サマリー

この調査レポートでは、業界の今後10年間の金属印刷用ハードウェアと金属3D印刷材料の需要について詳細に調査・分析しています。市場での豊富な歴史と多数の一次取材に基づき、過去2年間のCOVID-19の大流行による影響と回復を含め、公平な市場予測を提供しています。

主な掲載内容(目次より抜粋)

-

金属印刷プロセス

-

新しい金属印刷プロセス

-

メタルプリンター:比較とベンチマーキング

-

3Dプリンティング用金属材料

-

適合する金属材料

Report Summary

After initial commercialization in the 1990s, metal additive manufacturing (also referred to as 3D printing of metals) has witnessed a flurry of interest in recent years. Key players have been quick to capitalize on this demand, enjoying exponential revenue growth since 2013 as a result.

This comprehensive technical report from IDTechEx gives the detailed status and outlook for the industry. Built upon an extensive history in the market and large number of primary interviews, this report provides an unbiased forecast for the market, including the impact and recovery from the COVID-19 pandemic in the past two years.

Granular forecasts and detailed player profiles

This report provides granular 10-year market forecasts for the industry. The demand for metal printing hardware and metal 3D printing materials in the next decade is quantified. Targeted quantitative analysis is given for printer technologies and materials, broken down into 10 technology segments and 9 materials segments.

These forecasts are generated by the IDTechEx analyst team. The analysts go far beyond what is publicly available by conducting an extensive number of primary interviews, providing the latest and most important information to the reader. Over 75 company profiles are included as part of this report; this includes key OEMs, disruptive start-ups, incumbent powder providers, and emerging material companies.

Benchmarking the competitive printer processes

The proposed advantages to metal additive manufacturing are numerous with design freedom, local versatile manufacturing, potential cost savings, shortened manufacturing times, and much more.

To exploit this there is an ever-expanding family of printer processes using a wide number of material feedstocks. A common tactic for new entrants is to invent new terms for their technology to differentiate from the competition. Some of these are unique but most are aligned with existing processes, introducing only subtle variations.

This report cuts through this marketing and provides accessible impartial categorization for the industry. The reality is that every process must compromise on something, be it the rate, price, precision, size, material compatibility, or more. IDTechEx provide critical benchmarking studies of these processes: an essential process for identifying gaps in the market and end-use applications.

There is also the learning curve to be considered. As with any new (primarily) B2B technology with a large price-tag, it will take time for end-users to have confidence in the process and value-add to warrant the investment. Powder bed fusion processes (DMLS, SLM, and EBM) have been commercial for the longest time, which results in this technology underpinning most installations. However, the next generation of technologies is gaining more traction and within the next decade a more diverse installation base will be observed.

There are some overarching trends for new entrants as they try to find gaps in the market. Low-cost variants, printers pushing the size extremes from micro to very large scales, faster rates, and those exploiting alternative forms of feedstocks are all rapidly emerging and assessed.

Expanding material portfolio, capacity, and competition

IDTechEx forecast that the majority of annual revenue will come from material demand rather than printer sales and installation. Every printer process and application has different material requirements, throughput rates, and alloy demands.

There is a large amount of movement in this industry with notable acquisitions, capacity expansions, improved atomization processes, new materials, and cost reductions. Players are introducing material portfolios bespoke for additive manufacturing from well-known structural alloys to advanced options such as MMCs, high entropy alloys, and amorphous alloys.

Given the variation across this industry, there are very different forecasts when considering cost and volume; titanium powder will be the most significant which is again evident from the market dynamics of expansions, investments, vertical integration and exploring new avenues such as the use of scrap feedstocks.

Key markets and the impact of COVID-19

Metal additive manufacturing has been used for prototypes, tooling, replacement parts, and small to large manufacturing. There are multiple sectors in which this emerging technology is gaining significant uptake, including oil & gas, jewelry, and building & construction. The growth and adoption have all been in high-value industry verticals and the long-term future looks very optimistic.

That said, the COVID-19 global pandemic rapidly introduced new opportunities and concerns for the industry. One opportunity has arisen from major disruptions in global supply chains, which is new interest in distributed manufacturing operations. As international manufacturers address vulnerabilities in their supply chain, metal additive manufacturing has the potential to position itself as a key component in solving supply chain issues. On the other hand, key markets like aerospace face prolonged recovery from pandemic effects. This report analyzes the many trends and global market factors impacting metal additive manufacturing within the decade.

