Summary

この調査レポートは、IDTechExが自動車分野で使用されるディスプレイを初めて詳細に調査し、この分野で利用可能な様々なディスプレイ技術について詳細に調査・分析しています。

主な掲載内容(目次より抜粋)

-

車載ディスプレイ分野の主要トレンド

-

市場予測

-

ディスプレイ技術

-

ディスプレイ・コンポーネント

Report Summary

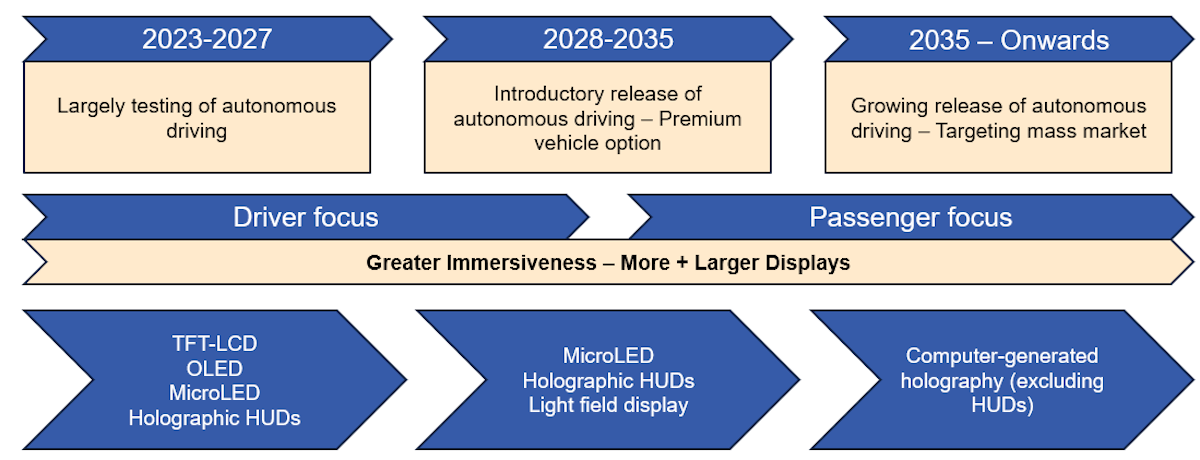

The next generation automotive displays promise to revolutionize our driving experience, with a greater number of larger displays being made available per vehicle. The rise in vehicle autonomy will coincide with the shift in focus by OEMs in enhancing the passenger experience when compared to the traditional driver experience. IDTechEx's new report evaluates the current and future display technologies made available to the automotive industry and an in-depth analysis to the feasibility of adopting these technologies on different in-vehicle displays. Interviews with key players in the market helped shape this forecast with the market expected to reach over US$27 billion by 2034.

This report is IDTechEx's first in-depth coverage into displays used in the automotive sector and assesses the different display technologies available in this space. The effectiveness of these technologies is dependent on where they are placed. A dashboard display, for instance, requires a technology with high brightness and lifetime, to ensure passenger safety while driving. TFT-LCD displays are a popular choice because they cover these requirements and have an added benefit of being cost effective compared to alternative displays. Centre information displays (CID) and console side panels, on the other hand, appear to be favouring flexibility and as a result, the adoption of OLED technology is witnessing a notable increase in demand. These design criteria reflect the current state of the market with the availability and cost of these technologies playing a fundamental role in the selection process, however, the next decade is expected to bring even more innovation with the expected emergence and growing importance of microLEDs. It is predicted these devices will exhibit enhanced image quality and contrast, high brightness, low power consumption, high lifetime and endure harsh ambient conditions, all important features in modern automotive displays. They are expected to greatly surpass the performance of TFT-LCDs and OLEDs, however, their high cost and sub-optimal yields, have hindered their growth in the market.

Emerging display types such as heads-up displays (HUDs) and side window displays are also covered in this report along with an analysis of what the key players are delivering in terms of technology, either the stereoscopic TFT-LCD or the three-dimensional computer-generated holography and light field displays.

While these three-dimensional technologies are still farfetched for most applications, some companies have been successful in advocating and showcasing its effectiveness in HUDs. Despite this growing interest, TFT-LCDs remain the dominant supplying HUDs, although this decade will present some interesting innovation on this front.

Figure 1: Rise in vehicle autonomy will influence the automotive display sector in the coming decade. Source: IDTechEx

The main distinction to this report, however, is the understanding that displays are a lot more than these technologies. Especially in automotive, there are a lot of components that make up a display, from its cover glass to diffusers and adhesives. This report provides a holistic perspective onto modern displays and attempts to inform the reader of the most recent advancements made to this industry from a wider perspective.

Key players are assessed, as well as forecasts into the next decade covering 2024-2034. The forecasts are broken down by display technology and type of display. A regional breakdown is provided covering display type volumes.

