of DNA sequencing. As such, this report explores the technology for the different components of nanopore sequencing in depth. A prominent drawback for nanopore sequencers today is their comparative lack of accuracy; this report analyzes current research directions for mitigation of this problem, along with addressing several further drawbacks of nanopore sequencing.

Enable Ginger

The report goes on to describe the various applications and business models for DNA sequencing, identifying the current and potential usage of sequencing in each. The requirements for sequencing instruments across a variety of applications are considered and discussed to help readers better identify suitable markets for a given sequencing platform. The report provides insight into the barriers of entry and challenges faced for current and prospective players, along with an analysis of the business models employed by various players across the entire industry. The report concludes by forecasting the future of the DNA sequencing market, covering the revenue forecast by market segment and by sequencing device generation up to 2033.

Enable GingerCannot connect to Ginger Check your internet connection

or reload the browserDisable in this text fieldRephraseRephrase current sentenceEdit in Ginger

Enable GingerCannot connect to Ginger Check your internet connection

or reload the browserDisable in this text fieldRephraseRephrase current sentenceLog in to edit with Ginger

Enable GingerCannot connect to Ginger Check your internet connection

or reload the browserDisable in this text fieldRephraseRephrase current sentenceEdit in Ginger

Enable GingerCannot connect to Ginger Check your internet connection

or reload the browserDisable in this text fieldRephraseRephrase current sentenceEdit in Ginger

Enable GingerCannot connect to Ginger Check your internet connection

or reload the browserDisable in this text fieldRephraseRephrase current sentenceLog in to edit with Ginger