This market report gives granular forecasts for technologies and materials taking into account the impact of COVID-19.

Key questions that are answered in this report

-

What are the current and emerging printer technology types?

-

How do metrics such as price, build speed, build volume and precision vary by printer type?

-

What are the strengths and weaknesses of different 3D printing technologies?

-

Which printers support different material feedstock?

-

What is the current installed base of metal 3D printers?

-

What is the price range of 3D metal printers by technology type?

-

What are the market shares of those active in the market?

-

What are the key drivers and restraints of market growth?

-

Who are the main players and emerging start-ups?

-

How will sales of different printer types evolve from 2022 to 2032?

-

What was the impact of the COVID-19 pandemic on metal 3D printing in 2020 and 2021?

ページTOPに戻る

目次

|

1. |

EXECUTIVE SUMMARY |

|

1.1. |

Metal Additive Manufacturing: Technology Overview |

|

1.2. |

Metal 3D Printing Technologies: Benchmarking Overview |

|

1.3. |

Market Forecast for Metal Additive Manufacturing |

|

1.4. |

Metal 3D Printing Continues Seeing Innovation |

|

1.5. |

Material-Process Relationships |

|

1.6. |

Timeline of 3D Printing Metals |

|

1.7. |

Drivers and Restraints of Growth for 3D Printing |

|

1.8. |

Impact of COVID-19: Summary of Company Perspectives |

|

1.9. |

Revenue Recovery from COVID-19 in 2020 and 2021 |

|

1.10. |

COVID-19 and 3D Printing: Takeaways |

|

1.11. |

Metal 3D Printing Investment Overview for 2021 |

|

1.12. |

Companies Going Public in 2021: Summary |

|

1.13. |

Technology Segmentation |

|

1.14. |

Technology Installed Base and Market Share in 2022 |

|

1.15. |

Technology Installed Base and Market Share in 2032 |

|

1.16. |

Market Share by Mass of Metals Demand by Alloy |

|

1.17. |

Metal Hardware Revenue Forecast by Technology |

|

1.18. |

Metal Material Forecast By Technology - Revenue and Mass |

|

1.19. |

Metal Material Forecast by Technology - Discussion |

|

1.20. |

Metal Material Forecast By Alloy - Revenue and Mass |

|

1.21. |

Metal Material Forecast by Alloy - Discussion |

|

1.22. |

Key Trends in Metal Additive Manufacturing |

|

1.23. |

Key Trends in Metal Additive Manufacturing |

|

1.24. |

Company Profiles |

|

2. |

INTRODUCTION |

|

2.1. |

Glossary: common acronyms for reference |

|

2.2. |

Scope of Report |

|

2.3. |

The Different 3D Printing Processes |

|

2.4. |

Material-Process Relationships |

|

2.5. |

Why Adopt 3D Printing? |

|

2.6. |

Timeline of 3D Printing Metals |

|

2.7. |

Business Models: Selling Printers vs Parts |

|

2.8. |

The Desktop 3D Printer Explosion |

|

2.9. |

Drivers and Restraints of Growth for 3D Printing |

|

2.10. |

Computer Aided Engineering (CAE): Topology |

|

3. |

METAL PRINTING PROCESSES |

|

3.1. |

Powder Bed Fusion: Direct Metal Laser Sintering (DMLS) |

|

3.2. |

Powder Bed Fusion: Electron Beam Melting (EBM) |

|

3.3. |

Directed Energy Deposition: Powder |

|

3.4. |

Directed Energy Deposition: Wire |

|

3.5. |

Binder Jetting: Metal Binder Jetting |

|

3.6. |

Binder Jetting: Sand Binder Jetting |

|

3.7. |

Sheet Lamination: Ultrasonic Additive Manufacturing (UAM) |

|

4. |

NEW METAL PRINTING PROCESSES |

|

4.1. |

Emerging Printing Processes - Overview |

|

4.2. |

Extrusion: Metal-Polymer Filament (MPFE) |

|

4.3. |

Extrusion: Metal-Polymer Pellet |

|

4.4. |

Extrusion: Metal Paste |

|

4.5. |

Vat Photopolymerisation: Digital Light Processing (DLP) |