Drivers and constraints are considered throughout the report, as well as technology maturity, competitive landscape, and ongoing trends in the market. Interviews with numerous players in this space - both display manufacturers and their suppliers - are conducted, and findings are presented giving the reader insight into where the market is placed and where it is moving. The progress of individual companies is outlined in the report and their product lines assessed and compared with similar competition.

Key aspects of the automotive displays market report

The research in this report has been compiled by IDTechEx analysts following our existing expertise in microLEDs and photonics to electric vehicles and vehicle autonomy. Primary and secondary research was fundamental when putting together this report, speaking to multiple stakeholders in the sector with both a commercial and academic focus on the subject. IDTechEx has attended conferences and tradeshows, to understand the market and validate some hypotheses. The information and data gathered was helpful when conceiving this uniquely comprehensive report.

This report provides an overall assessment of into the automotive display landscape and covers fundamental technologies, product lines, applications, and key players. Key features of this report include:

-

An introduction to different types of automotive display technologies and types of displays.

-

Discussion of key trends and sector movements.

-

Industry analysis from multiple interviews conducted and conferences attended.

-

Several SWOT analyses covering key technologies.

-

Analysis into technologies beyond display technologies. A holistic approach to displays, covering technologies that supply displays, cover glass, diffusers, driver ICs.

-

10-year market forecast, across multiple display types and technologies. Includes annual market value and display volume forecasts.

Key regions are covered:

-

Europe

-

America

-

Asia/Middle East/Oceania

-

Africa

-

Central and South America

-

USA

-

China

-

India

-

Japan

-

South Korea

ページTOPに戻る

Table of Contents

|

1. |

EXECUTIVE SUMMARY |

|

1.1. |

Key topics covered in report |

|

1.2. |

What are automotive displays - how have they evolved? |

|

1.3. |

Types of automotive displays |

|

1.4. |

Types of automotive displays (2) |

|

1.5. |

Display design trends |

|

1.6. |

OEM expected display technology priorities over time |

|

1.7. |

Shift to 3D coincides with rise in autonomous vehicles and focus on passenger experience |

|

1.8. |

OEM shift in display focus by display type |

|

1.9. |

Display eco-system |

|

1.10. |

Multiple display technologies in use |

|

1.11. |

Multiple display technologies in use |

|

1.12. |

What do LCDs offer to the automotive sector? |

|

1.13. |

How is OLED competing in the automotive sector |

|

1.14. |

What do microLEDs bring to the automotive sector? |

|

1.15. |

Why adopt spatial LFDs |

|

1.16. |

What CGH brings to displays |

|

1.17. |

How is TFEL competing in the display market |

|

1.18. |

Global volume forecast by display type |

|

1.19. |

Europe volume forecast by display type |

|

1.20. |

America volume forecast by display type |

|

1.21. |

Asia/Oceania/Middle East volume forecast by display type |

|

1.22. |

Africa volume forecast by display type |

|

1.23. |

Global volume forecast by display technology |

|

1.24. |

Global total automotive display market value |

|

2. |

KEY TRENDS IN THE AUTOMOTIVE DISPLAY SECTOR |

|

2.1. |

Display manufacturing priorities |

|

2.2. |

Display design trends |

|

2.3. |

OEM expected display technology priorities over time |

|

2.4. |

Current battle between TFT-LCD and OLED |

|

2.5. |

Next generation display technologies |

|

2.6. |

Shift to 3D coincides with rise in autonomous vehicles and focus on passenger experience |

|

3. |

MARKET FORECASTS |

|

3.1. |

Forecast introduction and assumptions |

|

3.2. |

Global volume forecast by display type |

|

3.3. |

Europe volume forecast by display type |

|

3.4. |

America volume forecast by display type |

|

3.5. |

Asia/Oceania/Middle East volume forecast by display type |

|

3.6. |

Africa volume forecast by display type |

|

3.7. |

USA volume forecast by display type |

|

3.8. |

Central and South America volume forecast by display type |

|

3.9. |

China volume forecast by display type |

|

3.10. |

Japan volume forecast by display type |

|

3.11. |

South Korea volume forecast by display type |

|

3.12. |

India volume forecast by display type |

|

3.13. |

Global volume forecast by display technology |

|

3.14. |

Explanation on forecast by display technology |

|

3.15. |

Global total automotive display market value |

|

4. |

INTRODUCTION TO AUTOMOTIVE DISPLAYS |

|

4.1.1. |

What are automotive displays - how have they evolved? |

|

4.1.2. |

Types of automotive displays |

|

4.1.3. |

Applied fields of automotive display |

|

4.1.4. |

Displays beyond cars |

|

4.1.5. |

The future of displays |

|

4.1.6. |

Section structure |

|

4.2. |

Driver Focus |

|

4.3. |

Dashboard Displays |

|

4.3.1. |

Dashboard display latest trends |

|

4.3.2. |

Dashboard evolution |

|

4.3.3. |

Where next? Possible paths for the dashboard display |

|

4.4. |

CID Displays |

|

4.4.1. |

CID display requirements |

|

4.4.2. |

Current and future trends of CID displays |

|

4.4.3. |

Companies by technology |

|

4.5. |

Heads-Up Displays (HUDs) |

|

4.5.1. |

Rising importance of HUDs |

|

4.5.2. |

Introduction to HUDs |

|

4.5.3. |

From military aviation to the future of automotive displays - a brief historical overview of HUDs |

