Automotive Semiconductors 2023-2033車載用半導体 2023-2033年 この調査レポートは、電動化や自律走行車(AV)といった自動車業界のメガトレンドが、半導体業界に新たな成長と機会をもたらしていることを深く掘り下げている。 主な掲載内容(目次より抜粋... もっと見る

※ 調査会社の事情により、予告なしに価格が変更になる場合がございます。

Summary

この調査レポートは、電動化や自律走行車(AV)といった自動車業界のメガトレンドが、半導体業界に新たな成長と機会をもたらしていることを深く掘り下げている。

主な掲載内容(目次より抜粋)

Report Summary

The "Automotive Semiconductors 2023-2033" report provides a deep dive into how megatrends in the automotive industry, such as electrification and autonomous vehicle (AV) are bringing new growth and opportunity to the semiconductor industry. These trends require new componentry on vehicles, such as LiDAR in automation, and with them new semiconductors, such as indium phosphate laser emitters. Eighteen components across the areas of advanced driver assistance systems, automated driving, electrification, communications & infotainment, and general MCU architectures are analysed for semiconductor content and trends which will impact semiconductor technologies used.

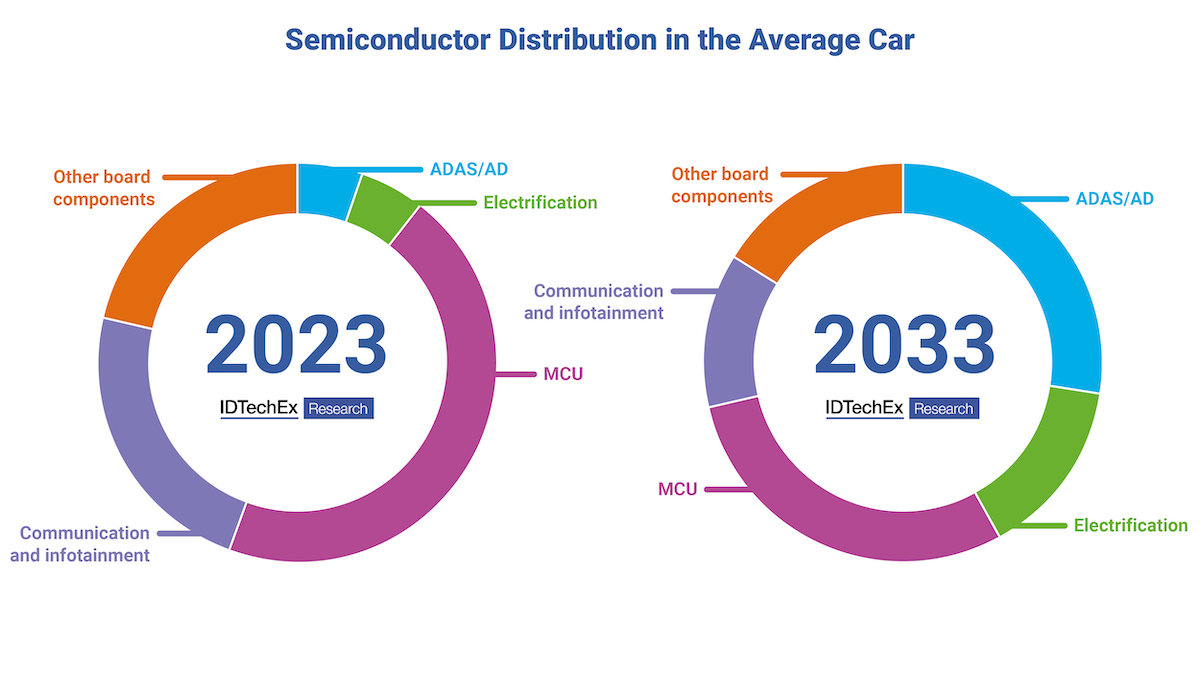

Semiconductor technology is at the heart of all modern vehicles. Their presence and prevalence have risen rapidly over the past couple of decades in the form of microcontrollers which now govern almost all aspects of vehicle operation. They communicate inputs, execute actuations and perform calculations across the entire car. This has transformed the public's perception of vehicles into "computers on wheels". Unsurprisingly, and as shown in the graphic below, automotive MCUs are the leading component for generating semiconductor value within the vehicle.

Semiconductor wafer value in the average vehicle today, and in 2033.