|

4.6. |

Material Jetting: Nanoparticle Jetting (NPJ) |

|

4.7. |

Material Jetting: Magnetohydrodynamic Deposition |

|

4.8. |

Material Jetting: Electrochemical Deposition |

|

4.9. |

Material Jetting: Cold Spray |

|

4.10. |

Binder Jetting Advancements |

|

4.11. |

Developments in PBF and DED: Energy Sources |

|

4.12. |

Developments in PBF and DED: Low-Cost Printers |

|

4.13. |

Developments in PBF and DED: New Technologies |

|

4.14. |

Processes with a Metal Slurry Feedstock |

|

4.15. |

Alternative Emerging DMLS Variations |

|

5. |

METAL PRINTERS: COMPARISON AND BENCHMARKING |

|

5.1. |

Metal Additive Manufacturing: Technology Overview |

|

5.2. |

Benchmarking: Maximum Build Volume |

|

5.3. |

Benchmarking: Build Rate |

|

5.4. |

Benchmarking: Z Resolution |

|

5.5. |

Benchmarking: XY Resolution |

|

5.6. |

Benchmarking: Price vs Build Volume |

|

5.7. |

Benchmarking: Price vs Build Rate |

|

5.8. |

Benchmarking: Price vs Z Resolution |

|

5.9. |

Benchmarking: Build Rate vs Build Volume |

|

5.10. |

Benchmarking: Build Rate vs Z Resolution |

|

5.11. |

Overview of Metal 3D Printing Technologies |

|

5.12. |

Maximums & Minimums of Metal 3D Printing Technologies |

|

6. |

METAL MATERIALS FOR 3D PRINTING |

|

6.1. |

Material feedstock options |

|

6.2. |

Powder morphology specifications |

|

6.3. |

Water or gas atomisation |

|

6.4. |

Plasma atomisation |

|

6.5. |

Electrochemical atomisation |

|

6.6. |

Powder morphology depends on atomisation process |

|

6.7. |

Evaluation of powder manufacturing techniques |

|

6.8. |

Supported materials |

|

6.9. |

Suppliers of metal powders for AM |

|

6.10. |

Suppliers of metal powders for AM |

|

6.11. |

Titanium powder - overview |

|

6.12. |

Titanium powder - main players |

|

6.13. |

Titanium powder - main players |

|

6.14. |

Key material start-ups for metal additive manufacturing |

|

6.15. |

Recycled titanium feedstocks |

|

6.16. |

Metal powder bed fusion post processing |

|

6.17. |

Barriers and limitations to using metal powders |

|

7. |

COMPATIBLE METAL MATERIALS |

|

7.1. |

Alloys and material properties |

|

7.2. |

Aluminum and alloys |

|

7.3. |

Expanding the Aluminum AM Material Portfolio |

|

7.4. |

Copper and bronze |

|

7.5. |

3D Printing with Copper: Huge Potential with Many Challenges |

|

7.6. |

Expanding the Copper AM Material Portfolio |

|

7.7. |

Current Applications for Copper 3D Printing |

|

7.8. |

Cobalt and alloys |

|

7.9. |

Nickel alloy: Inconel 625 |

|

7.10. |

Nickel alloy: Inconel 718 |

|

7.11. |

Precious metals and alloys |

|

7.12. |

Maraging Steel 1.2709 |

|

7.13. |

15-5PH Stainless Steel |

|

7.14. |

17-4 PH Stainless Steel |

|

7.15. |

316L stainless steel |

|

7.16. |

Titanium and alloys |

|

7.17. |

Metal wire feedstocks |

|

7.18. |

Metal wire feedstocks |

|

7.19. |

Metal + polymer filaments |

|

7.20. |

Metal + polymer filaments |

|

7.21. |

Metal + polymer filaments: BASF Ultrafuse 316LX |

|

7.22. |

Metal + photopolymer resin |

|

7.23. |

Metal + photopolymer resin |

|

7.24. |

AM of High Entropy Alloys |

|

7.25. |

AM of amorphous alloys |

|

7.26. |

Emerging aluminium alloys and MMCs |

|

7.27. |

Multi-material solutions |

|

7.28. |

Materials informatics for additive manufacturing materials |

|

7.29. |

Materials informatics for additive manufacturing materials |

|

ページTOPに戻る

Summary

この調査レポートでは、業界の今後10年間の金属印刷用ハードウェアと金属3D印刷材料の需要について詳細に調査・分析しています。市場での豊富な歴史と多数の一次取材に基づき、過去2年間のCOVID-19の大流行による影響と回復を含め、公平な市場予測を提供しています。

