Low-Loss Materials for 5G and 6G 2024-2034: Markets, Trends, Forecasts5Gと6G向け低損失材料 2024-2034年:市場、動向、予測 この調査レポートでは、5Gおよび6G市場向け低損失材料の主要材料、プレーヤー、動向に関する広範な情報について詳細に調査・分析しています。 主な掲載内容(目次より抜粋) ... もっと見る

※ 調査会社の事情により、予告なしに価格が変更になる場合がございます。

Summary

この調査レポートでは、5Gおよび6G市場向け低損失材料の主要材料、プレーヤー、動向に関する広範な情報について詳細に調査・分析しています。

主な掲載内容(目次より抜粋)

Report Summary

Fifth-generation telecommunication technology, 5G, is more than a faster mobile experience to stream movies. It enables a universal connection between devices from automotive to remote robots. As profitable business models and killer applications start to emerge, 5G is one of the fastest growth markets, which IDTechEx forecasts to hit over US$842bn in 2033 and contribute trillions in annual connectivity boost to global GDP.

The most revolutionary aspect of the 5G network relies on high frequency 5G technologies, i.e. mmWave 5G, which utilize the spectrum from 26 GHz up to 40 GHz. At such high frequencies, many technologies and devices are facing challenges such as significant transmission loss, higher power usage needing more efficient power supply, and excess heat generation. Transmission loss is a pain point for both 5G antennas and radio frequency integrated circuits. For low frequency 5G, i.e. sub-6 GHz 5G, due to the high data transfer speed, reducing signal loss is also desirable.

.png)

Figure 1: Overview of challenges, trends and innovations for mmWave 5G, source: IDTechEx

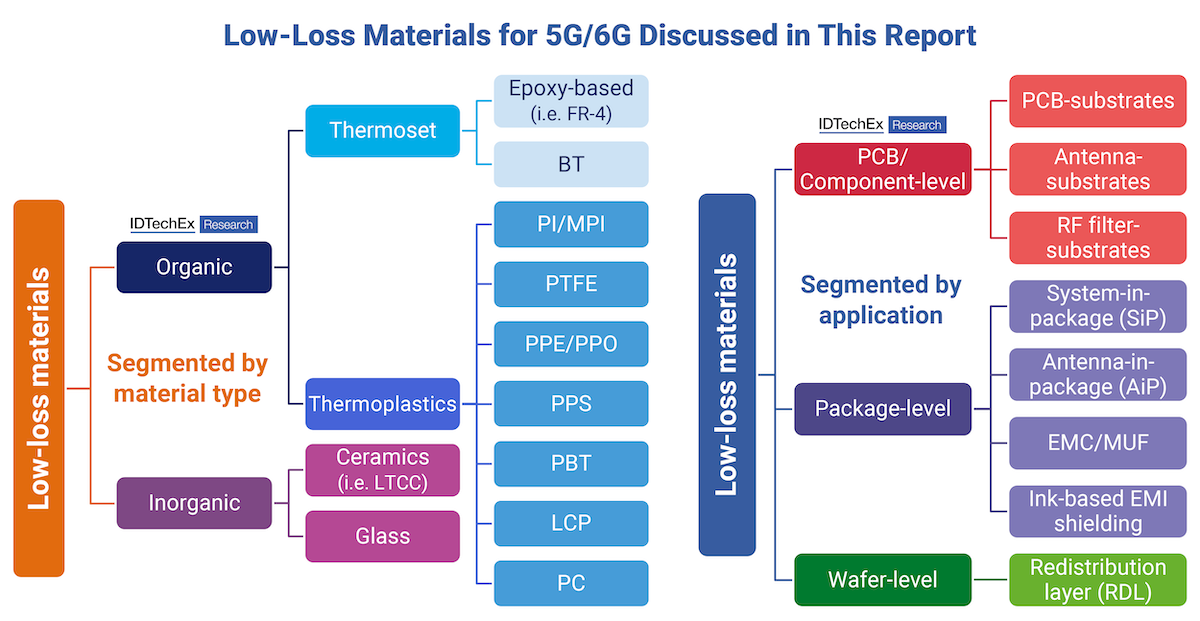

With the future rise of mmWave 5G, low-loss materials will experience rapid growth and play an increasingly important role. In this report, we survey the landscape of the low-loss materials and benchmark their performance by five key factors, i.e. dielectric constant (Dk), dissipation factor (Df), moisture absorption, cost and manufacturability. Low-loss materials will not only be used as a substrate for RF components or for the PCB, but also within advanced packages. One strong packaging trend is antenna in package (AiP); as telecom technology goes higher in frequency towards mmWave 5G, the size of the antenna elements will shrink such that the arrays can be fitted into the package itself. This integration will also help shorten the RF paths and thus minimize the transmission losses. AiP will need low-loss materials for the substrates, redistribution layers, electromagnetic interference (EMI) shielding, mold underfill (MUF) materials, and more.

Figure 2: Scope of the low-loss materials covered in the report, source: IDTechEx

We highlight promising low-loss materials for 5G devices. This includes:

Additionally, though the 6G spectrum is years from being allocated, research institutions and materials suppliers are already exploring the material requirements needed to meet the next generation of telecommunication technologies. This report explores the approaches to achieve even lower Df/Dk and the potential 6G applications, like reconfigurable intelligent surfaces (RIS).

Ten-year granular forecasts focusing on low-loss materials area and revenue for 5G devices are presented in this report, with over five forecast lines. The forecasts are segmented by:

.png)

Figure 3: Forecast and growth rate of low-loss materials for 5G, source: IDTechEx

Based on materials trends, we forecast the low-loss materials revenue for 5G devices from 2024 to 2034. The total market will hit US$2.1 billion USD by 2034. The report contains a comprehensive analysis of different low-loss materials from different perspectives such as performance, technology trends, potential, and bottlenecks for large scale deployment. Importantly, the report presents an unbiased analysis of primary data gathered via our interviews with players across the supply chain, and it builds on our large database of 5G infrastructure and user equipment data.

Key questions answered in this report:

Key aspects

This report provides extensive information and analysis on the major materials, players, and trends for low-loss materials for the 5G and 6G markets.

Material trends for low-loss materials and manufacturer analysis:

Market Forecasts & Analysis:

Table of Contents

株式会社 データリソース Data Resource, Inc.

電話:03-3582-2531

COPYRIGHT(C) 2011-2025 DATA RESOURCE, Inc. ALL RIGHTS RESERVED. |