Source: IDTechEx

IDTechEx's "Automotive Semiconductors 2023-2033" report finds that the value of MCUs within vehicles is going to continue to grow. This will contribute to a wafer revenue CAGR of 9.4%, but much of the growth is going to be driven by growing semiconductor demand within advanced driver assistance systems (ADAS), autonomous vehicles (AV) and vehicle electrification. Not only will these new components require additional MCUs, but the advanced and intensive processing undertaken in automated driving is seeing the adoption of more cutting-edge semiconductor technologies into the vehicle.

Semiconductors for ADAS and autonomous vehicles, a rapidly growing sector

ADAS and autonomous vehicles promise to revolutionise the transportation industry with the superhuman safety they can offer. Providing these superhuman capabilities are a suite of sensors and computers that rely on advanced semiconductor technologies to function and provide the best performance. As such ADAS and autonomous vehicles are going to be a great boon to the automotive semiconductor market. According to the findings of this report the semiconductor wafer revenue for ADAS and AV applications will grow at a 10-year CAGR of 29%. There are three factors that combine to drive this high growth rate:

1. The emergence and adoption of SAE level 3 and SAE level 4 autonomous vehicles and the additional sensors required.

2. Automotive sensors transitioning to more advance semiconductors.

3. High performance computing coming to vehicles.

This report explains all these trends in detail and their impact on the semiconductor markets. Of particular interest is the growth of non-silicon-based semiconductor demand driven by LiDAR. Most LiDARs today operate in the near infrared (NIR) region with a typical wavelength of 905nm, which can be achieved with silicon photodetectors. However, the future of LiDAR is likely to use the shortwave infrared (SWIR) region with a typical wavelength of 1,550nm. This trend within the industry is demonstrated by the overwhelming dominance of 1,550nm LiDAR announcements shown in the chart below. Details pertaining to the superiority of 155nm LiDARs and the impact the switch has on changing demand across different semiconductor technologies are covered in this report.

.png)

Source: IDTechEx

While Tesla has been publicly anti-lidar, other key players in the autonomy space such as Waymo, Cruise, Daimler and Honda are all using LiDAR on their highly automated vehicles. In fact, as of the end of 2022 there have only been two vehicles certified for SAE level 3 use (where the driver's attention is not required under certain conditions) on the road; the Mercedes S-Class and the Honda Legend. IDTechEx is expecting many more high-end vehicles to follow the S-Class over the next 10-years, and for level 3 technologies to be widely available. This will of course drive semiconductor demand across all the sensor types and computers that are needed for these highly advanced vehicles. But another major trend in the automotive market that will impact semiconductor demand is electrification.

Semiconductors for automotive electrification

The automotive industry is under increasing pressure to decarbonise through electrification and In 2022 electric vehicles (EV) sales rose to approximately 10% of all new vehicle sales. EV's are now heading out of the early adopter phase and towards the early majority and wider spread adoption. EVs, their power electronics and their battery packs bring additional demands that drive more growth within the semiconductor industry.

OEMs are always looking for ways to extend range by making the vehicles more efficient and one avenue increasing in popularity is moving from inverters based on silicon to ones based on silicon carbide There are two factors that are pushing electric vehicle OEMs such as Tesla, Mercedes, Audi and Ford towards silicon carbide. Firstly, some OEMs are planning to transition from 400V to 800V architectures. The higher voltage reduces the amount of current required to achieve the same power, this means reduced wastage in the powertrain system from Ohmic losses and increased efficiency. Silicon carbide is much more suited to the higher voltage and is therefore the more sensible choice than Si. However, and the second reason for adoption, silicon carbide is also more efficient than Si at 400V, which is why players like Tesla are interested even though it would struggle to transition to 800V with its existing 400V supercharger network. This report covers the pros and cons of silicon, silicon carbide and the even more nascent gallium nitride, and explains how these new technologies are going to impact the semiconductor wafer market.

The trends mentioned here are forecasted over a 10-year period to 2033 giving wafer volumes, revenues and raw material demand over ADAS and AV, electrification communication and infotainment and vehicle MCUs. For even more granular detail a database with over 400 forecast lines is available with this report. It covers 18 components, across four key vehicle areas, and considering four levels of automation and three different powertrain types (ICE, EV and PHEV), providing wafer volumes, revenues, raw material demand and more.

Key aspects

Market Forecasts:

10-year granular market forecasts of

10-year market forecasts split by

Table of Contents

株式会社 データリソース Data Resource, Inc.

電話:03-3582-2531

COPYRIGHT(C) 2011-2025 DATA RESOURCE, Inc. ALL RIGHTS RESERVED. |