ページTOPに戻る

Table of Contents

Enable Ginger

|

1. |

EXECUTIVE SUMMARY |

|

1.1. |

Executive introduction |

|

1.2. |

Use cases of sequencing |

|

1.3. |

Key industry drivers for sequencing |

|

1.4. |

Sequencing instrument roadmap |

|

1.5. |

Comparing sequencing methods |

|

1.6. |

Technological drivers for sequencing |

|

1.7. |

Challenges of DNA sequencing |

|

1.8. |

DNA sequencing instrument market |

|

1.9. |

Barriers of entry to the DNA instrument market |

|

1.10. |

Potential differentiating factors for sequencing |

|

1.11. |

NGS: notable technology trends and developments |

|

1.12. |

Potential improvements to nanopore sequencers |

|

1.13. |

Developmental trends for NGS and third-generation sequencing |

|

1.14. |

Key players in DNA sequencing by business model |

|

1.15. |

Requirements of sequencing platforms in different applications |

|

1.16. |

DNA sequencing services |

|

1.17. |

Market breakdown by segment and players |

|

1.18. |

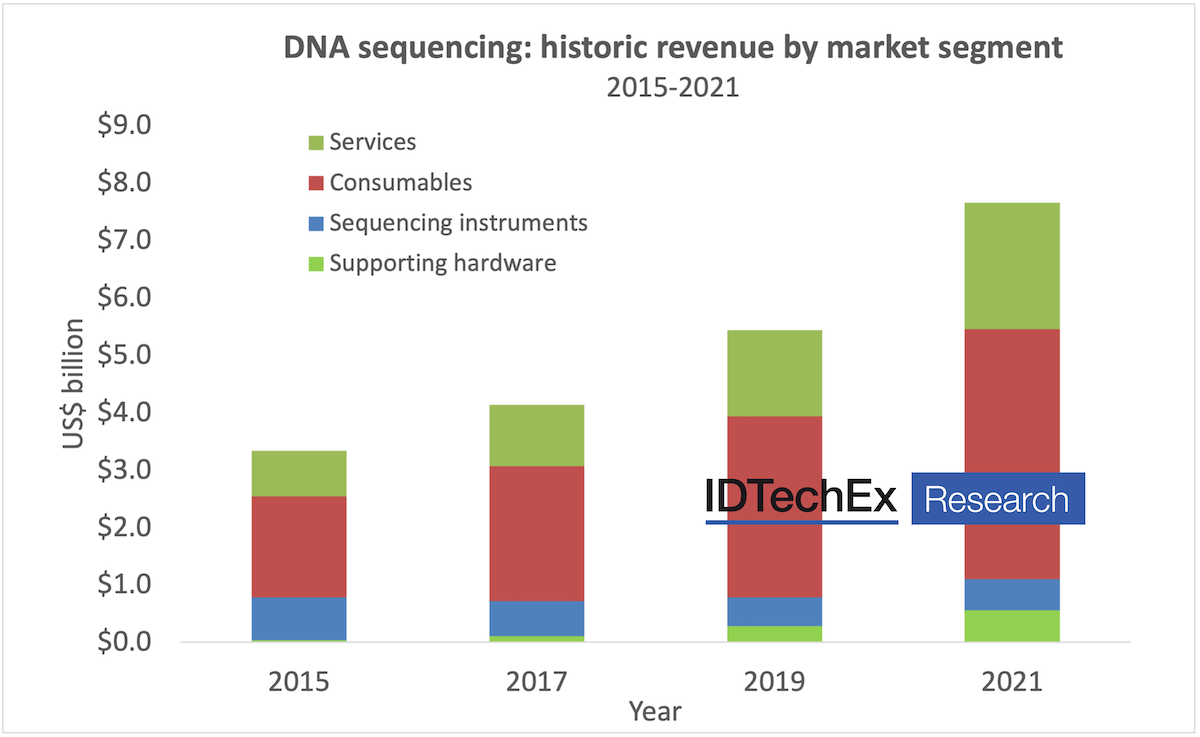

Global DNA sequencing revenue by market segment (2014-2033) |

|

1.19. |

DNA sequencing forecast revenue by market segment (2022-2033) |

|

1.20. |

Global revenue by sequencing device generation (2014-2033) |

|

1.21. |

Forecast revenue by sequencing device generation |

|

2. |

INTRODUCTION |

|

2.1. |

What is DNA? |

|

2.2. |

DNA sequencing |

|

2.3. |

DNA sequencing: timeline |

|

2.4. |

The history of the sequencing market |

|

2.5. |

The Human Genome Project |

|

2.6. |

Costs of DNA sequencing have fallen dramatically |

|

2.7. |

Use cases of sequencing |

|

2.8. |

Key industry drivers for sequencing |

|

2.9. |

Technological drivers for sequencing |

|

2.10. |

Challenges of DNA sequencing |

|

3. |

TECHNOLOGIES IN DNA SEQUENCING |

|

3.1.1. |

Sequencing instrument roadmap |

|

3.2. |

First generation sequencing |

|

3.2.1. |

First-generation sequencing: Sanger sequencing |

|

3.2.2. |

Key players in Sanger sequencing |

|

3.2.3. |

SCIEX/Danaher |

|

3.2.4. |

Thermo Fisher Scientific |

|

3.2.5. |

Sanger sequencing: Outlook |

|

3.3. |

Next-Generation Sequencing (NGS) |

|

3.3.1. |

Next-generation sequencing (NGS): introduction |

|

3.4. |

Sequencing-by-synthesis |

|

3.4.1. |

NGS approaches: Sequencing-by-synthesis |

|

3.4.2. |

Illumina |

|

3.4.3. |

Illumina: workflow |

|

3.4.4. |

Cluster generation |

|

3.4.5. |

Reversible terminator sequencing |

|

3.4.6. |

Illumina: Sequencing platforms |

|

3.4.7. |

Pyrosequencing: process |

|

3.4.8. |

Qiagen |

|

3.4.9. |

Roche: Efforts in DNA sequencing |

|

3.4.10. |

Proton detection sequencing: process |

|

3.4.11. |

Thermo Fisher: Ion Torrent |

|

3.4.12. |

ISFET sensors in Ion Torrent chips |

|

3.4.13. |

Element Biosciences |

|

3.4.14. |