主な掲載内容(目次より抜粋)

-

金属印刷プロセス

-

新しい金属印刷プロセス

-

メタルプリンター:比較とベンチマーキング

-

3Dプリンティング用金属材料

-

適合する金属材料

Report Summary

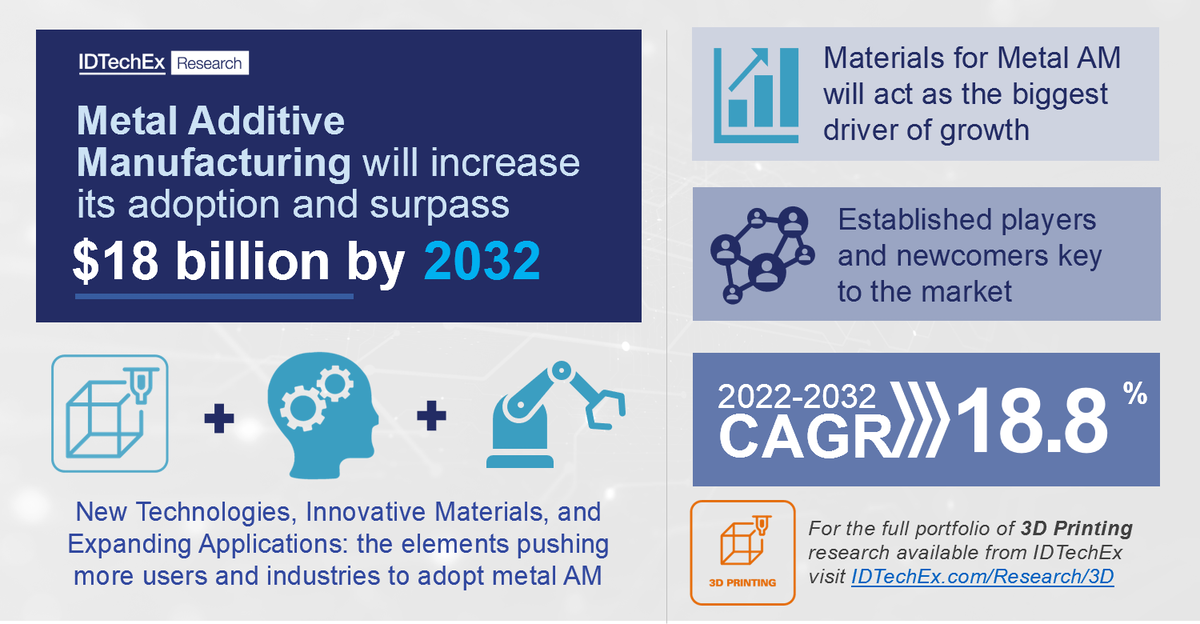

After initial commercialization in the 1990s, metal additive manufacturing (also referred to as 3D printing of metals) has witnessed a flurry of interest in recent years. Key players have been quick to capitalize on this demand, enjoying exponential revenue growth since 2013 as a result.

This comprehensive technical report from IDTechEx gives the detailed status and outlook for the industry. Built upon an extensive history in the market and large number of primary interviews, this report provides an unbiased forecast for the market, including the impact and recovery from the COVID-19 pandemic in the past two years.

Granular forecasts and detailed player profiles

This report provides granular 10-year market forecasts for the industry. The demand for metal printing hardware and metal 3D printing materials in the next decade is quantified. Targeted quantitative analysis is given for printer technologies and materials, broken down into 10 technology segments and 9 materials segments.

These forecasts are generated by the IDTechEx analyst team. The analysts go far beyond what is publicly available by conducting an extensive number of primary interviews, providing the latest and most important information to the reader. Over 75 company profiles are included as part of this report; this includes key OEMs, disruptive start-ups, incumbent powder providers, and emerging material companies.

Benchmarking the competitive printer processes

The proposed advantages to metal additive manufacturing are numerous with design freedom, local versatile manufacturing, potential cost savings, shortened manufacturing times, and much more.

To exploit this there is an ever-expanding family of printer processes using a wide number of material feedstocks. A common tactic for new entrants is to invent new terms for their technology to differentiate from the competition. Some of these are unique but most are aligned with existing processes, introducing only subtle variations.