|

4.5.4. |

Evolution of HUD for automotive |

|

4.5.5. |

A selection of automotive with HUDs |

|

4.5.6. |

Companies by technology |

|

4.6. |

Passenger Focus |

|

4.7. |

Side Window Display |

|

4.7.1. |

Outlook on side window displays |

|

4.7.2. |

Rise in side window displays |

|

4.7.3. |

Side window displays technology examples |

|

4.7.4. |

Side window display players |

|

4.8. |

Front window (outward) displays |

|

4.8.1. |

Front window (outward communication) displays |

|

4.9. |

Passenger Virtual Reality |

|

4.9.1. |

What are Virtual, Augmented, Mixed and Extended Reality? |

|

4.9.2. |

Use of VR in automotive? |

|

5. |

KEY FEATURES REQUIRED IN THE AUTOMOTIVE DISPLAYS SECTOR |

|

5.1. |

Image quality comparison |

|

5.2. |

Image brightness comparison |

|

5.3. |

Flexibility - form factor comparison |

|

5.4. |

Durability/resilience comparison |

|

5.5. |

Response times |

|

5.6. |

Display lifetime |

|

6. |

DISPLAY TECHNOLOGIES |

|

6.1.1. |

Evolution of displays |

|

6.1.2. |

21st Century - The time for flat screen panels and the rise of LCD technology |

|

6.2. |

Thin-Film Transistor-Liquid Crystal Display (TFT-LCD) |

|

6.3. |

TFT-LCD Overview |

|

6.3.1. |

The rise of thin-film transistor liquid crystal displays (TFT-LCDs) |

|

6.3.2. |

The legacy variant - twisted nematic liquid crystal |

|

6.3.3. |

TFT-based in-plane switching (IPS) technology |

|

6.3.4. |

Vertical alignment (VA) LCDs |

|

6.3.5. |

TN vs IPS vs VA |

|

6.3.6. |

TFT-LCD automotive display value propositions |

|

6.3.7. |

Automotive Display Component Assembly |

|

6.3.8. |

Typical TFT-LCD based display component layout |

|

6.4. |

TFT-LCD Backlight Technologies |

|

6.5. |

Light Emitting Diodes (LEDs) |

|

6.5.1. |

History of solid-state lighting |

|

6.5.2. |

What is an LED? |

|

6.5.3. |

How does an LED work? |

|

6.5.4. |

Homojunction vs heterojunction |

|

6.5.5. |

LEDs by package technique 1 |

|

6.5.6. |

LEDs by package technique 2 |

|

6.5.7. |

Typical LED and packaged LED sizes |

|

6.5.8. |

LED size definitions |

|

6.6. |

MiniLEDs |

|

6.6.1. |

MiniLED - Moving past LED and towards full-array local dimming |

|

6.6.2. |

MiniLEDs are facilitating local dimming in LCDs to achieve HDR and higher image contrasts |

ページTOPに戻る

本レポートと同じKEY WORD()の最新刊レポート

- 本レポートと同じKEY WORDの最新刊レポートはありません。

よくあるご質問

IDTechEx社はどのような調査会社ですか?

IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る

調査レポートの納品までの日数はどの程度ですか?

在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

但し、一部の調査レポートでは、発注を受けた段階で内容更新をして納品をする場合もあります。

発注をする前のお問合せをお願いします。

注文の手続きはどのようになっていますか?

1)お客様からの御問い合わせをいただきます。

2)見積書やサンプルの提示をいたします。

3)お客様指定、もしくは弊社の発注書をメール添付にて発送してください。

4)データリソース社からレポート発行元の調査会社へ納品手配します。

5) 調査会社からお客様へ納品されます。最近は、pdfにてのメール納品が大半です。

お支払方法の方法はどのようになっていますか?

納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

お客様よりデータリソース社へ(通常は円払い)の御振り込みをお願いします。

請求書は、納品日の日付で発行しますので、翌月最終営業日までの当社指定口座への振込みをお願いします。振込み手数料は御社負担にてお願いします。

お客様の御支払い条件が60日以上の場合は御相談ください。

尚、初めてのお取引先や個人の場合、前払いをお願いすることもあります。ご了承のほど、お願いします。

データリソース社はどのような会社ですか?

当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

世界各国の「市場・技術・法規制などの」実情を調査・収集される時には、データリソース社にご相談ください。

お客様の御要望にあったデータや情報を抽出する為のレポート紹介や調査のアドバイスも致します。

|