Element Biosciences: Technology |

|

3.4.15. |

Ultima Genomics |

|

3.4.16. |

Ultima Genomics: Technology |

|

3.4.17. |

Ultima Genomics: Chemistry |

|

3.4.18. |

GenapSys: a cautionary tale of sequencing start-ups |

|

3.5. |

Sequencing-by-ligation |

|

3.5.1. |

NGS approaches: Sequencing-by-ligation |

|

3.5.2. |

Applied Biosystems/Thermo Fisher: SOLiD (I) |

|

3.5.3. |

Applied Biosystems/Thermo Fisher: SOLiD (II) |

|

3.5.4. |

Nanoball sequencing |

|

3.5.5. |

BGI Genomics: DNBSEQ |

|

3.6. |

Third generation sequencing |

|

3.6.1. |

Third generation sequencing |

|

3.6.2. |

Single molecule real-time sequencing: introduction |

|

3.6.3. |

Pacific Biosciences (PacBio) |

|

3.6.4. |

PacBio: Workflow |

|

3.6.5. |

PacBio: SWOT analysis |

|

3.6.6. |

Nanopore sequencing: overview |

|

3.6.7. |

Structure of a nanopore sequencer |

|

3.6.8. |

Why is nanopore sequencing important? |

|

3.6.9. |

Nanopore sequencing: operational principle |

|

3.6.10. |

Adaptive sampling |

|

3.6.11. |

Patent and research trends in nanopore sequencing |

|

3.7. |

Biological nanopores |

|

3.7.1. |

Biological nanopores: composition |

|

3.7.2. |

Comparison of protein characteristics |

|

3.7.3. |

Biological nanopores: Manufacturing methods |

|

3.7.4. |

Oxford Nanopore Technologies: Overview |

|

3.7.5. |

Oxford Nanopore Technologies: Patents |

|

3.7.6. |

Oxford Nanopore Technologies: Business model |

|

3.7.7. |

Oxford Nanopore Technologies: Products |

|

3.7.8. |

Roche |

|

3.7.9. |

Genia Technologies: Technology and patents |

|

3.7.10. |

Stratos Genomics: Technology and patents |

|

3.7.11. |

Qitan Technology |

|

3.7.12. |

Biological nanopores: strengths and weaknesses |

|

3.8. |

Solid-state nanopores |

|

3.8.1. |

Solid-state nanopores: overview |

|

3.8.2. |

Graphene nanopores |

|

3.8.3. |

Manufacturing methods: nanopore fabrication |

|

3.8.4. |

Manufacturing method: membrane thinning |

|

3.8.5. |

Comparison of manufacturing techniques |

|

3.8.6. |

Controlled dielectric breakdown shows several advantages over focused beam etching |

|

3.8.7. |

Hitachi |

|

3.8.8. |

Hitachi: patents |

|

3.8.9. |

What is stopping solid-state nanopores? |

|

3.8.10. |

IBM: DNA transistor |

|

3.9. |

Alternative structures for nanopore sequencers |

|

3.9.1. |

The motivation for alternative approaches to nanopore sequencing |

|

3.9.2. |

Plasmonic nanopores (I) |

|

3.9.3. |

Plasmonic nanopores (II) |

|

3.9.4. |

Base4 Innovation |

|

3.9.5. |

Hybrid nanopores: overview |

|

ページTOPに戻る

- 細胞分析市場の規模、シェアおよび動向分析レポート:製品・サービス別(試薬・消耗品、機器)、手法別(フローサイトメトリー、細胞マイクロアレイ)、プロセス別、用途別、地域別、およびセグメント別予測(2026年~2033年)

- 密閉型バイオプロセス市場規模、シェアおよび動向分析レポート:製品別(バイオリアクター、発酵槽、撹拌システム)、用途別(ワクチン製造、細胞・遺伝子治療)、最終用途別(製薬・バイオテクノロジー企業)、地域別、およびセグメント別予測(2026年~2033年)