This report cuts through this marketing and provides accessible impartial categorization for the industry. The reality is that every process must compromise on something, be it the rate, price, precision, size, material compatibility, or more. IDTechEx provide critical benchmarking studies of these processes: an essential process for identifying gaps in the market and end-use applications.

There is also the learning curve to be considered. As with any new (primarily) B2B technology with a large price-tag, it will take time for end-users to have confidence in the process and value-add to warrant the investment. Powder bed fusion processes (DMLS, SLM, and EBM) have been commercial for the longest time, which results in this technology underpinning most installations. However, the next generation of technologies is gaining more traction and within the next decade a more diverse installation base will be observed.

There are some overarching trends for new entrants as they try to find gaps in the market. Low-cost variants, printers pushing the size extremes from micro to very large scales, faster rates, and those exploiting alternative forms of feedstocks are all rapidly emerging and assessed.

Expanding material portfolio, capacity, and competition

IDTechEx forecast that the majority of annual revenue will come from material demand rather than printer sales and installation. Every printer process and application has different material requirements, throughput rates, and alloy demands.

There is a large amount of movement in this industry with notable acquisitions, capacity expansions, improved atomization processes, new materials, and cost reductions. Players are introducing material portfolios bespoke for additive manufacturing from well-known structural alloys to advanced options such as MMCs, high entropy alloys, and amorphous alloys.

Given the variation across this industry, there are very different forecasts when considering cost and volume; titanium powder will be the most significant which is again evident from the market dynamics of expansions, investments, vertical integration and exploring new avenues such as the use of scrap feedstocks.

Key markets and the impact of COVID-19

Metal additive manufacturing has been used for prototypes, tooling, replacement parts, and small to large manufacturing. There are multiple sectors in which this emerging technology is gaining significant uptake, including oil & gas, jewelry, and building & construction. The growth and adoption have all been in high-value industry verticals and the long-term future looks very optimistic.

That said, the COVID-19 global pandemic rapidly introduced new opportunities and concerns for the industry. One opportunity has arisen from major disruptions in global supply chains, which is new interest in distributed manufacturing operations. As international manufacturers address vulnerabilities in their supply chain, metal additive manufacturing has the potential to position itself as a key component in solving supply chain issues. On the other hand, key markets like aerospace face prolonged recovery from pandemic effects. This report analyzes the many trends and global market factors impacting metal additive manufacturing within the decade.

This market report gives granular forecasts for technologies and materials taking into account the impact of COVID-19.

Key questions that are answered in this report

-

What are the current and emerging printer technology types?

-

How do metrics such as price, build speed, build volume and precision vary by printer type?

-

What are the strengths and weaknesses of different 3D printing technologies?

-

Which printers support different material feedstock?

-

What is the current installed base of metal 3D printers?

-

What is the price range of 3D metal printers by technology type?

-

What are the market shares of those active in the market?

-

What are the key drivers and restraints of market growth?

-

Who are the main players and emerging start-ups?

-

How will sales of different printer types evolve from 2022 to 2032?

-

What was the impact of the COVID-19 pandemic on metal 3D printing in 2020 and 2021?

ページTOPに戻る

Table of Contents

|

1. |

EXECUTIVE SUMMARY |

|

1.1. |

Metal Additive Manufacturing: Technology Overview |

|

1.2. |

Metal 3D Printing Technologies: Benchmarking Overview |

|

1.3. |

Market Forecast for Metal Additive Manufacturing |

|

1.4. |

Metal 3D Printing Continues Seeing Innovation |

|

1.5. |

Material-Process Relationships |

|

1.6. |

Timeline of 3D Printing Metals |

|

1.7. |

Drivers and Restraints of Growth for 3D Printing |

|

1.8. |

Impact of COVID-19: Summary of Company Perspectives |

|

1.9. |

Revenue Recovery from COVID-19 in 2020 and 2021 |

|

1.10. |

COVID-19 and 3D Printing: Takeaways |

|

1.11. |

Metal 3D Printing Investment Overview for 2021 |

|

1.12. |

Companies Going Public in 2021: Summary |

|

1.13. |

Technology Segmentation |

|

1.14. |

Technology Installed Base and Market Share in 2022 |

|

1.15. |

Technology Installed Base and Market Share in 2032 |

|

1.16. |

Market Share by Mass of Metals Demand by Alloy |

|

1.17. |

Metal Hardware Revenue Forecast by Technology |

|

1.18. |

Metal Material Forecast By Technology - Revenue and Mass |

|

1.19. |

Metal Material Forecast by Technology - Discussion |

|

1.20. |

Metal Material Forecast By Alloy - Revenue and Mass |

|

1.21. |

Metal Material Forecast by Alloy - Discussion |

|

1.22. |

Key Trends in Metal Additive Manufacturing |

|

1.23. |

Key Trends in Metal Additive Manufacturing |

|

1.24. |

Company Profiles |

|

2. |

INTRODUCTION |

|

2.1. |

Glossary: common acronyms for reference |

|

2.2. |

Scope of Report |

|

2.3. |

The Different 3D Printing Processes |

|

2.4. |

Material-Process Relationships |

|

2.5. |

Why Adopt 3D Printing? |

|

2.6. |

Timeline of 3D Printing Metals |

|

2.7. |

Business Models: Selling Printers vs Parts |

|

2.8. |

The Desktop 3D Printer Explosion |

|

2.9. |

Drivers and Restraints of Growth for 3D Printing |

|

2.10. |

Computer Aided Engineering (CAE): Topology |

|

3. |

METAL PRINTING PROCESSES |

|

3.1. |

Powder Bed Fusion: Direct Metal Laser Sintering (DMLS) |

|

3.2. |

Powder Bed Fusion: Electron Beam Melting (EBM) |

|

3.3. |

Directed Energy Deposition: Powder |

|

3.4. |

Directed Energy Deposition: Wire |

|

3.5. |

Binder Jetting: Metal Binder Jetting |

|

3.6. |

Binder Jetting: Sand Binder Jetting |

|

3.7. |

Sheet Lamination: Ultrasonic Additive Manufacturing (UAM) |

|

4. |

NEW METAL PRINTING PROCESSES |

|

4.1. |

Emerging Printing Processes - Overview |

|

4.2. |

Extrusion: Metal-Polymer Filament (MPFE) |

|

4.3. |

Extrusion: Metal-Polymer Pellet |

|

4.4. |

Extrusion: Metal Paste |

|

4.5. |

Vat Photopolymerisation: Digital Light Processing (DLP) |

|

4.6. |

Material Jetting: Nanoparticle Jetting (NPJ) |

|

4.7. |

Material Jetting: Magnetohydrodynamic Deposition |

|

4.8. |

Material Jetting: Electrochemical Deposition |

|

4.9. |

Material Jetting: Cold Spray |

|

4.10. |

Binder Jetting Advancements |

|

4.11. |

Developments in PBF and DED: Energy Sources |

|

4.12. |

Developments in PBF and DED: Low-Cost Printers |

|

4.13. |

Developments in PBF and DED: New Technologies |

|

4.14. |

Processes with a Metal Slurry Feedstock |

|

4.15. |

Alternative Emerging DMLS Variations |

|

5. |

METAL PRINTERS: COMPARISON AND BENCHMARKING |

|

5.1. |

Metal Additive Manufacturing: Technology Overview |

|

5.2. |

Benchmarking: Maximum Build Volume |

|

5.3. |

Benchmarking: Build Rate |

|

5.4. |

Benchmarking: Z Resolution |

|

5.5. |

Benchmarking: XY Resolution |

|

5.6. |

Benchmarking: Price vs Build Volume |