- 免疫ゲノミクス市場規模、シェアおよび動向分析レポート:タイプ別(機器、消耗品、ソフトウェア)、技術別(ポリメラーゼ連鎖反応、マイクロアレイ)、用途別(臨床用途、研究用途)、エンドユーザー別、地域別、およびセグメント別予測(2026年~2033年)

- 凍結乾燥装置およびサービス市場規模、シェア、動向分析レポート:提供形態別(装置、サービス)、事業規模別(実験室規模、パイロット規模)、用途別(診断・研究、食品産業)、地域別、およびセグメント別予測(2026年~2033年)

- 合成遺伝子回路市場規模、シェアおよび動向分析レポート:製品別(トグルスイッチ回路、発振器)、用途別(研究、治療)、最終用途別(学術・研究機関、バイオテクノロジー・製薬企業)、地域別、およびセグメント別予測(2026年~2033年)

- ウイルスベクターおよびプラスミドDNA製造市場の規模、シェア、動向分析レポート:ベクタータイプ別(レンチウイルス、アデノウイルス、レトロウイルス)、ワークフロー別、用途別(遺伝子治療、細胞治療、ワクチン学)、最終用途別、疾患別(がん、遺伝性疾患)、地域別、およびセグメント別予測(2026年~2033年)

- 血小板濃縮血漿(PRP)市場規模、シェアおよび動向分析レポート:タイプ別(純粋PRP、白血球濃縮PRP)、用途別(整形外科、スポーツ医学、美容外科、皮膚科、眼科手術)、エンドユーザー別、地域別、およびセグメント別予測(2026年~2033年)

- 細胞培養培地および細胞株市場の規模、シェア、動向分析レポート:製品別(従来型細胞株、従来型培地)、用途別(バイオ医薬品製造、診断、研究・学術機関)、最終用途別、地域別、およびセグメント別予測(2026年~2033年)

- 製品別(消耗品(キット・試薬)、機器、ソフトウェア)、技術別(PCR、キャピラリー電気泳動、NGS、マイクロアレイ、迅速DNA分析)、用途別(法医学、親子鑑定)、エンドユーザー別の人類識別市場 ― 2031年までの世界予測

- Next-Generation Sequencing Market by Product Type (Consumables, Platforms, Bioinformatics), Technology (SBS, Nanopore), Workflow (Sequencing, Data Analysis), Services, Application (Drug Discovery, Diagnostic, Agriculture) - Global Forecast to 2030

本レポートと同じKEY WORD()の最新刊レポート

- 本レポートと同じKEY WORDの最新刊レポートはありません。

よくあるご質問

IDTechEx社はどのような調査会社ですか?

IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る

調査レポートの納品までの日数はどの程度ですか?

在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

但し、一部の調査レポートでは、発注を受けた段階で内容更新をして納品をする場合もあります。

発注をする前のお問合せをお願いします。

注文の手続きはどのようになっていますか?

1)お客様からの御問い合わせをいただきます。

2)見積書やサンプルの提示をいたします。

3)お客様指定、もしくは弊社の発注書をメール添付にて発送してください。

4)データリソース社からレポート発行元の調査会社へ納品手配します。

5) 調査会社からお客様へ納品されます。最近は、pdfにてのメール納品が大半です。

お支払方法の方法はどのようになっていますか?

納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

お客様よりデータリソース社へ(通常は円払い)の御振り込みをお願いします。

請求書は、納品日の日付で発行しますので、翌月最終営業日までの当社指定口座への振込みをお願いします。振込み手数料は御社負担にてお願いします。

お客様の御支払い条件が60日以上の場合は御相談ください。

尚、初めてのお取引先や個人の場合、前払いをお願いすることもあります。ご了承のほど、お願いします。

データリソース社はどのような会社ですか?

当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

世界各国の「市場・技術・法規制などの」実情を調査・収集される時には、データリソース社にご相談ください。

お客様の御要望にあったデータや情報を抽出する為のレポート紹介や調査のアドバイスも致します。

|

|

.png)