|

5.7. |

Benchmarking: Price vs Build Rate |

|

5.8. |

Benchmarking: Price vs Z Resolution |

|

5.9. |

Benchmarking: Build Rate vs Build Volume |

|

5.10. |

Benchmarking: Build Rate vs Z Resolution |

|

5.11. |

Overview of Metal 3D Printing Technologies |

|

5.12. |

Maximums & Minimums of Metal 3D Printing Technologies |

|

6. |

METAL MATERIALS FOR 3D PRINTING |

|

6.1. |

Material feedstock options |

|

6.2. |

Powder morphology specifications |

|

6.3. |

Water or gas atomisation |

|

6.4. |

Plasma atomisation |

|

6.5. |

Electrochemical atomisation |

|

6.6. |

Powder morphology depends on atomisation process |

|

6.7. |

Evaluation of powder manufacturing techniques |

|

6.8. |

Supported materials |

|

6.9. |

Suppliers of metal powders for AM |

|

6.10. |

Suppliers of metal powders for AM |

|

6.11. |

Titanium powder - overview |

|

6.12. |

Titanium powder - main players |

|

6.13. |

Titanium powder - main players |

|

6.14. |

Key material start-ups for metal additive manufacturing |

|

6.15. |

Recycled titanium feedstocks |

|

6.16. |

Metal powder bed fusion post processing |

|

6.17. |

Barriers and limitations to using metal powders |

|

7. |

COMPATIBLE METAL MATERIALS |

|

7.1. |

Alloys and material properties |

|

7.2. |

Aluminum and alloys |

|

7.3. |

Expanding the Aluminum AM Material Portfolio |

|

7.4. |

Copper and bronze |

|

7.5. |

3D Printing with Copper: Huge Potential with Many Challenges |

|

7.6. |

Expanding the Copper AM Material Portfolio |

|

7.7. |

Current Applications for Copper 3D Printing |

|

7.8. |

Cobalt and alloys |

|

7.9. |

Nickel alloy: Inconel 625 |

|

7.10. |

Nickel alloy: Inconel 718 |

|

7.11. |

Precious metals and alloys |

|

7.12. |

Maraging Steel 1.2709 |

|

7.13. |

15-5PH Stainless Steel |

|

7.14. |

17-4 PH Stainless Steel |

|

7.15. |

316L stainless steel |

|

7.16. |

Titanium and alloys |

|

7.17. |

Metal wire feedstocks |

|

7.18. |

Metal wire feedstocks |

|

7.19. |

Metal + polymer filaments |

|

7.20. |

Metal + polymer filaments |

|

7.21. |

Metal + polymer filaments: BASF Ultrafuse 316LX |

|

7.22. |

Metal + photopolymer resin |

|

7.23. |

Metal + photopolymer resin |

|

7.24. |

AM of High Entropy Alloys |

|

7.25. |

AM of amorphous alloys |

|

7.26. |

Emerging aluminium alloys and MMCs |

|

7.27. |

Multi-material solutions |

|

7.28. |

Materials informatics for additive manufacturing materials |

|

7.29. |

Materials informatics for additive manufacturing materials |

|

ページTOPに戻る

IDTechEx社の3D印刷 - 3D Printing分野での最新刊レポート

本レポートと同じKEY WORD()の最新刊レポート

- 本レポートと同じKEY WORDの最新刊レポートはありません。

よくあるご質問

IDTechEx社はどのような調査会社ですか?

IDTechExはセンサ技術や3D印刷、電気自動車などの先端技術・材料市場を対象に広範かつ詳細な調査を行っています。データリソースはIDTechExの調査レポートおよび委託調査(個別調査)を取り扱う日... もっと見る

調査レポートの納品までの日数はどの程度ですか?

在庫のあるものは速納となりますが、平均的には 3-4日と見て下さい。

但し、一部の調査レポートでは、発注を受けた段階で内容更新をして納品をする場合もあります。

発注をする前のお問合せをお願いします。

注文の手続きはどのようになっていますか?

1)お客様からの御問い合わせをいただきます。

2)見積書やサンプルの提示をいたします。

3)お客様指定、もしくは弊社の発注書をメール添付にて発送してください。

4)データリソース社からレポート発行元の調査会社へ納品手配します。

5) 調査会社からお客様へ納品されます。最近は、pdfにてのメール納品が大半です。

お支払方法の方法はどのようになっていますか?

納品と同時にデータリソース社よりお客様へ請求書(必要に応じて納品書も)を発送いたします。

お客様よりデータリソース社へ(通常は円払い)の御振り込みをお願いします。

請求書は、納品日の日付で発行しますので、翌月最終営業日までの当社指定口座への振込みをお願いします。振込み手数料は御社負担にてお願いします。

お客様の御支払い条件が60日以上の場合は御相談ください。

尚、初めてのお取引先や個人の場合、前払いをお願いすることもあります。ご了承のほど、お願いします。

データリソース社はどのような会社ですか?

当社は、世界各国の主要調査会社・レポート出版社と提携し、世界各国の市場調査レポートや技術動向レポートなどを日本国内の企業・公官庁及び教育研究機関に提供しております。

世界各国の「市場・技術・法規制などの」実情を調査・収集される時には、データリソース社にご相談ください。

お客様の御要望にあったデータや情報を抽出する為のレポート紹介や調査のアドバイスも致します。

|

|

ページTOPに戻る

|